问题如下:

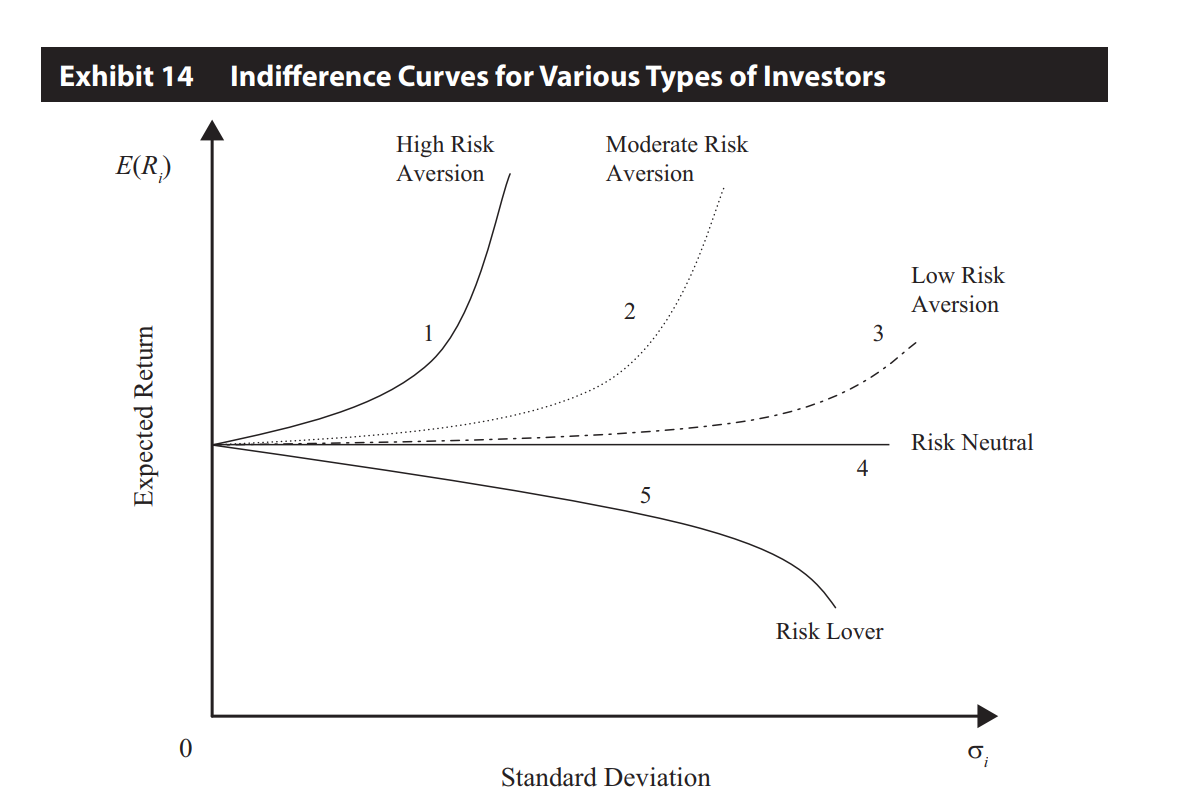

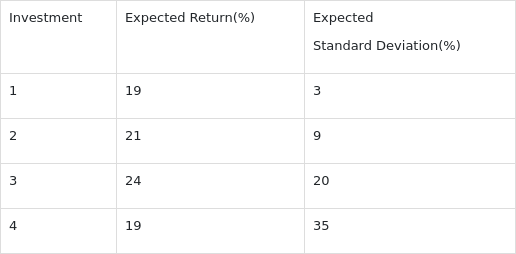

James Simone is a risk-netural investor. He will apply utility theory to choose the investment portfolio. The table shows the expected return and expected standard deviation of several investments, he is most likely to invest:

选项:

A.1

B.2

C.3

解释:

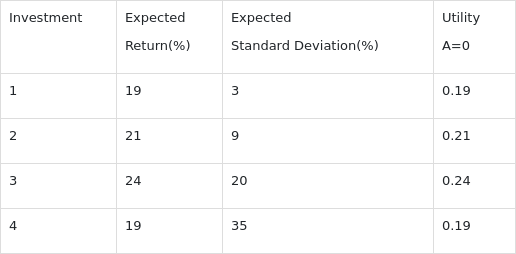

C is correct

As the investor is risk-neutral, A in the utility function is 0, risk is irrelevant to his choice, so the investment return is the only factor that should be considered. Therefore, Investment 3 has the highest return.

老师,求一下帮助,谢谢