问题如下:

There is a bond with the effective duration of 11 and the convexity of 120. If the yield falls by 200 basis points, what's the percentage of the price change of the bond?

选项:

A.19.6%

B.24.4%

C.26.8%

解释:

B is correct.

Correct answer:

the percentage of the price change= -effective duration * (ΔYTM)+(1/2) * convexity * (ΔYTM)2 = (-11)*(-2%)+(1/2) * 120 * (2%)2 =0.244=24.4%

Incorrect answer:

the percentage of the price change= -effective duration * (ΔYTM)+convexity * (ΔYTM)2 = (-11)*(-2%)+120 * (2%)2 =0.268=26.8%

the percentage of the price change= -effective duration * (ΔYTM)+(1/2) * (-convexity) * (ΔYTM)2 = (-11)x(-2%)+(1/2)x (-120)x (2%)2 =0.196=19.6%

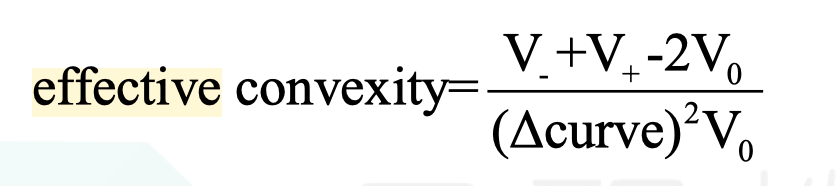

effective duration 与 convexity之间的关联公式是什么?二者如何转换?