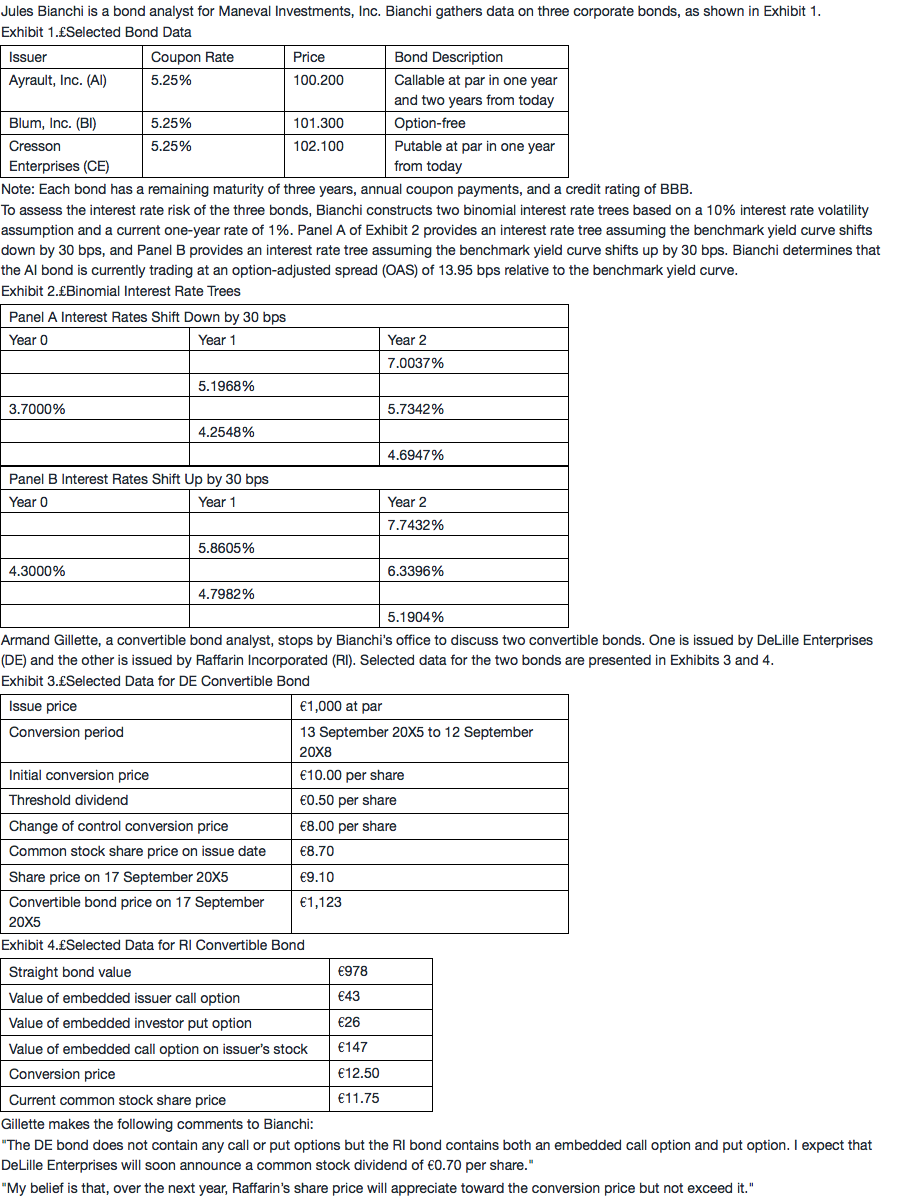

问题如下:

Based on Exhibit 4, the arbitrage-free value of the RI bond is closest to:

选项:

A. €814.

B. €1,056.

C. €1,108.

解释:

C is correct.

The value of a convertible bond with both an embedded call option and a put option can be determined using the following formula:

Value of callable putable convertible bond = Value of straight bond + Value of call option on the issuer’s stock – Value of issuer call option + Value of investor put option.

Value of callable putable bond = €978 + €147 – €43 + €26 = €1,108

147为什么是债券持有人的呢?谢谢老师