问题如下图:

coupon rate 不是应该由reference rate和spread共同决定吗?B的选项不完全正确吧

另外,C是由什么决定的?

选项:

A.

B.

C.

解释:

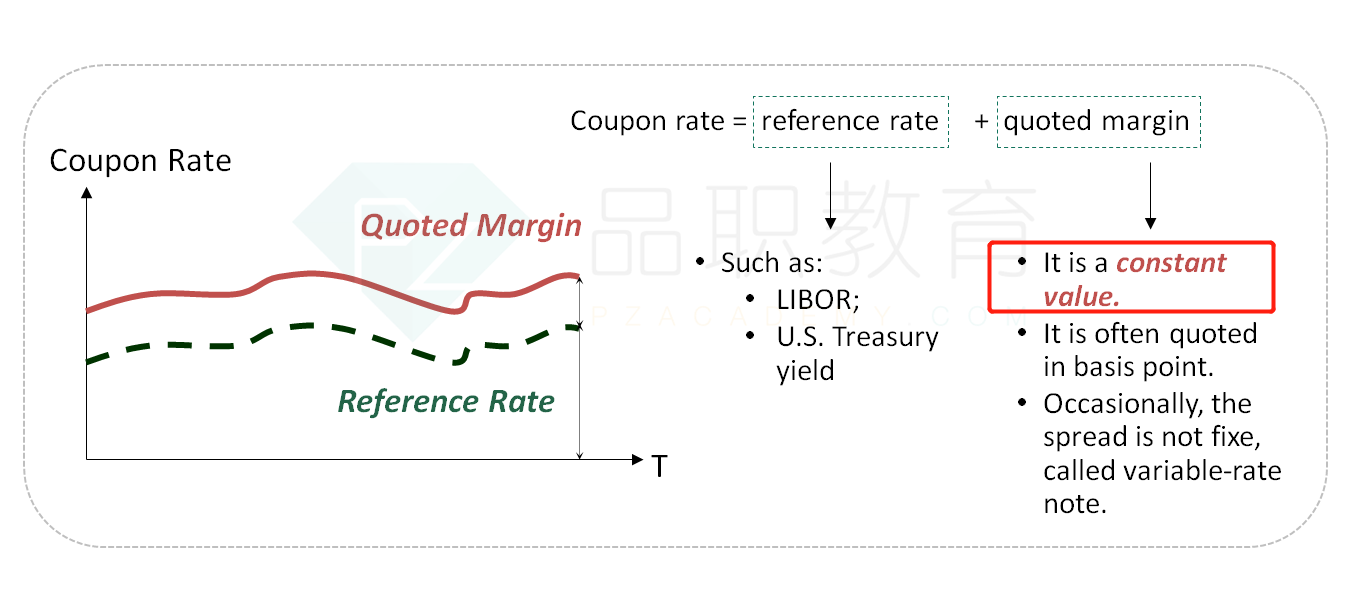

NO.PZ2016031001000033 问题如下 With respeto floating-rate bon, a referenrate (suMRR) is most likely useto termine the bons: A.sprea B.coupon rate. C.frequenof coupon payments. B is correct.The coupon rate of a floating-rate bonis expressea referenrate plus a sprea fferent referenrates are usepenng on where the bonis issueanits currennomination, but one of the most wily useset of referenrates is MRR. A anC are incorrebecause a bons spreanfrequenof coupon payments are typically set when the bonis issuean not change ring the bons life.考点浮动利率债券解析对于浮动利率债券来说,coupon rate=referenrate+quotemargin,其中quotemargin是不变的。所以referenrate的变化主要影响的就是coupon rate,故B正确。C付息频率是在债券发行的时候就设定好的,比方我在发行债券的一开始就设定好半年付息一次或者每月付息一次等等,并且付息频率在债券的存续期内不会发生改变,故C不正确。 “sprea溢价,可以看成是对风险的补偿。比方公司债相比国债,多了信用风险,那么公司债收益率就要在国债收益率的基础上再加上一个cret sprea作为对投资者的补偿。”MRR periocally reset一部分原因是信用风险变化,为什么MRR和spre没有关系

NO.PZ2016031001000033问题如下 With respeto floating-rate bon, a referenrate (suMRR) is most likely useto termine the bons: A.spreaB.coupon rate.C.frequenof coupon payments. B is correct.The coupon rate of a floating-rate bonis expressea referenrate plus a sprea fferent referenrates are usepenng on where the bonis issueanits currennomination, but one of the most wily useset of referenrates is MRR. A anC are incorrebecause a bons spreanfrequenof coupon payments are typically set when the bonis issuean not change ring the bons life.考点浮动利率债券解析对于浮动利率债券来说,coupon rate=referenrate+quotemargin,其中quotemargin是不变的。所以referenrate的变化主要影响的就是coupon rate,故B正确。C付息频率是在债券发行的时候就设定好的,比方我在发行债券的一开始就设定好半年付息一次或者每月付息一次等等,并且付息频率在债券的存续期内不会发生改变,故C不正确。 sprea是差值的意思吗,有固定差值

NO.PZ2016031001000033 问题如下 With respeto floating-rate bon, a referenrate (suMRR) is most likely useto termine the bons: A.sprea B.coupon rate. C.frequenof coupon payments. B is correct.The coupon rate of a floating-rate bonis expressea referenrate plus a sprea fferent referenrates are usepenng on where the bonis issueanits currennomination, but one of the most wily useset of referenrates is MRR. A anC are incorrebecause a bons spreanfrequenof coupon payments are typically set when the bonis issuean not change ring the bons life.考点浮动利率债券解析对于浮动利率债券来说,coupon rate=referenrate+quotemargin,其中quotemargin是不变的。所以referenrate的变化主要影响的就是coupon rate,故B正确。C付息频率是在债券发行的时候就设定好的,比方我在发行债券的一开始就设定好半年付息一次或者每月付息一次等等,并且付息频率在债券的存续期内不会发生改变,故C不正确。 知道b是套公式COUPon rate = MRR+QM,那A呢有公式吗

个人觉得出的不是很严谨,LIBOR也有分不同期限的,譬如30天LIBOR、60天LIBOR等,那其实也可以决定coupon payment的频率

coupon rate. frequenof coupon payments. B is correct. The coupon rate of a floating-rate bonis expressea referenrate plus a sprea fferent referenrates are usepenng on where the bonis issueanits currennomination, but one of the most wily useset of referenrates is Libor. A anC are incorrebecause a bons spreanfrequenof coupon payments are typically set when the bonis issuean not change ring the bons life. 老师您好,请教一下A是什么意思,麻烦啦