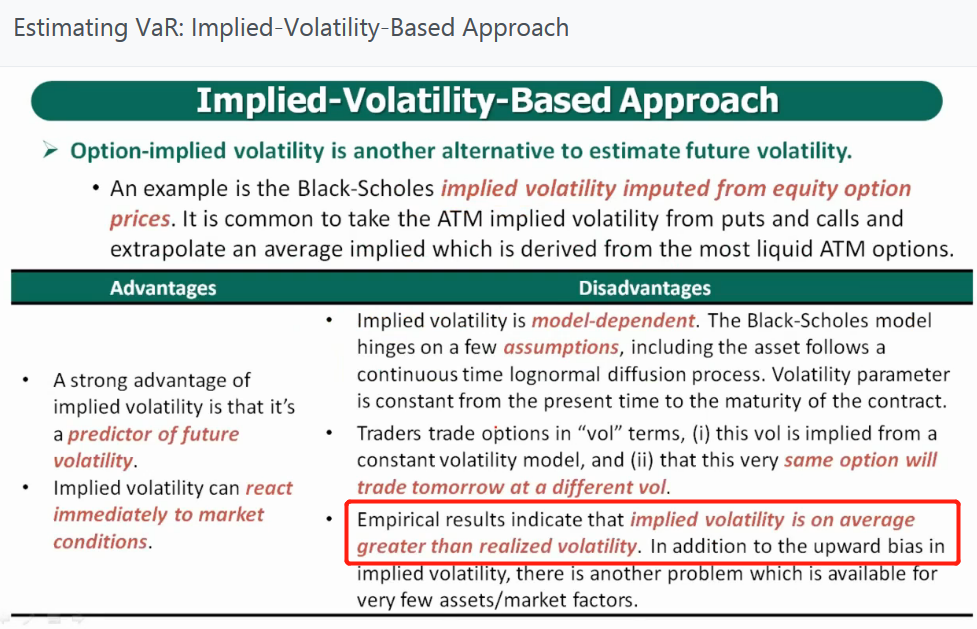

问题如下:

Which of the following statements is an advantage of the implied

volatility method in estimating future volatility?

选项:

A.The implied

volatility model reacts immediately to changing market conditions.

The implied

volatility model is not model dependent.

The implied

volatility is constant through time.

The implied

volatility is biased upward and is therefore more conservative.

解释:

The only advantage listed is that the implied volatility model reacts immediately to changing market conditions. Forecast models based on historical data require time to adjust to market events. Disadvantages include the following: (1) implied volatility is model dependent;(2) a major assumption of the model is that asset follows a continuous time lognormal diffusion process and are assumed to be constant but that implied volatility varies through time; and (3) implied volatility is biased upward.

老师好,D选项,为什么Implied Volatility is biased upward?