问题如下:

A bond portfolio manager wants to reduce the duration from 5.5 to 4.5 by interest rate swap, she would enter into a:

选项:

A.receiver swap involving paying fixed-rate payments and receiving floating-rate payments.

B.receiver swap involving paying floating-rate payments and receiving fixed-rate payments.

C.payer swap involving paying fixed-rate payments and receiving floating-rate payments.

解释:

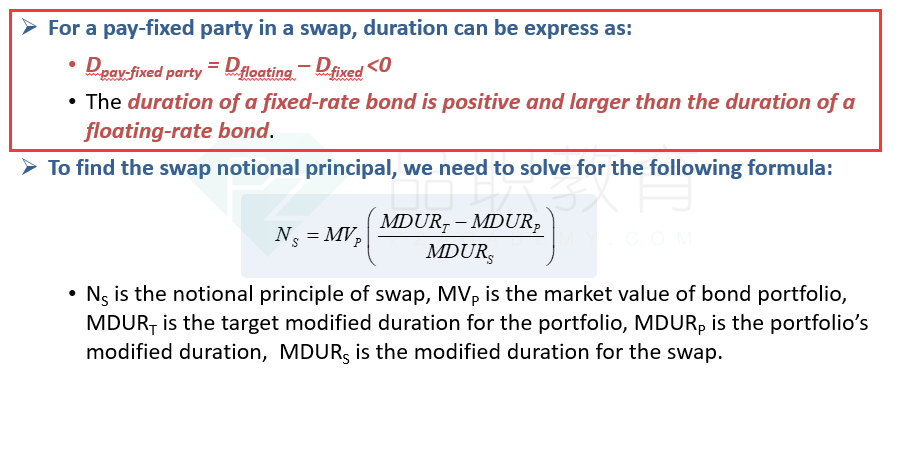

C is correct.

考点:interest rate swap

解析:

投资者希望降低组合的duration,因此应该进入一个duration为负的interest rate swap。

因为固定端的duration大于浮动端的duration,所以付固定、收浮动的duration为负,即应该进入payer swap.

为什么付固定、收浮动的duration为负?付固定是固定利率还是固定margin加上一个基准的浮动利率?谢谢