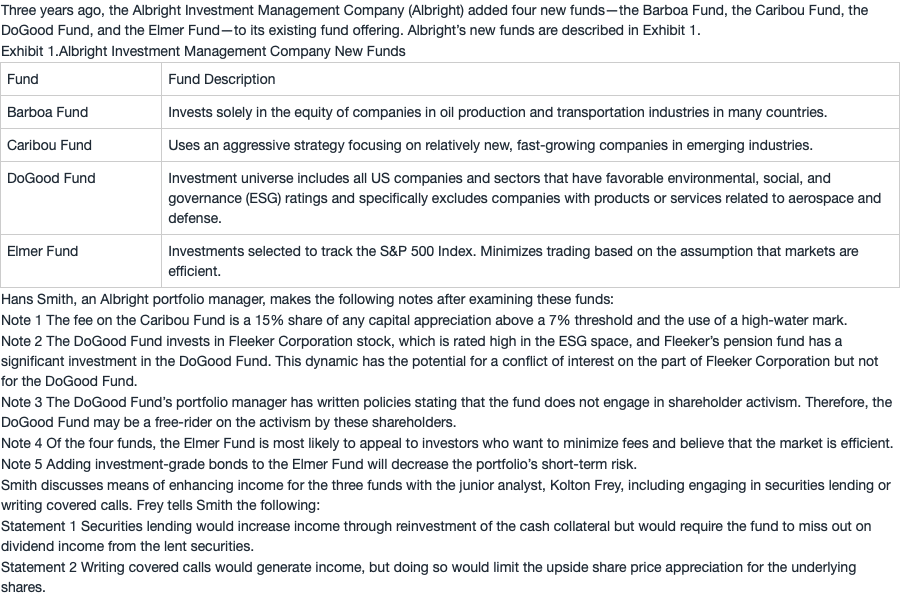

问题如下:

Which of the notes regarding the Elmer Fund is correct?

选项:

A.Only Note 4

B.Only Note 5

C.Both Note 4 and Note 5

解释:

A is correct. For passively managed portfolios, management fees are typically low because of lower direct costs of research and portfolio management relative to actively managed portfolios. Therefore, Note 4 is correct.

Note 5 is incorrect because the predictability of correlations is uncertain.

那这个和加入的bond类型有关系吗?如果是更像股票的垃圾债,结论和投资级别债券一样吗?还是说只要是bond就从【长期来看具有分散效果;短期一般有分散效果,但特殊情况如经济危机下性质一样,加大风险】这个维度考虑吗?