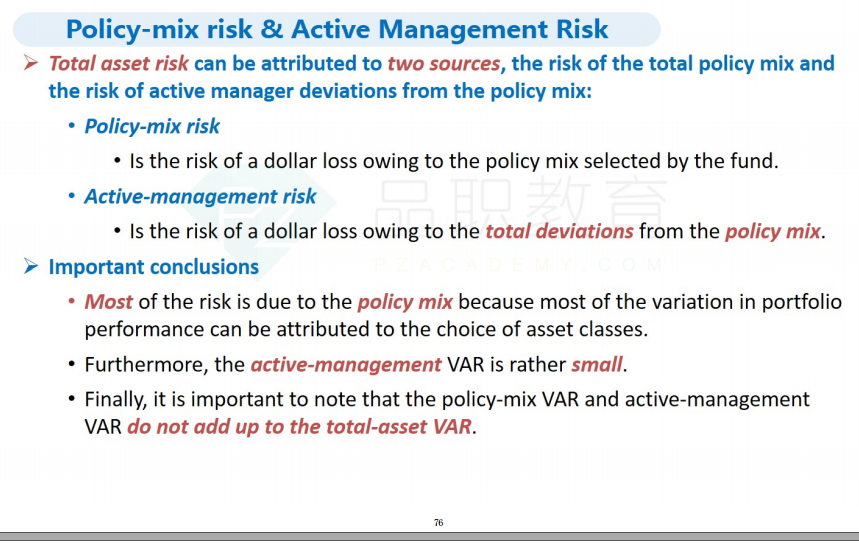

问题如下:

Which of the following is least accurate with respect to policy-mix risk and active management risk?

选项:

A. most of the risk is due to the policy mix .

B. the sum of policy-mix VAR and active-management VAR equal to the total asset VAR.

C. the active-management VAR is rather small.

D. diversification can be achieved, reducing the total asset VAR.

解释:

B is correct.

考点:policy-mix risk and active management risk

解析:首先注意题目中要求选出错误选项。选项A说法正确,大部分风险是由于policy-mix risk,因为投资组合的大部分风险可归因于资产类别的选择。选项C说法正确,与policy-mix risk相比, active management risk比较小。选项D说法正确,组合可以实现分散化效应,降低total asset VAR。policy-mix risk 与 active-management risk之间可以实现分散化效应,因此 policy-mix VAR 与 active-management VAR的和不等于total asset VAR, 选项B的说法错误,本题选B。

请问讲义上大概哪个地方提到了这个知识点啊?