问题如下:

Based on Exhibit 1 and assuming Tyo’s market views on yield curve changes are realized, the forward curve of which country will lie below its spot curve?

选项:

A.Country A

B.Country B

C.Country C

解释:

B is correct.

The yield curve for Country B is currently upward sloping, but Tyo expects a reversal in the slope of the current yield curve. This means she expects the resulting yield curve for Country B to slope downward, which implies that the resulting forward curve would lie below the spot yield curve. The forward curve lies below the spot curve in scenarios in which the spot curve is downward sloping;the forward curve lies above the spot curve in scenarios in which the spot curve is upward sloping.

A is incorrect because the yield curve for Country A is currently upward sloping and Tyo expects that the yield curve will maintain its shape and level. That expectation implies that the resulting forward curve would be above the spot yield curve.

C is incorrect because the yield curve for Country C is currently downward sloping and Tyo expects a reversal in the slope of the current yield curve. This means she expects the resulting yield curve for Country C to slope upward, which implies that the resulting forward curve would be above the spot yield curve.

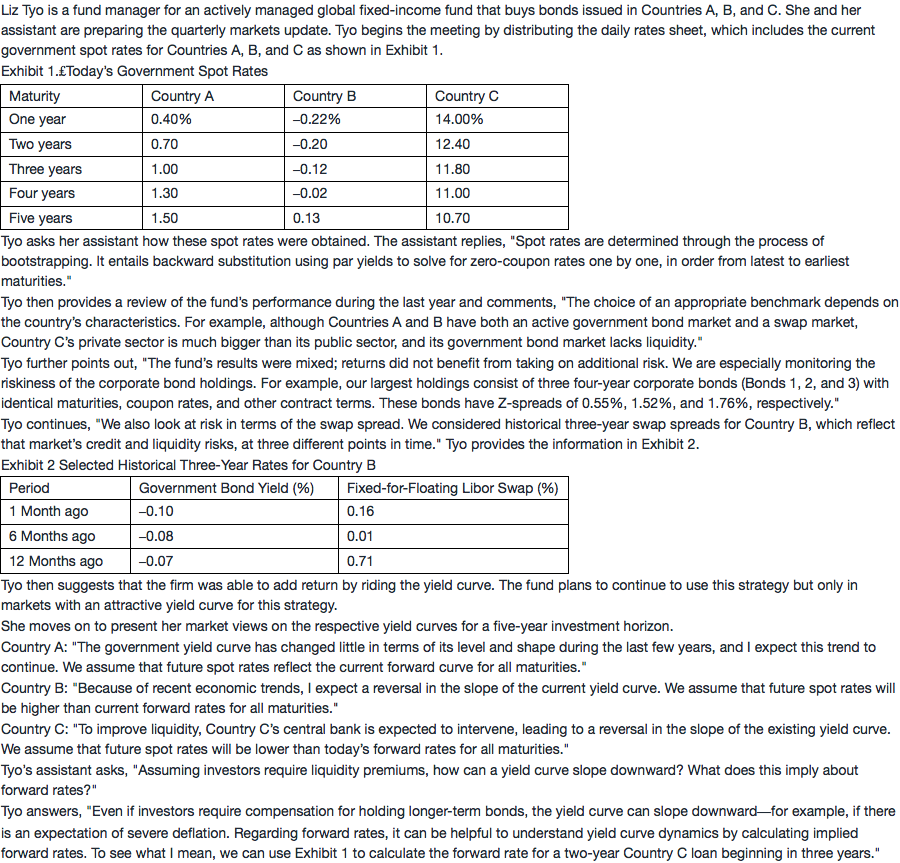

老师,我对这个句话 B 国家 We assume that future spot rates will be > current forward rates for all maturities 有两种理解,不懂哪种是对的.

问题问哪个国家的forward rate在上面

我这么想的:

B说 We assume that future spot rates will be > current forward rates for all maturities,这句话意思是说future spot curve 在上面么?(这是我的一种理解) ( 这个也符合题目说 B reverse, 变成了slope downwards.)

C说future spot rates will be < current forward rates, 这句话意思是说forward 在上面?( 这个也符合题目说C reverse, 变成了slope upwards了。)

我的第二个理解是:

B说 We assume that future spot rates will be > current forward rates for all maturities, 这里面说的current forward是说站在0时刻用表格1 里面的 S1, S2, S3 etc推出来的forward rate 比如下面图里面的 f ( 是么?)

future spot rate就是说到了未来时间点那个真实的future spot rate (比如下面图里面的 S1’ ) ( 是么? ) (这是我的另一个理解)(如下图我画的)

下面一个题目问:Tyo most likely perceives the bonds of which country to be fairly valued?

因为这个forward rate是用现价(0时刻的spot rate们也是现价推出来的) 推出来的,所以如果forward rate 小,说明现价高, 所以是被高估了。(是么?)

不懂我上面的理解都对么?