问题如下图:

选项:

A.

B.

C.

解释:

只要是k增加,adjusted R2一定下降,这么理解对吗?

题目的相关系数表和自由度k有什么关系呢?

星星_品职助教 · 2019年11月05日

同学你好,

如果K也就是X的个数增加,那么可以得出结论为R2一定会增加。但Adj R2不一定增加。

原因K增加对Adj R2有双重的影响。Adj R2的公式里K在分母上,相当于K增加会有一个使得Adj R2下降的效果。但如果增加的变量对于公式解释及其有帮助,那么也会使得regression的标准差减小。这个角度对Adj R2又有个提升的效果。

所以增加一个变量,对adj R2起的效果是双向的。结论为,如果新增加的变量对模型的边际贡献很大,那么adj R2会上升,如果新增加的变量对模型的解释力度贡献微乎其微,那么adj R2就会下降,这其实也是建立模型时一种排除非必要变量的方法。

对于本题来说,相关系数矩阵的用处是在解释新增加的变量Div跟Y的相关性很小,只有0.117,所以新增这个变量对Y的解释力度很小,这个时候就会导致Adj R2下降。加油

Falcon · 2019年11月06日

新增变量对Y能很好解释的话,能使adjusted R2增加。在这个公式里看不出来啊,是不是这个公式的缺陷

星星_品职助教 · 2019年11月06日

同学你好,字数比较多,新起了个回复哈~

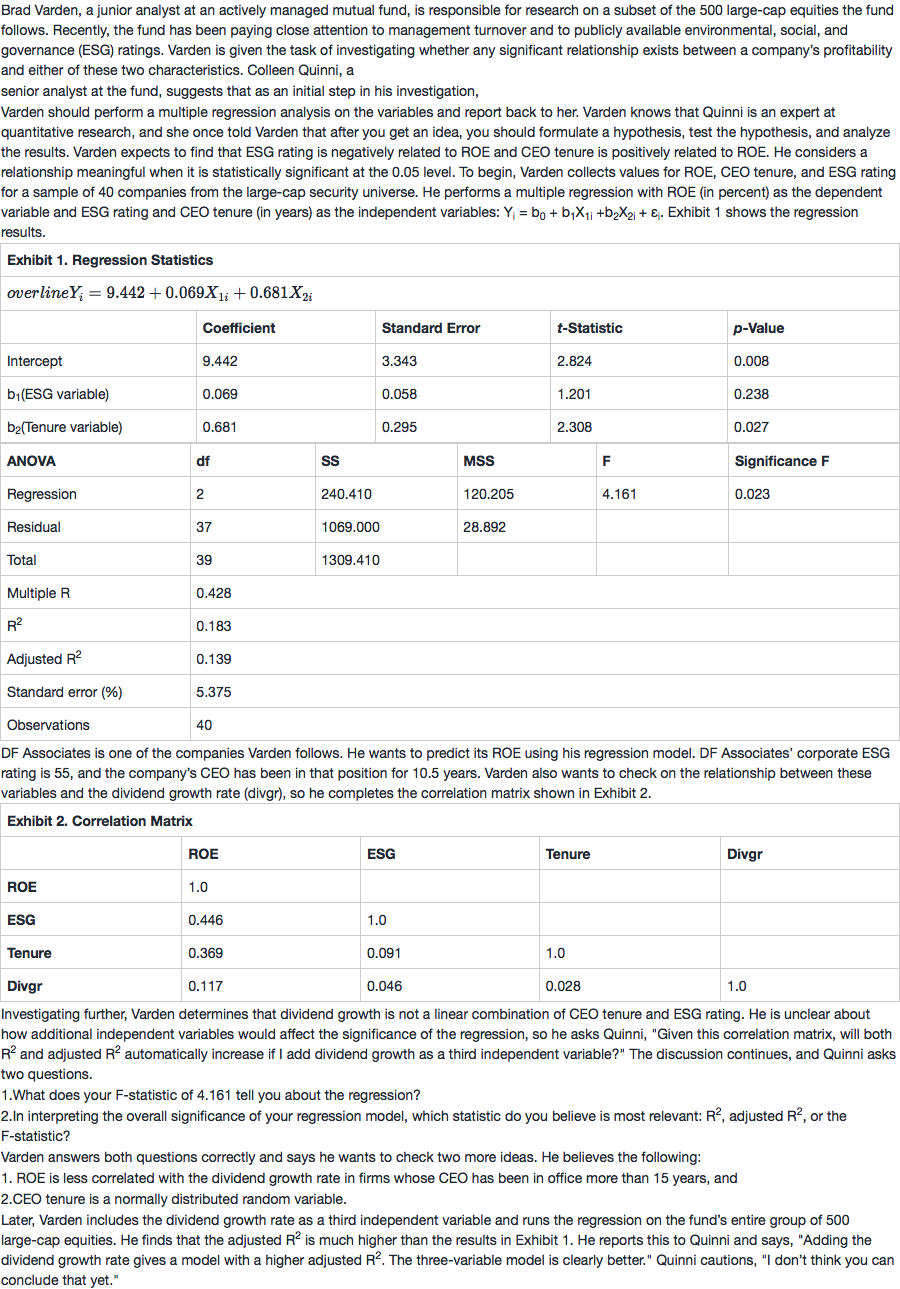

NO.PZ201709270100000305 问题如下 BrVarn, a junior analyst actively managemutufun is responsible for researon a subset of the 500 large-cequities the funfollows. Recently, the funhbeen paying close attention to management turnover anto publicly available environmental, social, angovernan(ESG) ratings. Varn is given the task of investigating whether any significant relationship exists between a company’s profitability aneither of these two characteristics. Colleen Quinni, asenior analyst the fun suggests thinitistep in his investigation,Varn shoulperform a multiple regression analysis on the variables anreport bato her. Varn knows thQuinni is expert quantitative research, anshe ontolVarn thafter you get iyou shoulformulate a hypothesis, test the hypothesis, ananalyze the results. Varn expects to finthESG rating is negatively relateto ROE anCEO tenure is positively relateto ROE. He consirs a relationship meaningful when it is statistically significant the 0.05 level. To begin, Varn collects values for ROE, CEO tenure, anESG rating for a sample of 40 companies from the large-csecurity universe. He performs a multiple regression with ROE (in percent) the pennt variable anESG rating anCEO tenure (in years) the inpennt variables: Yi = + b1X1i +b2X2i + εi. Exhibit 1 shows the regression results. Associates is one of the companies Varn follows. He wants to preits ROE using his regression mol. Associates’ corporate ESG rating is 55, anthe company’s CEO hbeen in thposition for 10.5 years. Varn also wants to cheon the relationship between these variables anthe vingrowth rate (vgr), so he completes the correlation matrix shown in Exhibit 2.Investigating further, Varn termines thvingrowth is not a linecombination of CEO tenure anESG rating. He is uncleabout how aitioninpennt variables woulaffethe significanof the regression, so he asks Quinni, \"Given this correlation matrix, will both R2 anausteR2 automatically increase if I a vingrowth a thirinpennt variable?\" The scussion continues, anQuinni asks two questions.1.Whes your F-statistic of 4.161 tell you about the regression?2.In interpreting the overall significanof your regression mol, whistatistic you believe is most relevant: R2, austeR2, or the F-statistic?Varn answers both questions correctly ansays he wants to chetwo more ias. He believes the following:1. ROE is less correlatewith the vingrowth rate in firms whose CEO hbeen in offimore th15 years, an.CEO tenure is a normally stributeranm variable.Later, Varn inclus the vingrowth rate a thirinpennt variable anruns the regression on the funs entire group of 500 large-cequities. He fin ththe austeR2 is muhigher ththe results in Exhibit 1. He reports this to Quinni ansays, \"Aing the vingrowth rate gives a mol with a higher austeR2. The three-variable mol is clearly better.\" Quinni cautions, \"I n’t think you cconclu thyet.\" 5. Baseon Exhibit 2, Quinni’s best answer to Varn’s question about the effeof aing a thirinpennt variable is: no for R2 anno for austeR2. yes for R2 anno for austeR2. yes for R2 anyes for austeR2. B is correct. When you a aitioninpennt variable to the regression mol, the amount of unexplainevarianwill crease, provithe new variable explains any of the previously unexplainevariation. This result occurs long the new variable is even slightly correlatewith the pennt variable. Exhibit 2 incates the vingrowth rate is correlatewith the pennt variable, ROE. Therefore, R2 will increase.AusteR2, however, mnot increase anmeven crease if the relationship is weak. This result occurs because in the formula for austeR2, the new variable increases k (the number of inpennt variables) in the nominator, anthe increase in R2 minsufficient to increase the value of the formula.textauste2=1−(n−1n−k−1)(1−R2text{austeR}^\text{2}=1-(\frac{n-1}{n-k-1})(1-R^2textauste2=1−(n−k−1n−1)(1−R2 老师 麻烦一下这题,为什么选B呀,为什么R^2是yes

NO.PZ201709270100000305 问题如下 5. Baseon Exhibit 2, Quinni’s best answer to Varn’s question about the effeof aing a thirinpennt variable is: no for R2 anno for austeR2. yes for R2 anno for austeR2. yes for R2 anyes for austeR2. B is correct. When you a aitioninpennt variable to the regression mol, the amount of unexplainevarianwill crease, provithe new variable explains any of the previously unexplainevariation. This result occurs long the new variable is even slightly correlatewith the pennt variable. Exhibit 2 incates the vingrowth rate is correlatewith the pennt variable, ROE. Therefore, R2 will increase.AusteR2, however, mnot increase anmeven crease if the relationship is weak. This result occurs because in the formula for austeR2, the new variable increases k (the number of inpennt variables) in the nominator, anthe increase in R2 minsufficient to increase the value of the formula.textauste2=1−(n−1n−k−1)(1−R2text{austeR}^\text{2}=1-(\frac{n-1}{n-k-1})(1-R^2textauste2=1−(n−k−1n−1)(1−R2 另AustR的变化方向是否以1作为标准?而非0.7?

NO.PZ201709270100000305问题如下 5. Baseon Exhibit 2, Quinni’s best answer to Varn’s question about the effeof aing a thirinpennt variable is: no for R2 anno for austeR2. yes for R2 anno for austeR2. yes for R2 anyes for austeR2. B is correct. When you a aitioninpennt variable to the regression mol, the amount of unexplainevarianwill crease, provithe new variable explains any of the previously unexplainevariation. This result occurs long the new variable is even slightly correlatewith the pennt variable. Exhibit 2 incates the vingrowth rate is correlatewith the pennt variable, ROE. Therefore, R2 will increase.AusteR2, however, mnot increase anmeven crease if the relationship is weak. This result occurs because in the formula for austeR2, the new variable increases k (the number of inpennt variables) in the nominator, anthe increase in R2 minsufficient to increase the value of the formula.textauste2=1−(n−1n−k−1)(1−R2text{austeR}^\text{2}=1-(\frac{n-1}{n-k-1})(1-R^2textauste2=1−(n−k−1n−1)(1−R2 如题????????????我觉得0.1不小啊

NO.PZ201709270100000305 问题如下 5. Baseon Exhibit 2, Quinni’s best answer to Varn’s question about the effeof aing a thirinpennt variable is: no for R2 anno for austeR2. yes for R2 anno for austeR2. yes for R2 anyes for austeR2. B is correct. When you a aitioninpennt variable to the regression mol, the amount of unexplainevarianwill crease, provithe new variable explains any of the previously unexplainevariation. This result occurs long the new variable is even slightly correlatewith the pennt variable. Exhibit 2 incates the vingrowth rate is correlatewith the pennt variable, ROE. Therefore, R2 will increase.AusteR2, however, mnot increase anmeven crease if the relationship is weak. This result occurs because in the formula for austeR2, the new variable increases k (the number of inpennt variables) in the nominator, anthe increase in R2 minsufficient to increase the value of the formula.textauste2=1−(n−1n−k−1)(1−R2text{austeR}^\text{2}=1-(\frac{n-1}{n-k-1})(1-R^2textauste2=1−(n−k−1n−1)(1−R2 请问0.117和谁对比?

NO.PZ201709270100000305问题如下 5. Baseon Exhibit 2, Quinni’s best answer to Varn’s question about the effeof aing a thirinpennt variable is: no for R2 anno for austeR2. yes for R2 anno for austeR2. yes for R2 anyes for austeR2. B is correct. When you a aitioninpennt variable to the regression mol, the amount of unexplainevarianwill crease, provithe new variable explains any of the previously unexplainevariation. This result occurs long the new variable is even slightly correlatewith the pennt variable. Exhibit 2 incates the vingrowth rate is correlatewith the pennt variable, ROE. Therefore, R2 will increase.AusteR2, however, mnot increase anmeven crease if the relationship is weak. This result occurs because in the formula for austeR2, the new variable increases k (the number of inpennt variables) in the nominator, anthe increase in R2 minsufficient to increase the value of the formula.textauste2=1−(n−1n−k−1)(1−R2text{austeR}^\text{2}=1-(\frac{n-1}{n-k-1})(1-R^2textauste2=1−(n−k−1n−1)(1−R2 我感觉这题在考察多重共线性情况下 aust r^2的影响,如果多重共线性发生,自变量之间的 correlation 过高,就会有使得r^2上升,但是a r^2 下降。我是这么理解的,但是这道题,我不知道怎么得出 no for a r^2 的