问题如下:

Among the scenarios in the previous question, Winslow’s portfolio is most sensitive to:

选项:

A. Scenario (A).

B. Scenario (B).

C. Scenario (C)

解释:

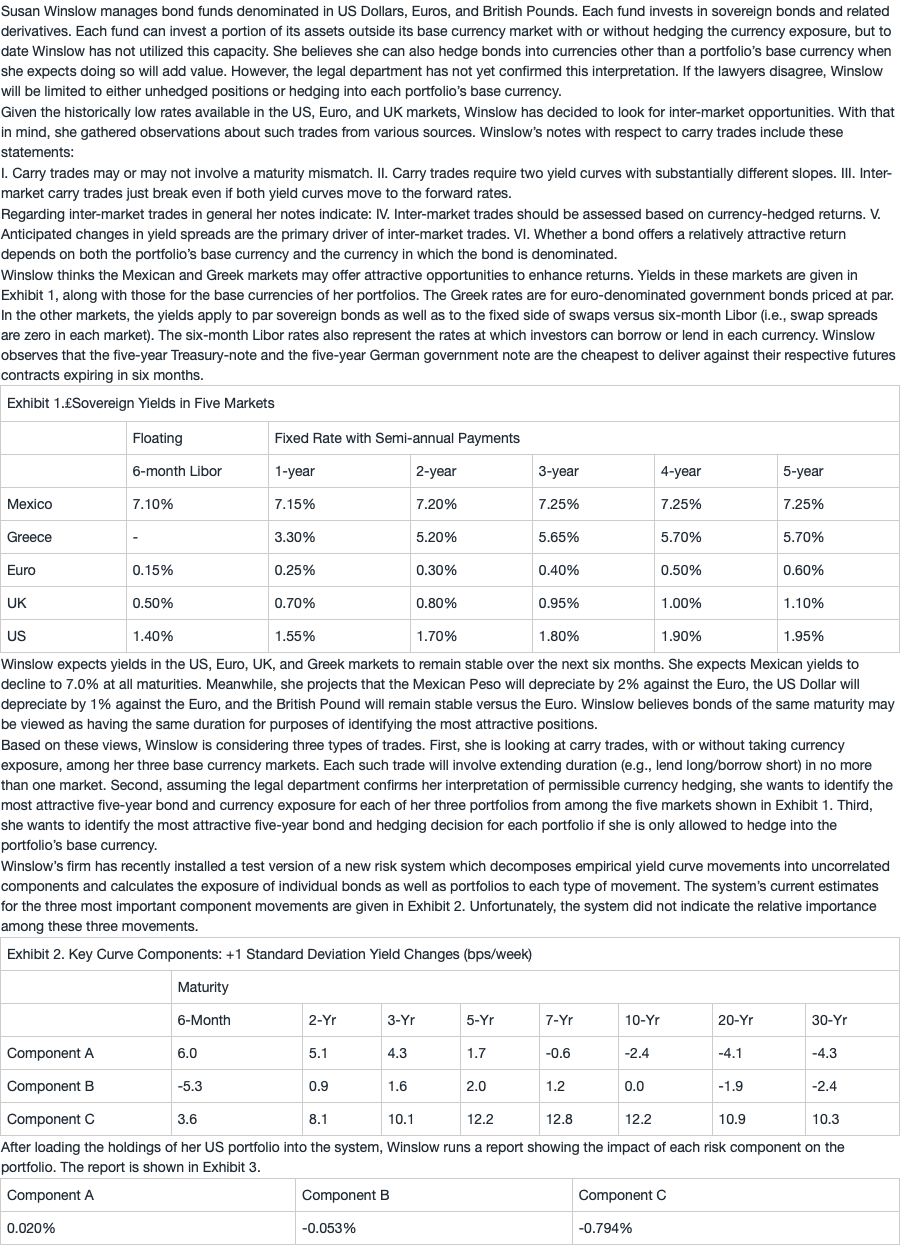

C is correct.

The impact of each scenario on Winslow’s portfolio is simply an equally weighted combination of the impacts given in Exhibit 3. Scenario A: 0.02 + (–0.053) + (–0.794) = –0.827 Scenario B: 0.02 – (–0.053) + (–0.794) = –0.721 Scenario C: –0.02 + (–0.053) + (–0.794) = –0.867 A is incorrect. Winslow’s portfolio is more sensitive to scenario C. B is incorrect. Winslow’s portfolio is more sensitive to each of the other scenarios.

题目表格里的company麻烦改一下,那是component