问题如下:

Based on Exhibit 1, Olabudo should:

选项:

A.conclude that the inflation predictions are unbiased.

reject the null hypothesis that the slope coefficient equals 1.

reject the null hypothesis that the intercept coefficient equals 0.

解释:

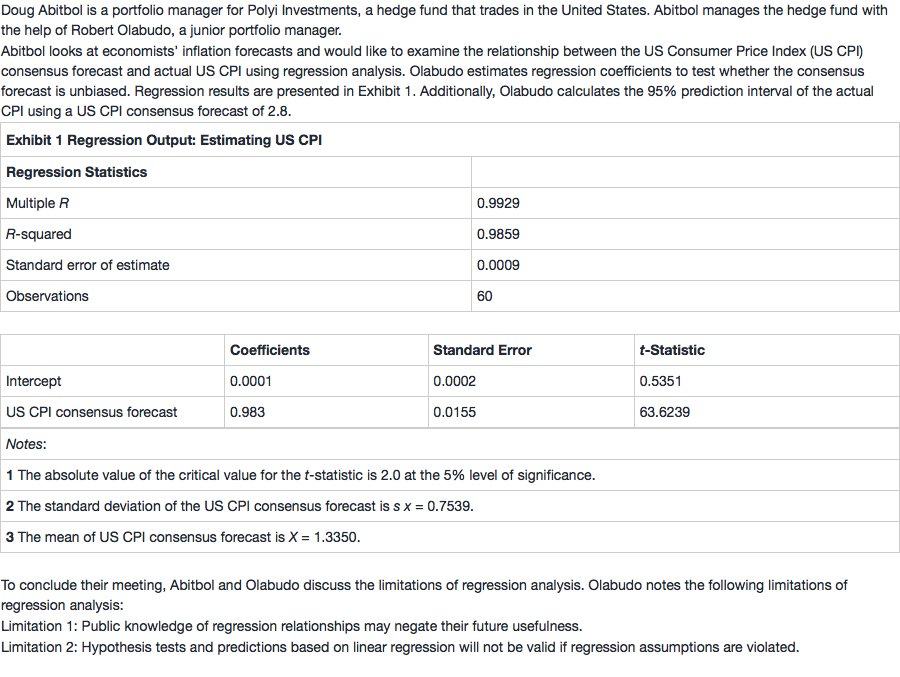

A is correct. If the consensus inflation forecast is unbiased, then the intercept, b0, should equal 0, and the slope coefficient, b1, should equal 1. The t-statistic for the intercept coefficient is 0.5351, which is less than the critical t-value of 2.0, so the intercept coefficient is not statistically different than 0. To test whether the slope coefficient equals 1, the t-statistic is calculated as: t=–1.0968

Because the absolute value of the t-statistic of –1.0968 is less than the critical t-value of 2.0, the slope coefficient is not statistically different than 1. Therefore, Olabudo can conclude that the inflation forecasts are unbiased.

能解释一下什么叫unbiased吗?为什么unbiased就是截距为0,斜率为1?