问题如下:

2. Using her first valuation approach and Exhibit 1, Withers’s forecast of the per share stock value of Ukon Corporation at the end of 2017 should be closest to:

选项:

A.EUR 48.

B.EUR 50.

C.EUR 51

解释:

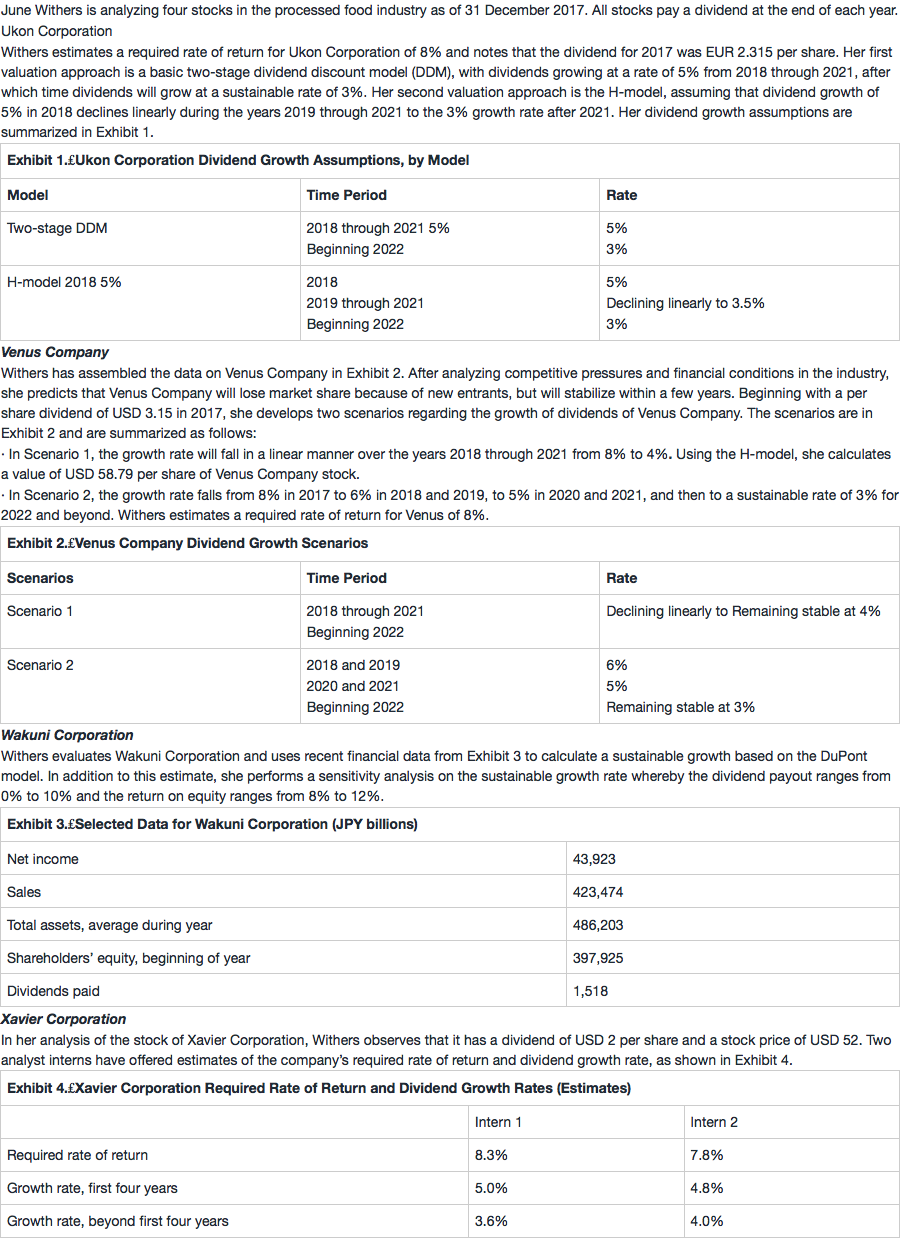

C is correct based on Withers’s assumptions applied to the dividend valuation model. The stock value as of the end of 2017 equals the present value of all future dividends in 2018 through 2021 plus the present value of the terminal value at the end of 2021. The forecasted stock value equals EUR 51.254:

57.980

60.795

44.686

2022

2.815(1.03) = 2.899

Total

51.254

The terminal value at the end of 2021 is calculated using the dividend in the first year beyond the first stage, divided by the difference between the required rate of return and the growth rate in the second stage.

Terminal value at end of 2021 = 2.815*(1.03)/ ( 0.08−0.03 ) =57.980

Div2017=2.315,但是题目中并未给出从2017年到2018年的增长率g是多少啊?那怎么就默认g=5%来计算Div2018了呢?