问题如下:

4. The value of Position 3 is closest to:

选项:

A.-¥40,020.

B.¥139,913.

C.¥239,963.

解释:

C is correct.

The current no-arbitrage price of the forward contract is

Ft(¥/$,T) = St(¥/$)FV¥,t,T(1)/FV$,t,T(1)

Ft(¥/$,T) = ¥112.00(1 - 0.002)0.25/(1 + 0.003)0.25 = ¥111.8602

Therefore, the value of Troubadour’s position in the ¥/$ forward contract, on a per dollar basis, is

Vt(T) = PV¥,t,T[F0(¥/$,T) - Ft(¥/$,T)]

=(112.10 - 111.8602)/(1 - 0.002)025 = ¥0.239963 per $1

Troubadour’s position is a short position of $1,000,000, so the short position has a positive value of (¥0.239963/$) x $1,000,000 = ¥239,963 because the forward rate has fallen since the contract initiation.

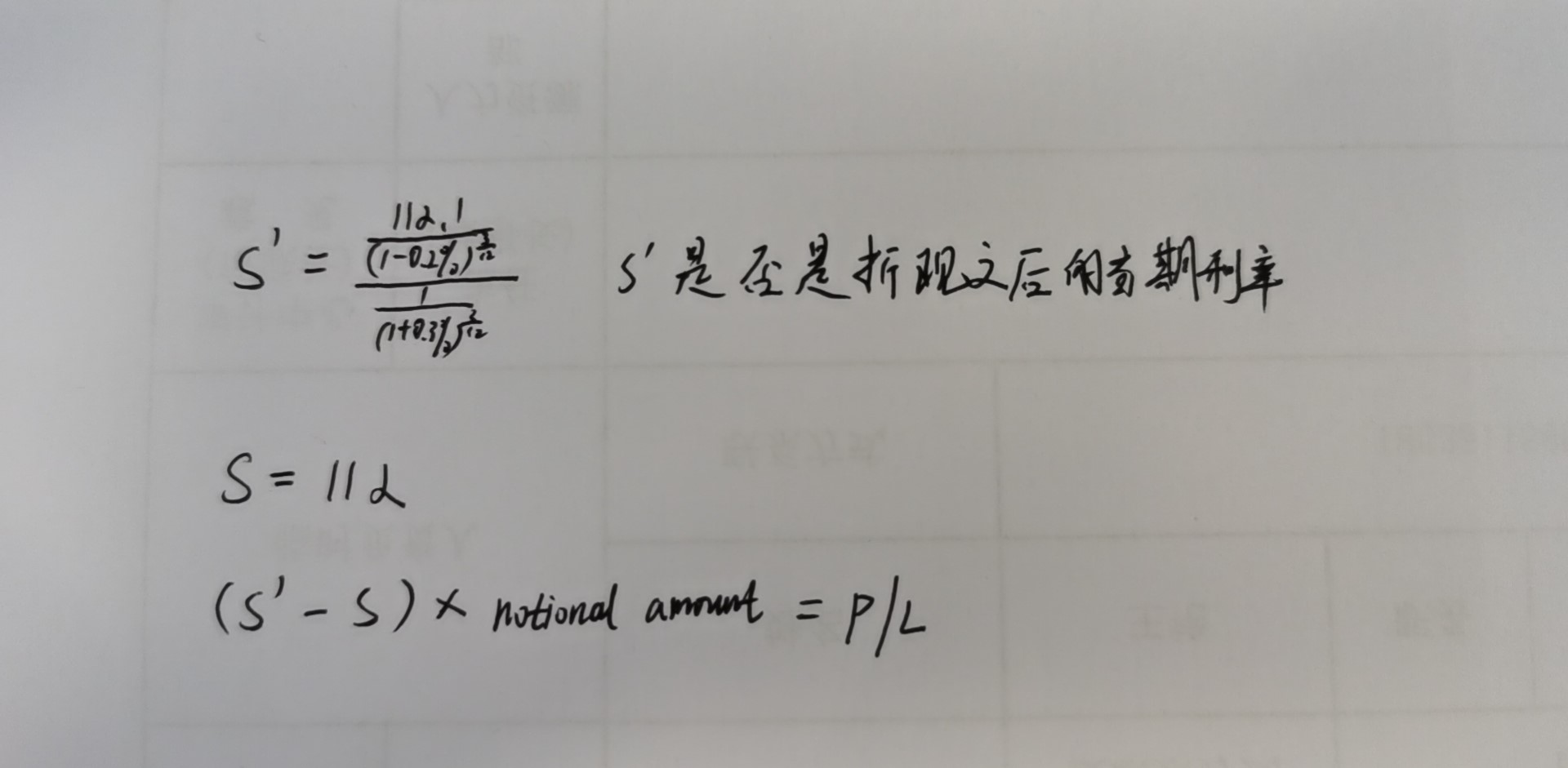

老师您好,如果先求出即期的汇率,然后和cureent的汇率做差,这样理解有什么问题呢,如图: