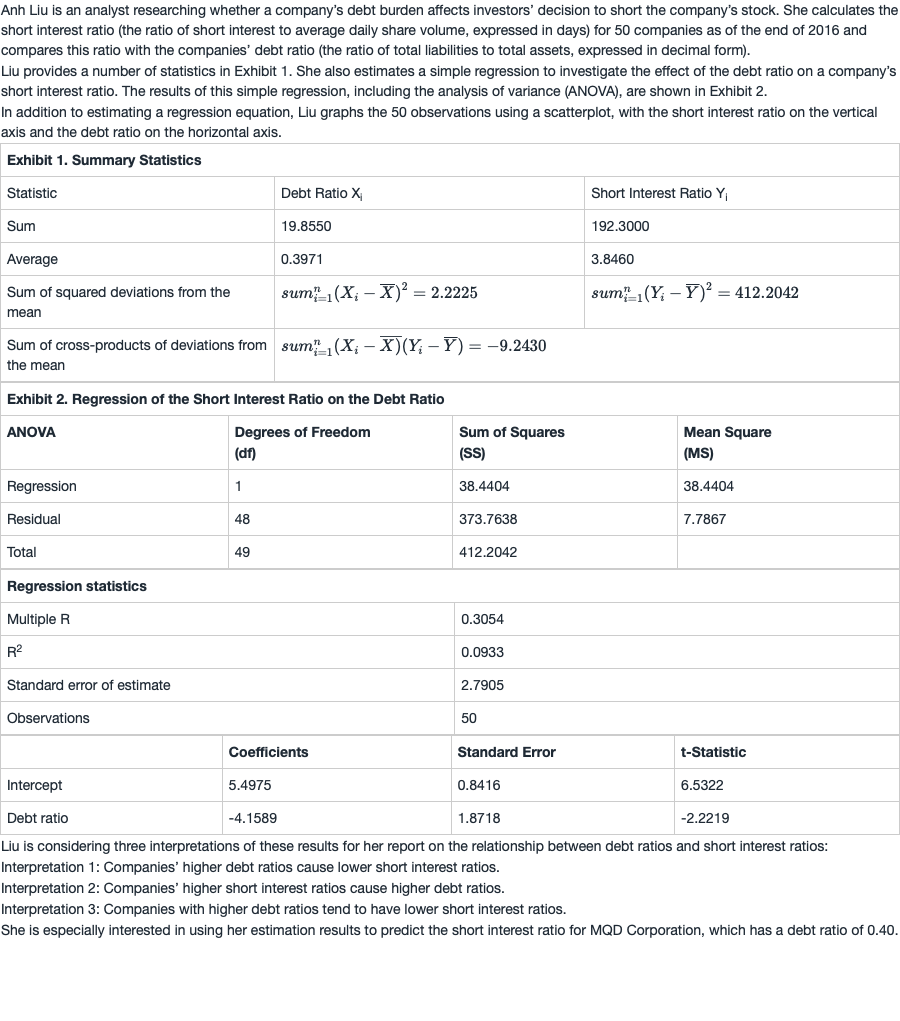

问题如下:

8. Which of the following should Liu conclude from these results shown in Exhibit 2?

选项:

A.The average short interest ratio is 5.4975.

B.The estimated slope coefficient is statistically significant at the 0.05 level.

C.The debt ratio explains 30.54% of the variation in the short interest ratio.

解释:

B is correct.

The t-statistic is −2.2219, which is outside of the bounds created by the critical t-values of ± 2.011 for a two-tailed test with a 5% significance level. The 2.011 is the critical t-value for the 5% level of significance (2.5% in one tail) for 48 degrees of freedom.

significant是说不等于0对吗?H0不是=0的假设吗?如果统计量小于-2.011就是落在了左侧,那么应该接受H0啊,那就是等于0的假设,那么不是应该not significant different from 0吗?