问题如下图:

选项:

A.

B.

C.

D.

解释:

老师你好,请问I这句话为什么对?可以详细解释一下吗?谢谢

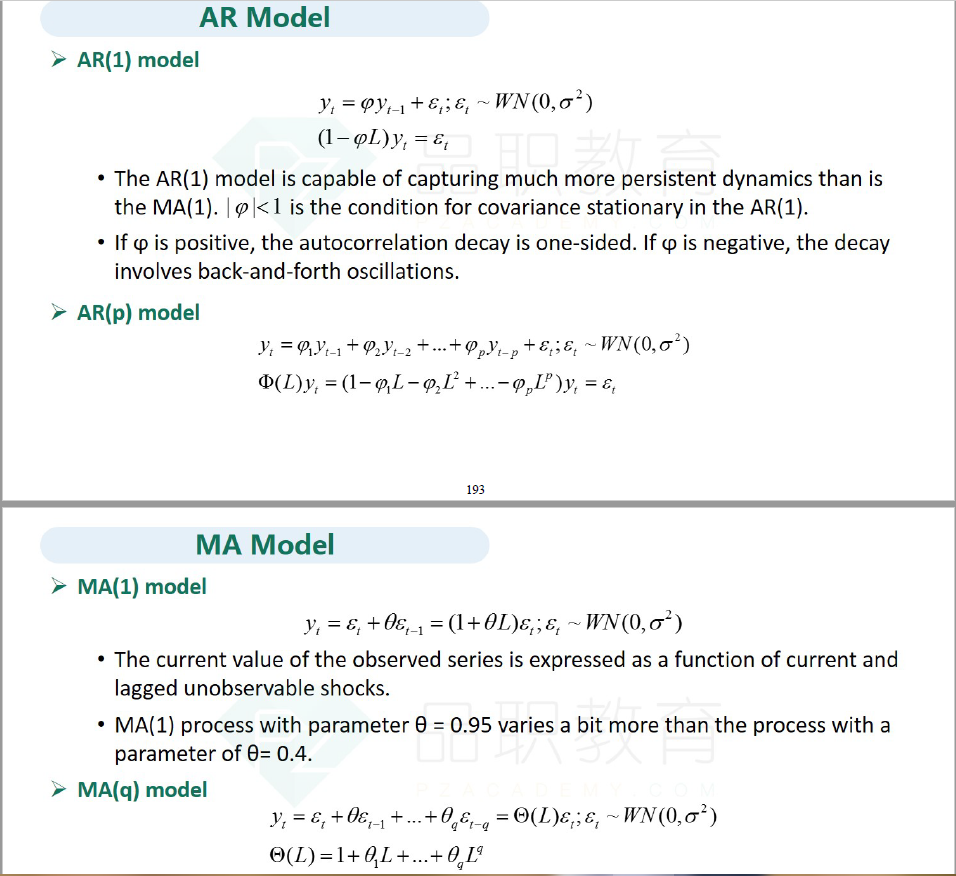

NO.PZ2019040801000060问题如下 The following statements are about the autoregressive moving average process. Whiof them is correct?I. It combines the laggeunobservable ranm shoof the MA process with the observelaggetime series of the process.II. It involves autocorrelations whicgraally.A.I only.B.II only.C.Both I anII.Neither I nor II.C is correct.考点Autoregressive Moving Average Process 解析这两个结论都是正确的,是autoregressive moving average process的性质。看不懂这个题,能翻译一下吗

NO.PZ2019040801000060 问题如下 The following statements are about the autoregressive moving average process. Whiof them is correct?I. It combines the laggeunobservable ranm shoof the MA process with the observelaggetime series of the process.II. It involves autocorrelations whicgraally. A.I only. B.II only. C.Both I anII. Neither I nor II. C is correct.考点Autoregressive Moving Average Process 解析这两个结论都是正确的,是autoregressive moving average process的性质。 ARMA process 中的MA部分不是只影响一个laggeshock吗?那为什么可以说It combines the laggeunobservable ranm shoof the MA process?AR部分不是考虑到了所有的shocks吗?为什么说它的影响只有observelaggetime series?请问statement I说的是什么意思?其中的observeunobservable该怎么理解?

NO.PZ2019040801000060问题如下The following statements are about the autoregressive moving average process. Whiof them is correct?I. It combines the laggeunobservable ranm shoof the MA process with the observelaggetime series of the process.II. It involves autocorrelations whicgraally.A.I only.B.II only.C.Both I anII.Neither I nor II.C is correct.考点Autoregressive Moving Average Process 解析这两个结论都是正确的,是autoregressive moving average process的性质。MA的ACF不应该是cut off的吗?

NO.PZ2019040801000060 MA不是针对shock的模型么?滞后项是?

NO.PZ2019040801000060 没有明白unobsevable