问题如下:

Robin Hudson, FRM, was discussing the various methods to estimate default probabilities with her colleague Kate Alexander, FRM. Hudson made the following comments:

I. Transition matrices are an important component of the risk-neutral approach.

II. Hazard rates measure the instantaneous conditional default probability.

III. Risk-neutral default probabilities are downward biased estimates of real-world default probabilities.

How many of these statements should Alexander agree with?

选项:

A.

None of the statements.

B.

One statement.

C.

Two statements.

D.

Three statements.

解释:

B Only statement II is correct. Transition matrices are more likely to be used in the historical approach. Empirical evidence shows that real-world default probabilities are significantly lower than risk-neutral default probabilities.

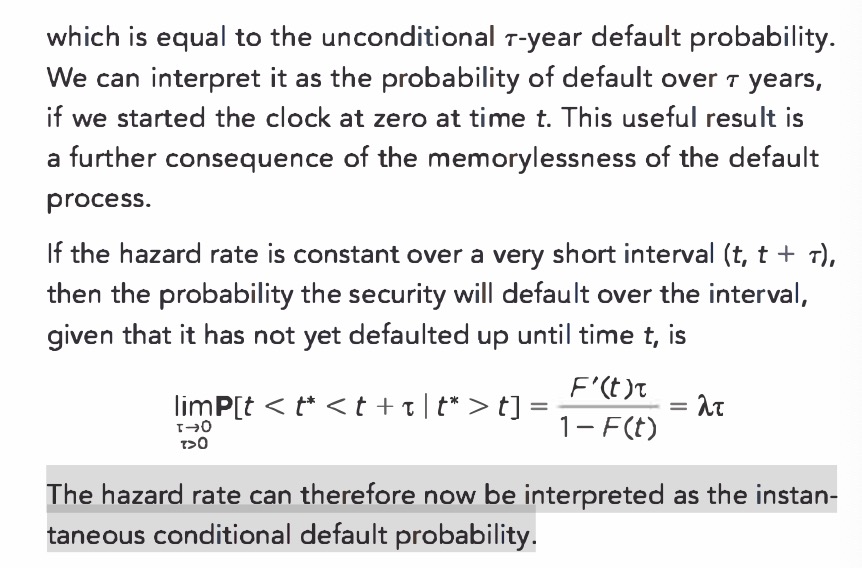

不太理解选项II里这个instantaneous condition是指的什么,Hazard Rate不是指的连续时的违约概率吗?