Risk premium的公式不是Rm-Rf吗?解析里的公式是什么呢?好像没见过,这俩有什么区别?谢谢

问题如下图:

选项:

A.

B.

C.

解释:

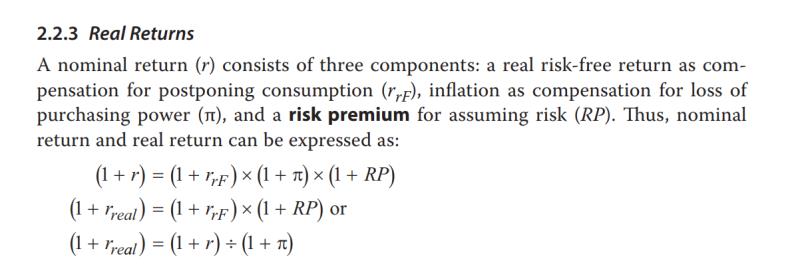

NO.PZ2015121801000137问题如下analyst observes the following historic geometric returns: The risk premium for equities is closest to: A.5.4%. B.5.5%. C.5.6%. A is correct. (1 + 0.080)/(1 + 0.0250) – 1 = 5.4% 如题,求老师帮忙解惑。另外,考点目前应该在基础课哪里?

NO.PZ2015121801000137问题如下analyst observes the following historic geometric returns: The risk premium for equities is closest to: A.5.4%. B.5.5%. C.5.6%. A is correct. (1 + 0.080)/(1 + 0.0250) – 1 = 5.4% 如题,不好意思我记得数量里有相关等式介绍,请问数量里在基础课哪里?

NO.PZ2015121801000137 问题如下 analyst observes the following historic geometric returns: The risk premium for equities is closest to: A.5.4%. B.5.5%. C.5.6%. A is correct. (1 + 0.080)/(1 + 0.0250) – 1 = 5.4% 为什么不能直接rm-rf?

NO.PZ2015121801000137 问题如下 analyst observes the following historic geometric returns: The risk premium for equities is closest to: A.5.4%. B.5.5%. C.5.6%. A is correct. (1 + 0.080)/(1 + 0.0250) – 1 = 5.4% 老师好,请问这个题目所涉及的知识点是在哪个章节哪个视频里面?

NO.PZ2015121801000137问题如下analyst observes the following historic geometric returns: The risk premium for equities is closest to: A.5.4%. B.5.5%. C.5.6%. A is correct. (1 + 0.080)/(1 + 0.0250) – 1 = 5.4% 请问这个题是这个章节的嘛?麻烦指明出处谢谢