问题如下:

2. NinMount’s long-term debt to equity ratio on 31 December 2008 most likely will be lowest if the results of the acquisition are reported using:

选项:

A.the equity method.

B.consolidation with full goodwill.

C.consolidation with partial goodwill.

解释:

A is correct.

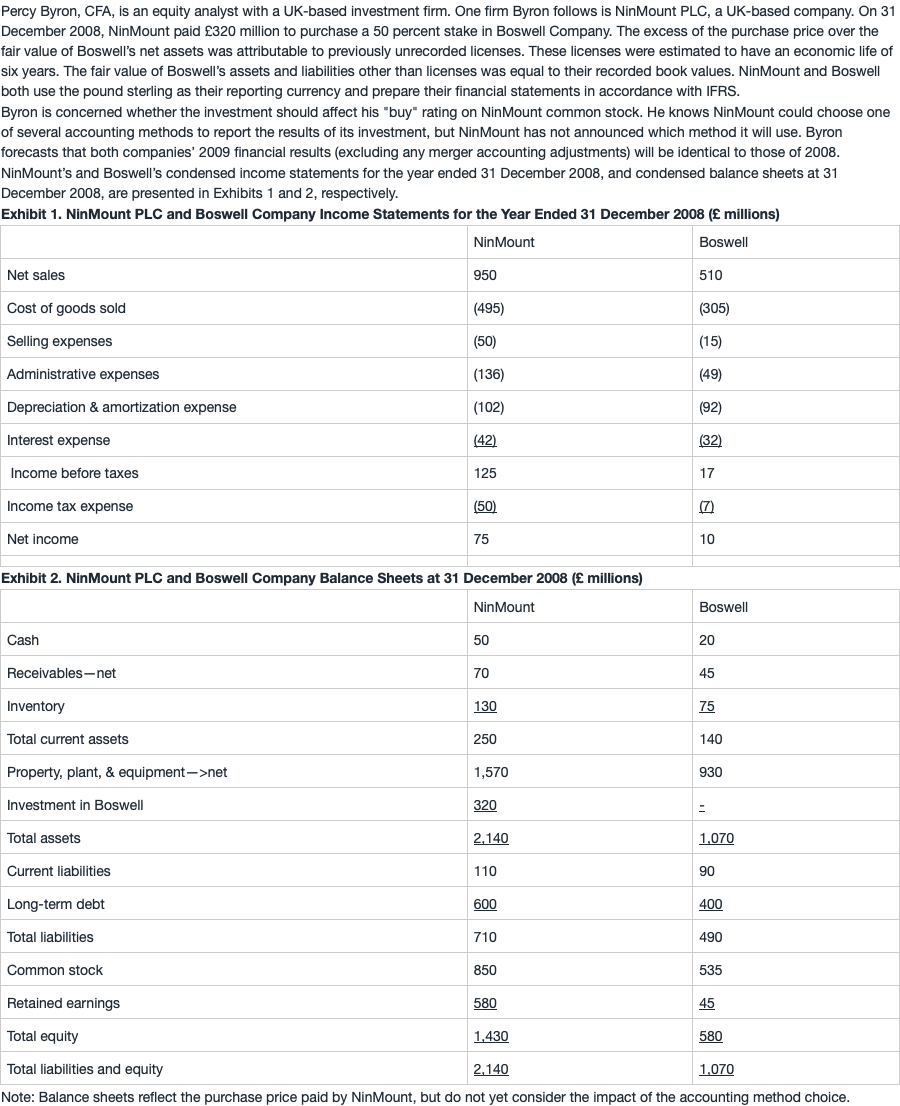

Using the equity method, long-term debt to equity = £600/£1,430 = 0.42. Using the consolidation method, long-term debt to equity = long-term debt/equity = £1,000/£1,750 = 0.57. Equity includes the £320 noncontrolling interest under either consolidation. It does not matter if the full or partial goodwill method is used since there is no goodwill.

考点 : 不同的会计方法对财务比率的影响

解析 :

如果使用equity method , long-term debt to equity= £600/£1,430 = 0.42

如果使用consolidation method,equity=£1,430+320(noncontrolling interest )=£1,750

long-term debt to equity=£1,000/£1,750 = 0.57

母公司取得子公司50%股权花费320,且根据题干没有goodwill,说明归属于少数股东的权益也是320.

consolidation method下,equity不仅包含归属于母公司的部分,也包含少数股东权益,因此加上320.

老师这个unrecord liscense是一个identifiable asset吗?如果是这样子的话,那么为啥在子公司的BS表的Asset一侧没有记录呢?我看到解析是说consideration等于FV of net identifiable asset,GW是0。