问题如下:

The interest rate in XXX is 1% and in YYY 4%. The XXXYYY spot rate is 1.3000. How would three-month forward rate be quoted using points?

选项:

解释:

The forward rate is

The forward rate would be quoted as 95.

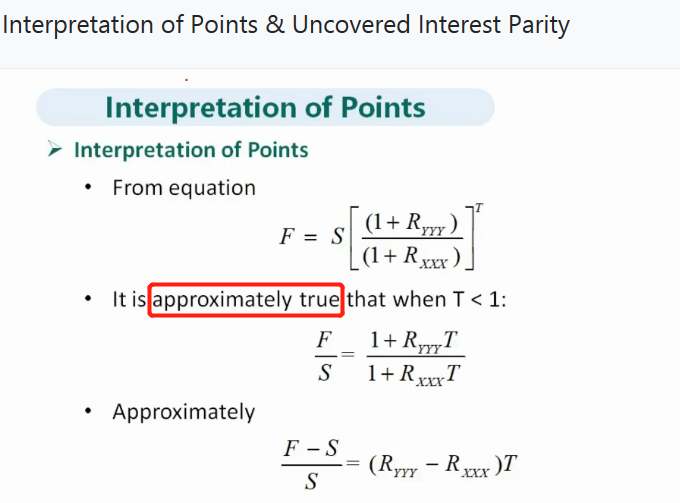

请问他是3个月的,为什么不能用近似的单利的公式呢?

NO.PZ2020020601000059问题如下The interest rate in XXX is 1% anin YYY 4%. The XXXYYY spot rate is 1.3000. How woulthree-month forwarrate quoteusing points? The forwarrate is 1.3000∗(1.04)0.25(1.01)0.25=1.30951.3000 *\frac{(1.04)^{0.25}}{ (1.01)^{0.25}} = 1.30951.3000∗(1.01)0.25(1.04)0.25=1.3095The forwarrate woulquote95. 如题

算出来1.3095后,远期利率的报价为啥是95

之前看李老师视频,xxxyyy就是XXX/YYY,分母应该是YYY,怎么感觉答案除反了

老师在啊合适一下 XXXYYY 是不是写成Y/X,Y是,X是F3 X/Y = 1:3=X:Y = YYYXXX