问题如下图:

选项:

A.

B.

C.

D.

解释:

请问C选项的remaining maturity不是应该是快到期的时间么?为什么解释里面直接把它当成两个不一样maturity的option来看了?

请问C选项的remaining maturity不是应该是快到期的时间么?为什么解释里面直接把它当成两个不一样maturity的option来看了?

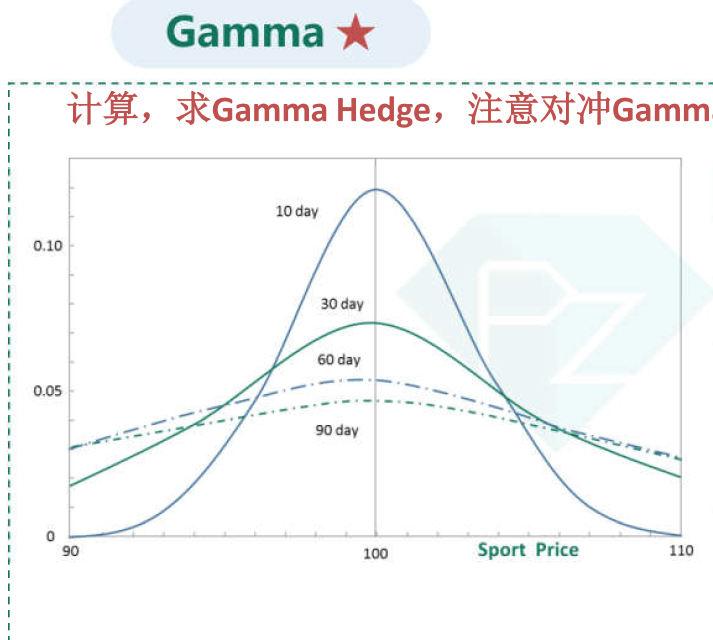

NO.PZ2016082404000035 问题如下 Whiof the following statements is incorrect? The vega of a European-style call option is highest when the option is at-the-money. The lta of a European-style put option moves towarzero the priof the unrlying storises. The gamma of at-the-money European-style option ten to increase the remaining maturity of the option creases. Compareto at-the-money European-style call option, out-of-the- money European-style option with the same strike prianremaining maturity ha greater negative value for theta. ANSWER: D Vega is highest for ATM Europeoptions, so statement A is correct. lta is negative and moves to zero S increases, so statement B is correct. Gamma increases the maturity of ATM option creases, so statement C is correct. Theta is greater (in absolute value) for short-term ATM options, so statement is incorrect. C,随着到期日临近,the money 的gamma上升;in/out the money 的gamma下降。请分别一下为什么?

NO.PZ2016082404000035问题如下 Whiof the following statements is incorrect? The vega of a European-style call option is highest when the option is at-the-money. The lta of a European-style put option moves towarzero the priof the unrlying storises. The gamma of at-the-money European-style option ten to increase the remaining maturity of the option creases. Compareto at-the-money European-style call option, out-of-the- money European-style option with the same strike prianremaining maturity ha greater negative value for theta. ANSWER: D Vega is highest for ATM Europeoptions, so statement A is correct. lta is negative and moves to zero S increases, so statement B is correct. Gamma increases the maturity of ATM option creases, so statement C is correct. Theta is greater (in absolute value) for short-term ATM options, so statement is incorrect. 关于答案错误的原因Theta is greater (in absolute value) for short-term ATM options, so statement is incorrect.我觉得和表述的不是一回事,我对理解是对于theta,无论是call还是put,都小于0,ATM时|theta|最大,OTM和ITM时,with the same strike prianremaining maturity,|theta|更小。

Whiof the following statements is incorrect? The vega of a European-style call option is highest when the option is at-the-money. The lta of a European-style put option moves towarzero the priof the unrlying storises. The gamma of at-the-money European-style option ten to increase the remaining maturity of the option creases. Compareto at-the-money European-style call option, out-of-the- money European-style option with the same strike prianremaining maturity ha greater negative value for thet ANSWER: Vega is highest for ATM Europeoptions, so statement A is correct. lta is negative anmoves to zero S increases, so statement B is correct. Gamma increases the maturity of ATM option creases, so statement C is correct. Theta is greater (in absolute value) for short-term ATM options, so statement is incorrect. 老师您好,解析里说 Theta is greater (in absolute value) for short-term ATM options, 这个没错。可是的是 a greater negative value for theta啊,这也是对的啊,又不是比较绝对值之后值的大小。是我英文理解的问题吗?

是理解不了