问题如下:

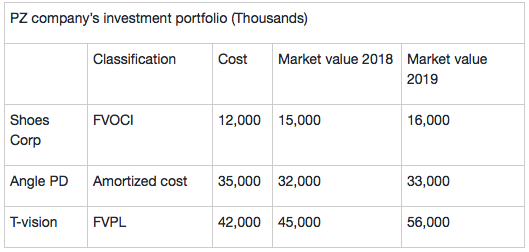

Fabian, CFA, work on the Equity investment company, Fabian is preparing a research report on PZ company, listed in HK and complies with IFRS 9. She collected a part of information from PZ company’s 2019 financial report in the following table(assume cost=par value):

If Shoes Corp had been classified as a Fair value through P/L, in 2019 the earnings before taxes would have been:

选项:

A.the same

B.1,000 higher

C.2,000 lower

解释:

B is correct.

考点:Financial asset 的会计计量

解析:

如果Shoes Corp一开始归类为Fair value through P/L , 那么unrealized G/L应该记在I.S中而不是OCI 。

在2019年 , Shoes Corp有一个1,000的unrealized gain(16,000-15,000), 因此2019年的earnings before taxes would have been higher 1,000.

老师,您好!能不能通过一个例子系统讲解一下FVOCI的会计处理,何老师课堂上讲那个案例只有从投资开始到第一个会计年度末的处理,有些地方不太明白,后面每年的处理还是和第一年的一样吗。

课上何老师讲的方法是:先计算每年的amortized cost,通过amortized cost 计算每年的interest income。用每年末的 fair value-当年末的amortized cost计算unrealized G/L。如果这样的话,2019年的unrealized G/L就不是用2019年的fair value减2018年的fair value,和这个题的解释有出入。