问题如下:

5.Based on Exhibit 5, the current value of the equity swap described in Exhibit 4 would be zero if the equity index was currently trading the closest to:

选项:

A. 97.30.

B. 99.09.

C. 100.00.

解释:

B is correct. The equity index level at which the swap’s fair value would be zero can be calculated by setting the swap valuation formula equal to zero and solving for St:

V_t=FB(C_0)-\left(\frac{s_t}{s_t-}\right)NA_E\\\\

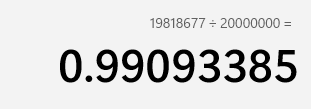

The value of the fixed leg of the swap has a present value of $19,818,677, or 99.0934% of par value:

Treating the swap notional value as par value and substituting the present value of the fixed leg and into the equation yields

Solving for St yields St = 99.0934

为什么没加上0.895255呢?谢谢老师