问题如下:

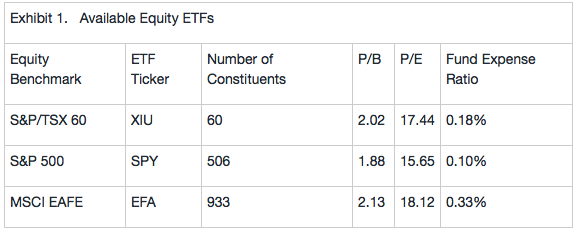

Winthrop and Tong agreethat only the existing equity investments need to be liquidated. Tong suggeststhat, as an alternative to direct equity investments, the new equity portfoliobe composed of the exchange-traded funds (ETFs) shown in Exhibit 1.

Basedon Exhibit 1 and assuming a full-replication indexing approach, the trackingerror is expected to be highest for:

选项:

A.

XIU

B.

SPY

C.

EFA

解释:

An index that contains a large number of constituents will tend tocreate higher tracking error than one with fewer constituents. Based on thenumber of constituents in the three indexes (S&P/TSX 60 has 60, S&P 500has 506, and MSCI EAFE has 933), EFA (the MSCI EAFE ETF) is expected to havethe highest tracking error. Higher expense ratios (XIU: 0.18%; SPY: 0.10%; and EFA:0.33%) also contribute to lower excess returns and higher tracking error, whichimplies that EFA has the highest expected tracking error.

看了之前的提问和回答。。。们。。 依旧一脸懵逼。。。 1.大概是懂了“n越大 tracking error越小” 但是吧。。2. 怎么理解那个U型曲线。。。是不是那个是加引号的tracking error曲线。。只是想随意聊一下trade-off呀。。 3.不然怎么判断60和933在曲线上的相对位置。。