问题如下图:

4800share是如何得出的

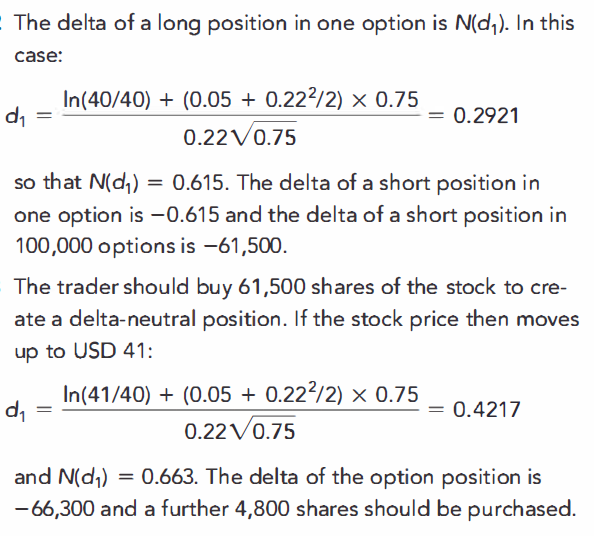

NO.PZ2020021205000065问题如下a short position on 100,000 call options on a stowith a market prianstrike priof US40 when the risk-free rate is 5%, the volatility is 22%, anthe time to maturity is nine months whtra shoulne to create a lta-neutrposition? (Assume ththe trar hno other positions pennt on the stoprice.) If the stopriincreases to US41 within a very short perio whfurther tra is necessary? The trar shoulbuy 61,500 shares of the stoto create a lta-neutrposition. If the stoprithen moves up to US41:=ln(41/40)+(0.05+0.222/2)×0.750.220.75=0.4217=\frac{\ln(41/40)+(0.05+0.22^2/2)\times0.75}{0.22\sqrt{0.75}}=0.4217=0.220.75ln(41/40)+(0.05+0.222/2)×0.75=0.4217anN( ) = 0.663. The lta of the option position is -66,300 ana further 4,800 shares shoulpurchase上一题是-61500,这题是-66300,数量增加了,那不是应该再short 4800个call么?

NO.PZ2020021205000065 因为题目中stoprice=strike price,当做short ATM Call 来看,认为lta 是 -0.5。 请问这种想法为什么不对?为什么何用BSM计算的公式结果不一样?谢谢。

请问一下为什么在第一种情况下lta计算完为-61,500,要去buy 61500 sto而不是stort stock?我以为是按照符号看long short的。谢谢

老师你好,61500是怎么算出来的?不知道要lta neutr头寸相反对冲