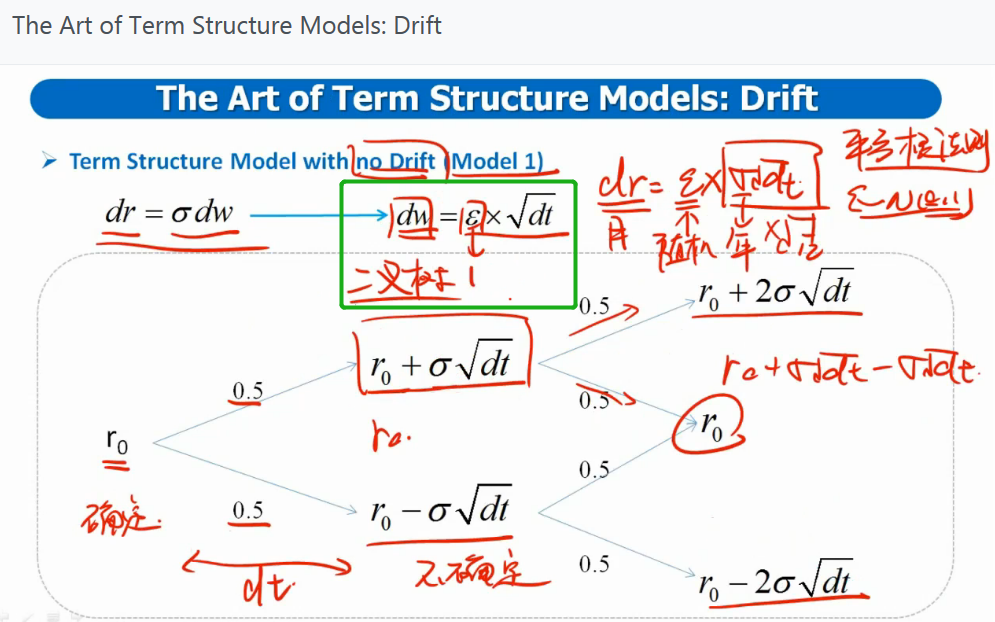

问题如下:

Using the Vasicek model, assume a current short-term rate of 6.2% and an annual volatility of the interest rate process of 2.5%. Also assume that the long-run mean- reverting level is 13.2% with a speed of adjustment of 0.4. Within a binomial interest rate tree, what are the upper and lower node rates after the first month?

选项:

Upper node

Lower node

6.67%

5.71%

6.67%

6.24%

7.16%

6.24%

7.16%

5.71%

解释:

D is correct. Using a Vasicek model, the upper and lower nodes for time 1 are computed as follows:

请问这里为什么没有把dt乘进去呢?只算了k(θ-r).