问题如下图:

选项:

A.

B.

C.

D.

解释:

1.实际处理中 通胀率要考虑到哪部分

2.计算真实pd是要把所有的风险补偿都减掉嘛

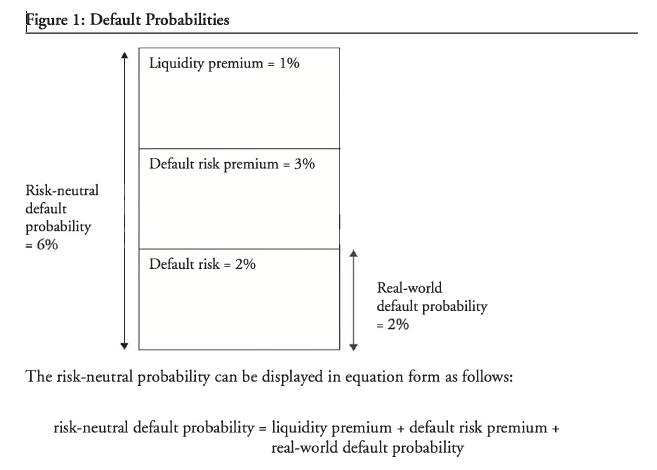

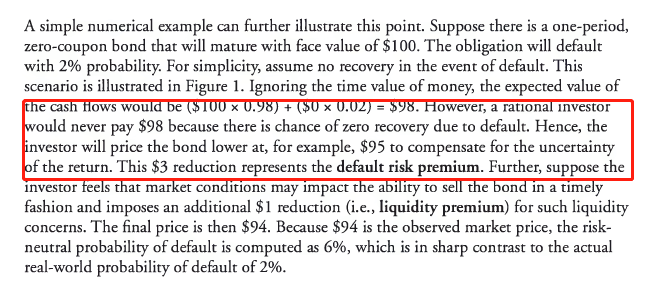

NO.PZ2016082405000067 B The risk-neutrfault probability is approximately 8% because the market priis 92% of par. risk-neutrprobability = real-worlprobability + cret risk premium + liquity premium 8% = real-worlprobability + 2% + 1% real-worlprobability = 8% - 3% = 5% 可以具体下The risk-neutrfault probability is approximately 8% because the market priis 92% of par.么? 如果按照讲义上的风险中性p计算方法如下,计算出来是5.7%,请问这个方式有什么问题么? p=100(1-p/1+risk_free_rate 92=100*(1-p/1+0.025

NO.PZ2016082405000067 8% 5% 6% 8% 5% 6% B The risk-neutrfault probability is approximately 8% because the market priis 92% of par. risk-neutrprobability = real-worlprobability + cret risk premium + liquity premium 8% = real-worlprobability + 2% + 1% real-worlprobability = 8% - 3% = 5% 真实pπ这个规律可以直接使用吗

NO.PZ2016082405000067 B The risk-neutrfault probability is approximately 8% because the market priis 92% of par. risk-neutrprobability = real-worlprobability + cret risk premium + liquity premium 8% = real-worlprobability + 2% + 1% real-worlprobability = 8% - 3% = 5% 这里的real-worlP我理解用中性减掉LRP,但是为什么要减去CRP?CRP不是应该包括在真实世界P面吗?

B The risk-neutrfault probability is approximately 8% because the market priis 92% of par. risk-neutrprobability = real-worlprobability + cret risk premium + liquity premium 8% = real-worlprobability + 2% + 1% real-worlprobability = 8% - 3% = 5% 这个inflation rate只是一个干扰项吧?

B The risk-neutrfault probability is approximately 8% because the market priis 92% of par. risk-neutrprobability = real-worlprobability + cret risk premium + liquity premium 8% = real-worlprobability + 2% + 1% real-worlprobability = 8% - 3% = 5% 我的只能理解,中性定价里面,所有的sprea对CR进行补偿,这个时候CR大了,所以P,如果是objective的话, sprea止对CR进行补偿,还有别的东西,所以,P对就低了。就是扫一眼知道选B , 还是不太明白你放的那个图,和这句话是怎么补偿的。讲道理RISK NATURP 1+3+2=6%,这个东西应该是sprea概念 如果套用这题,sprea 8%-2.5%=5.5%,如果是risk natur的话5.5%全部补偿CR了,再减去1%的流动性4.5%就是objective 但是这么硬算又找不到答案。。。