问题如下:

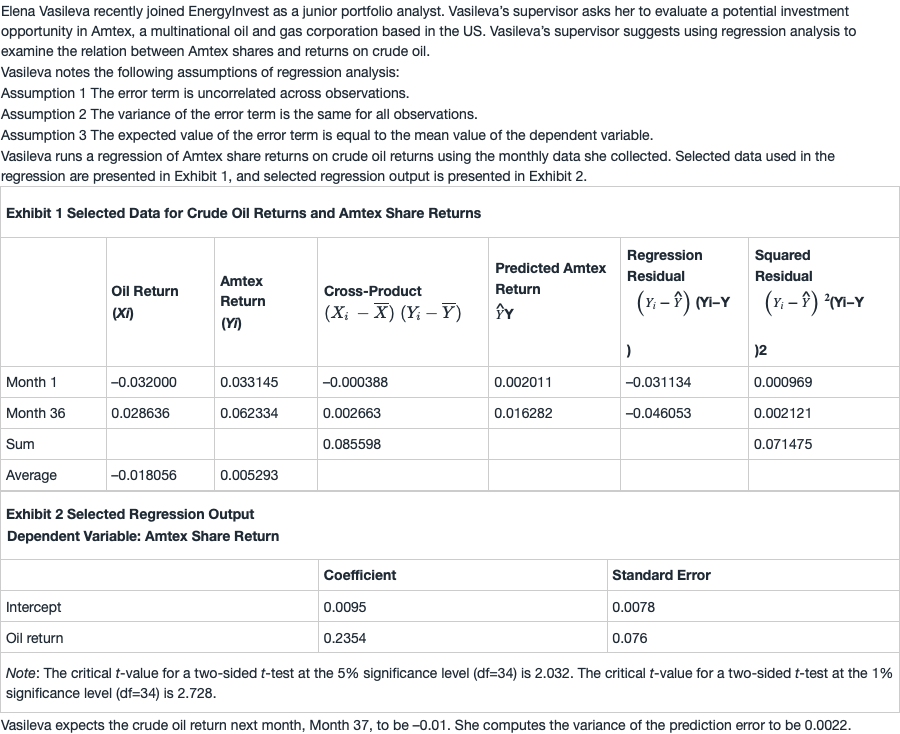

Based on Exhibit 2, Vasileva should reject the null hypothesis that:

选项:

A.the slope is less than or equal to 0.15

the intercept is less than or equal to 0

crude oil returns do not explain Amtex share returns.

解释:

C is correct. Crude oil returns explain the Amtex share returns if the slope coefficient is statistically different from zero. The slope coefficient is 0.2354 and is statistically different from zero because the absolute value of the t-statistic of 3.0974 is higher than the critical t-value of 2.032 (two-sided test for n – 2 = 34 degrees of freedom and a 5% significance level):

t-statistic =( 0.2354-0.0000)/

0.0760=3.0974

Therefore, Vasileva should reject the null hypothesis that crude oil returns do not explain Amtex share returns because the slope coefficient is statistically different from zero.

解析里面第一句先说,Crude oil returns explain the Amtex share returns if the slope coefficient is statistically different from zero. 后面的数据算出来3.0974大于1.691,拒绝原假设即H0=0,那slope coefficient is statistically different from zero,根据解析第一句话,不就是能够解释吗?为什么后面的结论又是不能解释?前后矛盾啊