问题如下:

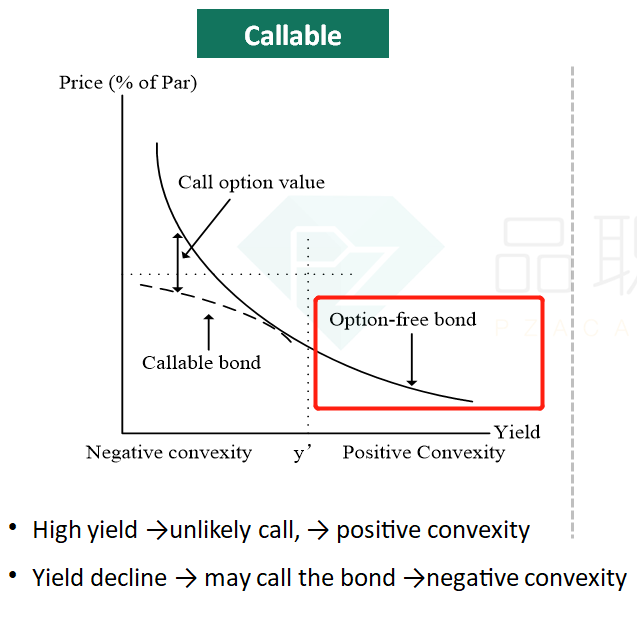

Other things equal, why would the duration of callable bond be less than that of other option-free bond?

选项:

A. As YTM increases, the value of the call option increases.

B. As YTM decreases, the value of the call option increases.

C. As bond price increases, the value of the call option decreases.

解释:

B is correct.

value of callable bond=straight bond value−value of call option

When the YTM of a callable bond falls, both the bond price and the call option value increase, therefore the increment in price is less than for an option-free bond.

YTM上升时,结果如何?