问题如下:

Based on Exhibit 1, Olabudo should calculate a prediction interval for the actual US CPI closest to:

选项:

A.2.7506 to 2.7544

2.7521 to 2.7529

2.7981 to 2.8019.

解释:

A is correct.

只有一个答案没有具体解题过程。

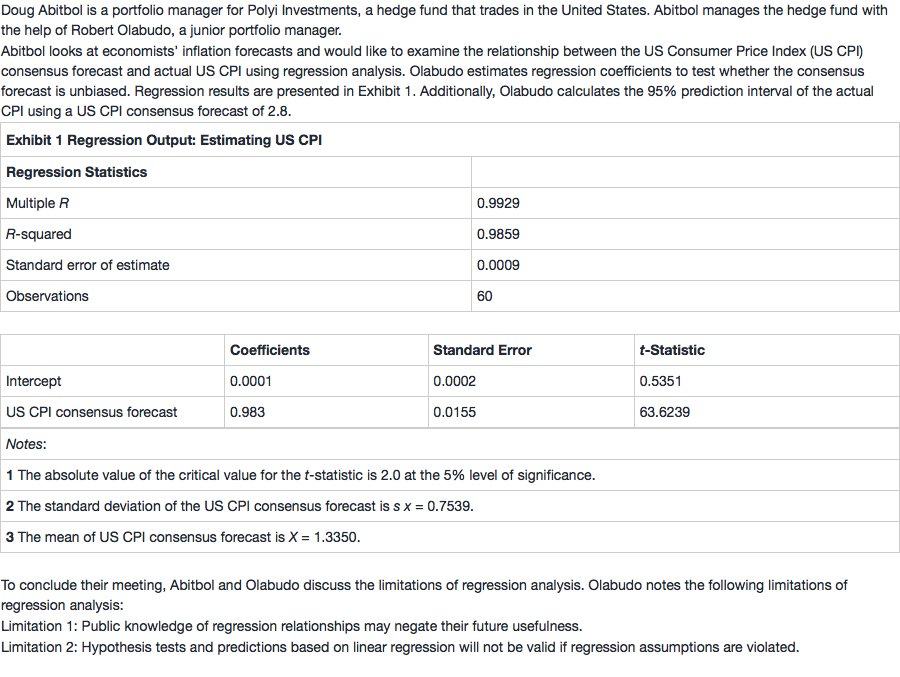

NO.PZ201512020300000902 为什么不可以用文中表格给出的stanrerror

NO.PZ201512020300000902 老师,公式里的S,为什么代入得是0.7539,而不是0.0155?

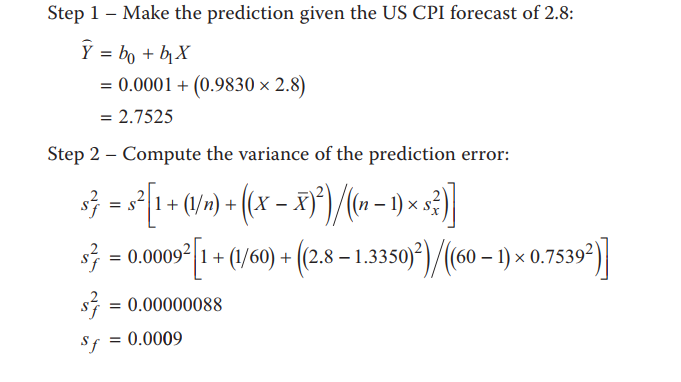

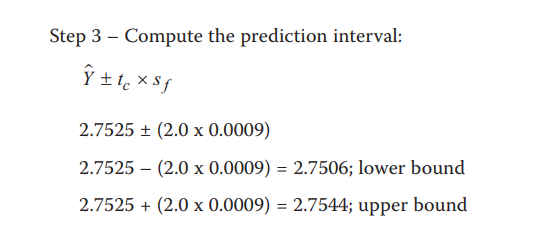

NO.PZ201512020300000902 2.7521 to 2.7529 2.7981 to 2.8019. A is correct. The prection intervfor inflation is calculatein three steps: Step 1 – Make the prection given the US CPI forecast of 2.8: Y^=b0+b1X=0.0001+(0.9830×2.8)=2.7525\wihat{Y}=b_0+b_1X=0.0001+(0.9830×2.8)=2.7525Y =b0+b1X=0.0001+(0.9830×2.8)=2.7525 Step 2 – Compute the varianof the prection error: sf2=s2[1+1n+(X−X‾)2(n−1)×sx2]s^2_f=s^2[1+\frac{1}{n}+\frac{{(X-\overline{X})}^2}{(n-1)\times{s^2_x}}]sf2=s2[1+n1+(n−1)×sx2(X−X)2] sf2=0.00092[1+160+(2.8−1.3350)2(60−1)×0.75392]=0.00000088s^2_f=0.0009^2[1+\frac{1}{60}+\frac{{(2.8-1.3350)}^2}{(60-1)\times{0.7539^2}}]=0.00000088sf2=0.00092[1+601+(60−1)×0.75392(2.8−1.3350)2]=0.00000088 sf=0.0009s_f=0.0009sf=0.0009 Step 3 – Compute the prection interval: Y^±tc×sf\wihat{Y}\pm{t_c}\times{s_f}Y ±tc×sf 2.7525±(2.0×0.0009)2.7525\pm{(2.0\times0.0009)}2.7525±(2.0×0.0009) 2.7525–(2.0×0.0009)=2.75062.7525–(2.0\times0.0009)=2.75062.7525–(2.0×0.0009)=2.7506; lower boun2.7525+(2.0×0.0009)=2.75442.7525+(2.0\times0.0009)=2.75442.7525+(2.0×0.0009)=2.7544; upper bounSo, given the US CPI forecast of 2.8, the 95% prection intervis 2.7506 to 2.7544. 这个题目的考点没有明白..而且计算好想很复杂

NO.PZ201512020300000902 求第二步骤的公式也是需要背下来的么?

2.7521 to 2.7529 2.7981 to 2.8019. A is correct. The prection intervfor inflation is calculatein three steps: Step 1 – Make the prection given the US CPI forecast of 2.8: Y^=b0+b1X=0.0001+(0.9830×2.8)=2.7525\wihat{Y}=b_0+b_1X=0.0001+(0.9830×2.8)=2.7525Y =b0+b1X=0.0001+(0.9830×2.8)=2.7525 Step 2 – Compute the varianof the prection error: sf2=s2[1+1n+(X−X‾)2(n−1)×sx2]s^2_f=s^2[1+\frac{1}{n}+\frac{{(X-\overline{X})}^2}{(n-1)\times{s^2_x}}]sf2=s2[1+n1+(n−1)×sx2(X−X)2] sf2=0.00092[1+160+(2.8−1.3350)2(60−1)×0.75392]=0.00000088s^2_f=0.0009^2[1+\frac{1}{60}+\frac{{(2.8-1.3350)}^2}{(60-1)\times{0.7539^2}}]=0.00000088sf2=0.00092[1+601+(60−1)×0.75392(2.8−1.3350)2]=0.00000088 sf=0.0009s_f=0.0009sf=0.0009 Step 3 – Compute the prection interval: Y^±tc×sf\wihat{Y}\pm{t_c}\times{s_f}Y ±tc×sf 2.7525±(2.0×0.0009)2.7525\pm{(2.0\times0.0009)}2.7525±(2.0×0.0009) 2.7525–(2.0×0.0009)=2.75062.7525–(2.0\times0.0009)=2.75062.7525–(2.0×0.0009)=2.7506; lower boun2.7525+(2.0×0.0009)=2.75442.7525+(2.0\times0.0009)=2.75442.7525+(2.0×0.0009)=2.7544; upper bounSo, given the US CPI forecast of 2.8, the 95% prection intervis 2.7506 to 2.7544. 老师好,请问一下讲义里Sf的公式是直接用SEE的,题目里SEE是0.0009,答案解析中为何还要把0.0009 平方后再去和后面去相乘