问题如下:

A USD 1million loan has a probability of 0.5% of defaulting in a year. The recovery

rate is estimated to be 40%. What is the expected credit loss and the standard

deviation of the credit loss?

解释:

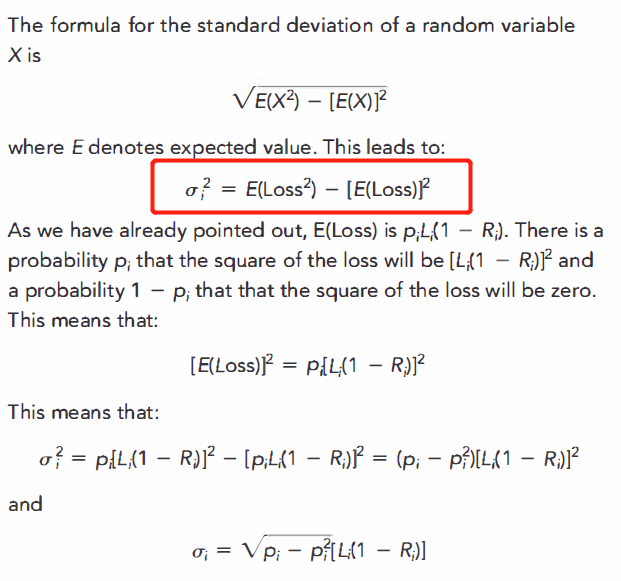

The expected loss in USD is 0.005 × 1 × (1 – 0.4) = 0.003. This is USD 3,000. The