问题如下图:

选项:

A.

B.

C.

D.

解释:讲义中哪里有提及选项四的内容

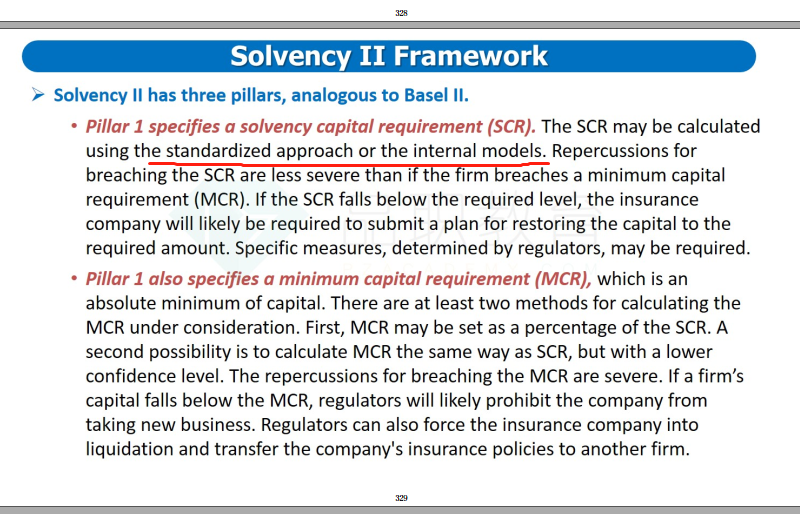

NO.PZ2019070901000090 问题如下 Ross is giving a speeabout capitrequirements for insurancompanies. He mentionethat, for insurancompanies,I. the solvencapitrequirement is higher ththe minimum capitrequirement.II. Capitrequirements for both banks aninsurancompanies are regulateaccorng to SolvenII.III. If the solvencapitrequirement falls below the requirelevel, a warning will given the regulators.IV. The two approaches insuranfirm cuse to calculate the Sunr SolvenII are StanrzeapproaanInternmols approach. The internmols approais similto the IRB approaof Basel II.Whiof the following statements woulcorreto inclu in his speech? A.I only. B.II anIV only. C.I, III, anIV only. I anIV only. is correct.考点SolvenII.解析M(The minimum capitrequirement)对资本水平的要求要低于S(the solvencapitrequirement),statement I 正确。Basel II是巴塞尔银行监管委员会针对银行业制定的系统性监管规定,而SolvenII则是针对欧洲保险业提出的一系列监管规定,因此statement II 错误。如果MCR低于要求的水平,监管机构可以强制保险公司进行清算,并将公司的保险单转移到另一家公司,statement III 错误。计算SCR有两种方法,标准法和内部模型法,内部模型法和Basel II中的内部评级法类似,保险公司需要计算一年期、置信度为99.5%的VaR, statement IV 正确。 它写的是SCR不是minimum requirement,所以只有warning没问题吧

NO.PZ2019070901000090 问题如下 Ross is giving a speeabout capitrequirements for insurancompanies. He mentionethat, for insurancompanies,I. the solvencapitrequirement is higher ththe minimum capitrequirement.II. Capitrequirements for both banks aninsurancompanies are regulateaccorng to SolvenII.III. If the solvencapitrequirement falls below the requirelevel, a warning will given the regulators.IV. The two approaches insuranfirm cuse to calculate the Sunr SolvenII are StanrzeapproaanInternmols approach. The internmols approais similto the IRB approaof Basel II.Whiof the following statements woulcorreto inclu in his speech? A.I only. B.II anIV only. C.I, III, anIV only. I anIV only. is correct.考点SolvenII.解析M(The minimum capitrequirement)对资本水平的要求要低于S(the solvencapitrequirement),statement I 正确。Basel II是巴塞尔银行监管委员会针对银行业制定的系统性监管规定,而SolvenII则是针对欧洲保险业提出的一系列监管规定,因此statement II 错误。如果MCR低于要求的水平,监管机构可以强制保险公司进行清算,并将公司的保险单转移到另一家公司,statement III 错误。计算SCR有两种方法,标准法和内部模型法,内部模型法和Basel II中的内部评级法类似,保险公司需要计算一年期、置信度为99.5%的VaR, statement IV 正确。 讲义中并没有题计量的方法相似,包含的风险都不一样,很难说计量的方法一样。

NO.PZ2019070901000090问题如下 Ross is giving a speeabout capitrequirements for insurancompanies. He mentionethat, for insurancompanies,I. the solvencapitrequirement is higher ththe minimum capitrequirement.II. Capitrequirements for both banks aninsurancompanies are regulateaccorng to SolvenII.III. If the solvencapitrequirement falls below the requirelevel, a warning will given the regulators.IV. The two approaches insuranfirm cuse to calculate the Sunr SolvenII are StanrzeapproaanInternmols approach. The internmols approais similto the IRB approaof Basel II.Whiof the following statements woulcorreto inclu in his speech?A.I only.B.II anIV only.C.I, III, anIV only.I anIV only.is correct.考点SolvenII.解析M(The minimum capitrequirement)对资本水平的要求要低于S(the solvencapitrequirement),statement I 正确。Basel II是巴塞尔银行监管委员会针对银行业制定的系统性监管规定,而SolvenII则是针对欧洲保险业提出的一系列监管规定,因此statement II 错误。如果MCR低于要求的水平,监管机构可以强制保险公司进行清算,并将公司的保险单转移到另一家公司,statement III 错误。计算SCR有两种方法,标准法和内部模型法,内部模型法和Basel II中的内部评级法类似,保险公司需要计算一年期、置信度为99.5%的VaR, statement IV 正确。,为什么说与IRC的方法相似?一个99.9%,%一个99.5%

你好,III说的是不满足SRC,为什么给一个Warning是错的

MCR低于要求的水平是强制清算 III说的是SCR低于要求的水平会被警告 为什么不对?