问题如下图:看了一堆解释,到底102.36是不是等于flat price?一会说是一会说不是的。

选项:

A.

B.

C.

解释:

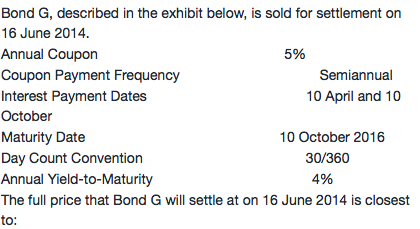

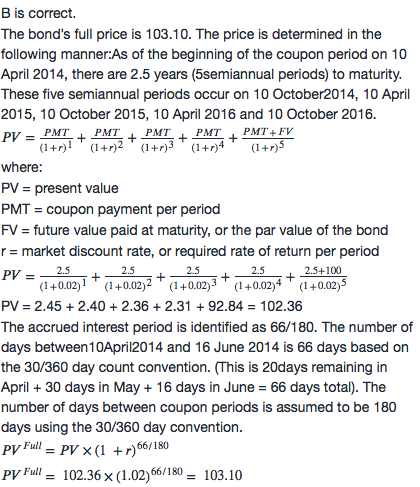

NO.PZ2016031001000069 问题如下 BonG, scribein the exhibit below, is solfor settlement on 16 June 2014.AnnuCoupon 5%Coupon Payment Frequen SemiannualInterest Payment tes 10 April an10 OctoberMaturity te 10 October 2016y Count Convention 30/360AnnuYielto-Maturity 4%The full prithBonG will settle on 16 June 2014 is closest to: A.102.36. B.103.10. C.103.65. B is correct.The bons full priis 103.10. The priis terminein the following manner:of the beginning of the coupon perioon 10 April 2014, there are 2.5 years (5semiannuperio) to maturity. These five semiannuperio occur on 10 October2014, 10 April 2015, 10 October 2015, 10 April 2016 an10 October 2016. PV=PMT(1+r)1+PMT(1+r)2+PMT(1+r)3+PMT(1+r)4+PMT+FV(1+r)5PV=\frac{PMT}{{(1+r)}^1}+\frac{PMT}{{(1+r)}^2}+\frac{PMT}{{(1+r)}^3}+\frac{PMT}{{(1+r)}^4}+\frac{PMT+FV}{{(1+r)}^5}PV=(1+r)1PMT+(1+r)2PMT+(1+r)3PMT+(1+r)4PMT+(1+r)5PMT+FVPV=2.5(1+0.02)1+2.5(1+0.02)2+2.5(1+0.02)3+2.5(1+0.02)4+2.5+100(1+0.02)5PV=\frac{2.5}{{(1+0.02)}^1}+\frac{2.5}{{(1+0.02)}^2}+\frac{2.5}{{(1+0.02)}^3}+\frac{2.5}{{(1+0.02)}^4}+\frac{2.5\text{+}100}{{(1+0.02)}^5}PV=(1+0.02)12.5+(1+0.02)22.5+(1+0.02)32.5+(1+0.02)42.5+(1+0.02)52.5+100PV = 2.45 + 2.40 + 2.36 + 2.31 + 92.84 = 102.36The accrueinterest periois intifie66/180. The number of ys between10April2014 an16 June 2014 is 66 ys baseon the 30/360 y count convention. (This is 20ys remaining in April + 30 ys in M+ 16 ys in June = 66 ys total). The number of ys between coupon perio is assumeto 180 ys using the 30/360 y convention.PVFull=PV×(1 +r)66/180PV^{Full}=PV\times{(1\text{ }+r)}^{66/180}PVFull=PV×(1 +r)66/180PVFull= 102.36×(1.02)66/180= 103.10PV^{Full}=\text{ }102.36\times{(1.02)}^{66/180}=\text{ }103.10PVFull= 102.36×(1.02)66/180= 103.10考点flpri full price解析首先,我们将未来五笔现金流折现到2014.4.10,得到现值之和为102.36。N=5,PMT=2.5,I/Y=2,FV=100,求得PV=102.36然后再将这个数值复利到2014.6.16,得到full price为103.10,故B正确。我们之所以没有直接将未来五笔现金流折到2014.6.16,是因为五笔现金流的时间间隔不同,后面四笔现金流时间间隔是半年,而从6.16到10.10之间并不是半年。因此现金流就不是一个年金的形式,我们就没有办法用计算器直接求PV了。 为什么要用半年期的利率来把4月10号的PV折算到6月16号。也就是, 为什么是用半年期对应的(1+2%)^(66/180), 而不是用annual的数据, (1+4%)^(66/360)

NO.PZ2016031001000069 问题如下 BonG, scribein the exhibit below, is solfor settlement on 16 June 2014.AnnuCoupon 5%Coupon Payment Frequen SemiannualInterest Payment tes 10 April an10 OctoberMaturity te 10 October 2016y Count Convention 30/360AnnuYielto-Maturity 4%The full prithBonG will settle on 16 June 2014 is closest to: A.102.36. B.103.10. C.103.65. B is correct.The bons full priis 103.10. The priis terminein the following manner:of the beginning of the coupon perioon 10 April 2014, there are 2.5 years (5semiannuperio) to maturity. These five semiannuperio occur on 10 October2014, 10 April 2015, 10 October 2015, 10 April 2016 an10 October 2016. PV=PMT(1+r)1+PMT(1+r)2+PMT(1+r)3+PMT(1+r)4+PMT+FV(1+r)5PV=\frac{PMT}{{(1+r)}^1}+\frac{PMT}{{(1+r)}^2}+\frac{PMT}{{(1+r)}^3}+\frac{PMT}{{(1+r)}^4}+\frac{PMT+FV}{{(1+r)}^5}PV=(1+r)1PMT+(1+r)2PMT+(1+r)3PMT+(1+r)4PMT+(1+r)5PMT+FVPV=2.5(1+0.02)1+2.5(1+0.02)2+2.5(1+0.02)3+2.5(1+0.02)4+2.5+100(1+0.02)5PV=\frac{2.5}{{(1+0.02)}^1}+\frac{2.5}{{(1+0.02)}^2}+\frac{2.5}{{(1+0.02)}^3}+\frac{2.5}{{(1+0.02)}^4}+\frac{2.5\text{+}100}{{(1+0.02)}^5}PV=(1+0.02)12.5+(1+0.02)22.5+(1+0.02)32.5+(1+0.02)42.5+(1+0.02)52.5+100PV = 2.45 + 2.40 + 2.36 + 2.31 + 92.84 = 102.36The accrueinterest periois intifie66/180. The number of ys between10April2014 an16 June 2014 is 66 ys baseon the 30/360 y count convention. (This is 20ys remaining in April + 30 ys in M+ 16 ys in June = 66 ys total). The number of ys between coupon perio is assumeto 180 ys using the 30/360 y convention.PVFull=PV×(1 +r)66/180PV^{Full}=PV\times{(1\text{ }+r)}^{66/180}PVFull=PV×(1 +r)66/180PVFull= 102.36×(1.02)66/180= 103.10PV^{Full}=\text{ }102.36\times{(1.02)}^{66/180}=\text{ }103.10PVFull= 102.36×(1.02)66/180= 103.10考点flpri full price解析首先,我们将未来五笔现金流折现到2014.4.10,得到现值之和为102.36。N=5,PMT=2.5,I/Y=2,FV=100,求得PV=102.36然后再将这个数值复利到2014.6.16,得到full price为103.10,故B正确。我们之所以没有直接将未来五笔现金流折到2014.6.16,是因为五笔现金流的时间间隔不同,后面四笔现金流时间间隔是半年,而从6.16到10.10之间并不是半年。因此现金流就不是一个年金的形式,我们就没有办法用计算器直接求PV了。 N=5,PMT=2.5,I/Y=2,FV=100,这种情况下如果把FV输入为-100,算出的PV就是78.789,请问是为什么?所以是否FV都是输入为正,PV输入都是为负,才可以得出正确结果?谢谢

NO.PZ2016031001000069问题如下BonG, scribein the exhibit below, is solfor settlement on 16 June 2014.AnnuCoupon 5%Coupon Payment Frequen SemiannualInterest Payment tes 10 April an10 OctoberMaturity te 10 October 2016y Count Convention 30/360AnnuYielto-Maturity 4%The full prithBonG will settle on 16 June 2014 is closest to:A.102.36.B.103.10.C.103.65. B is correct.The bons full priis 103.10. The priis terminein the following manner:of the beginning of the coupon perioon 10 April 2014, there are 2.5 years (5semiannuperio) to maturity. These five semiannuperio occur on 10 October2014, 10 April 2015, 10 October 2015, 10 April 2016 an10 October 2016. PV=PMT(1+r)1+PMT(1+r)2+PMT(1+r)3+PMT(1+r)4+PMT+FV(1+r)5PV=\frac{PMT}{{(1+r)}^1}+\frac{PMT}{{(1+r)}^2}+\frac{PMT}{{(1+r)}^3}+\frac{PMT}{{(1+r)}^4}+\frac{PMT+FV}{{(1+r)}^5}PV=(1+r)1PMT+(1+r)2PMT+(1+r)3PMT+(1+r)4PMT+(1+r)5PMT+FVPV=2.5(1+0.02)1+2.5(1+0.02)2+2.5(1+0.02)3+2.5(1+0.02)4+2.5+100(1+0.02)5PV=\frac{2.5}{{(1+0.02)}^1}+\frac{2.5}{{(1+0.02)}^2}+\frac{2.5}{{(1+0.02)}^3}+\frac{2.5}{{(1+0.02)}^4}+\frac{2.5\text{+}100}{{(1+0.02)}^5}PV=(1+0.02)12.5+(1+0.02)22.5+(1+0.02)32.5+(1+0.02)42.5+(1+0.02)52.5+100PV = 2.45 + 2.40 + 2.36 + 2.31 + 92.84 = 102.36The accrueinterest periois intifie66/180. The number of ys between10April2014 an16 June 2014 is 66 ys baseon the 30/360 y count convention. (This is 20ys remaining in April + 30 ys in M+ 16 ys in June = 66 ys total). The number of ys between coupon perio is assumeto 180 ys using the 30/360 y convention.PVFull=PV×(1 +r)66/180PV^{Full}=PV\times{(1\text{ }+r)}^{66/180}PVFull=PV×(1 +r)66/180PVFull= 102.36×(1.02)66/180= 103.10PV^{Full}=\text{ }102.36\times{(1.02)}^{66/180}=\text{ }103.10PVFull= 102.36×(1.02)66/180= 103.10考点flpri full price解析首先,我们将未来五笔现金流折现到2014.4.10,得到现值之和为102.36。N=5,PMT=2.5,I/Y=2,FV=100,求得PV=102.36然后再将这个数值复利到2014.6.16,得到full price为103.10,故B正确。我们之所以没有直接将未来五笔现金流折到2014.6.16,是因为五笔现金流的时间间隔不同,后面四笔现金流时间间隔是半年,而从6.16到10.10之间并不是半年。因此现金流就不是一个年金的形式,我们就没有办法用计算器直接求PV了。 最后为什么不是102。36 x (1+4%)的66/360次方?

NO.PZ2016031001000069 问题如下 BonG, scribein the exhibit below, is solfor settlement on 16 June 2014.AnnuCoupon 5%Coupon Payment Frequen SemiannualInterest Payment tes 10 April an10 OctoberMaturity te 10 October 2016y Count Convention 30/360AnnuYielto-Maturity 4%The full prithBonG will settle on 16 June 2014 is closest to: A.102.36. B.103.10. C.103.65. B is correct.The bons full priis 103.10. The priis terminein the following manner:of the beginning of the coupon perioon 10 April 2014, there are 2.5 years (5semiannuperio) to maturity. These five semiannuperio occur on 10 October2014, 10 April 2015, 10 October 2015, 10 April 2016 an10 October 2016. PV=PMT(1+r)1+PMT(1+r)2+PMT(1+r)3+PMT(1+r)4+PMT+FV(1+r)5PV=\frac{PMT}{{(1+r)}^1}+\frac{PMT}{{(1+r)}^2}+\frac{PMT}{{(1+r)}^3}+\frac{PMT}{{(1+r)}^4}+\frac{PMT+FV}{{(1+r)}^5}PV=(1+r)1PMT+(1+r)2PMT+(1+r)3PMT+(1+r)4PMT+(1+r)5PMT+FVPV=2.5(1+0.02)1+2.5(1+0.02)2+2.5(1+0.02)3+2.5(1+0.02)4+2.5+100(1+0.02)5PV=\frac{2.5}{{(1+0.02)}^1}+\frac{2.5}{{(1+0.02)}^2}+\frac{2.5}{{(1+0.02)}^3}+\frac{2.5}{{(1+0.02)}^4}+\frac{2.5\text{+}100}{{(1+0.02)}^5}PV=(1+0.02)12.5+(1+0.02)22.5+(1+0.02)32.5+(1+0.02)42.5+(1+0.02)52.5+100PV = 2.45 + 2.40 + 2.36 + 2.31 + 92.84 = 102.36The accrueinterest periois intifie66/180. The number of ys between10April2014 an16 June 2014 is 66 ys baseon the 30/360 y count convention. (This is 20ys remaining in April + 30 ys in M+ 16 ys in June = 66 ys total). The number of ys between coupon perio is assumeto 180 ys using the 30/360 y convention.PVFull=PV×(1 +r)66/180PV^{Full}=PV\times{(1\text{ }+r)}^{66/180}PVFull=PV×(1 +r)66/180PVFull= 102.36×(1.02)66/180= 103.10PV^{Full}=\text{ }102.36\times{(1.02)}^{66/180}=\text{ }103.10PVFull= 102.36×(1.02)66/180= 103.10考点flpri full price解析首先,我们将未来五笔现金流折现到2014.4.10,得到现值之和为102.36。N=5,PMT=2.5,I/Y=2,FV=100,求得PV=102.36然后再将这个数值复利到2014.6.16,得到full price为103.10,故B正确。我们之所以没有直接将未来五笔现金流折到2014.6.16,是因为五笔现金流的时间间隔不同,后面四笔现金流时间间隔是半年,而从6.16到10.10之间并不是半年。因此现金流就不是一个年金的形式,我们就没有办法用计算器直接求PV了。 为什么不是full price=10/4/2014的PV+accrueinterest?

NO.PZ2016031001000069 问题如下 BonG, scribein the exhibit below, is solfor settlement on 16 June 2014.AnnuCoupon 5%Coupon Payment Frequen SemiannualInterest Payment tes 10 April an10 OctoberMaturity te 10 October 2016y Count Convention 30/360AnnuYielto-Maturity 4%The full prithBonG will settle on 16 June 2014 is closest to: A.102.36. B.103.10. C.103.65. B is correct.The bons full priis 103.10. The priis terminein the following manner:of the beginning of the coupon perioon 10 April 2014, there are 2.5 years (5semiannuperio) to maturity. These five semiannuperio occur on 10 October2014, 10 April 2015, 10 October 2015, 10 April 2016 an10 October 2016. PV=PMT(1+r)1+PMT(1+r)2+PMT(1+r)3+PMT(1+r)4+PMT+FV(1+r)5PV=\frac{PMT}{{(1+r)}^1}+\frac{PMT}{{(1+r)}^2}+\frac{PMT}{{(1+r)}^3}+\frac{PMT}{{(1+r)}^4}+\frac{PMT+FV}{{(1+r)}^5}PV=(1+r)1PMT+(1+r)2PMT+(1+r)3PMT+(1+r)4PMT+(1+r)5PMT+FVPV=2.5(1+0.02)1+2.5(1+0.02)2+2.5(1+0.02)3+2.5(1+0.02)4+2.5+100(1+0.02)5PV=\frac{2.5}{{(1+0.02)}^1}+\frac{2.5}{{(1+0.02)}^2}+\frac{2.5}{{(1+0.02)}^3}+\frac{2.5}{{(1+0.02)}^4}+\frac{2.5\text{+}100}{{(1+0.02)}^5}PV=(1+0.02)12.5+(1+0.02)22.5+(1+0.02)32.5+(1+0.02)42.5+(1+0.02)52.5+100PV = 2.45 + 2.40 + 2.36 + 2.31 + 92.84 = 102.36The accrueinterest periois intifie66/180. The number of ys between10April2014 an16 June 2014 is 66 ys baseon the 30/360 y count convention. (This is 20ys remaining in April + 30 ys in M+ 16 ys in June = 66 ys total). The number of ys between coupon perio is assumeto 180 ys using the 30/360 y convention.PVFull=PV×(1 +r)66/180PV^{Full}=PV\times{(1\text{ }+r)}^{66/180}PVFull=PV×(1 +r)66/180PVFull= 102.36×(1.02)66/180= 103.10PV^{Full}=\text{ }102.36\times{(1.02)}^{66/180}=\text{ }103.10PVFull= 102.36×(1.02)66/180= 103.10考点flpri full price解析首先,我们将未来五笔现金流折现到2014.4.10,得到现值之和为102.36。N=5,PMT=2.5,I/Y=2,FV=100,求得PV=102.36然后再将这个数值复利到2014.6.16,得到full price为103.10,故B正确。我们之所以没有直接将未来五笔现金流折到2014.6.16,是因为五笔现金流的时间间隔不同,后面四笔现金流时间间隔是半年,而从6.16到10.10之间并不是半年。因此现金流就不是一个年金的形式,我们就没有办法用计算器直接求PV了。 我好像跟什么题目搞混了,有道题是再投资的,什么时候才会再投资来着?