问题如下图:

选项:

A.

B.

C.

D.

解释:

这题能详细解释一下么?

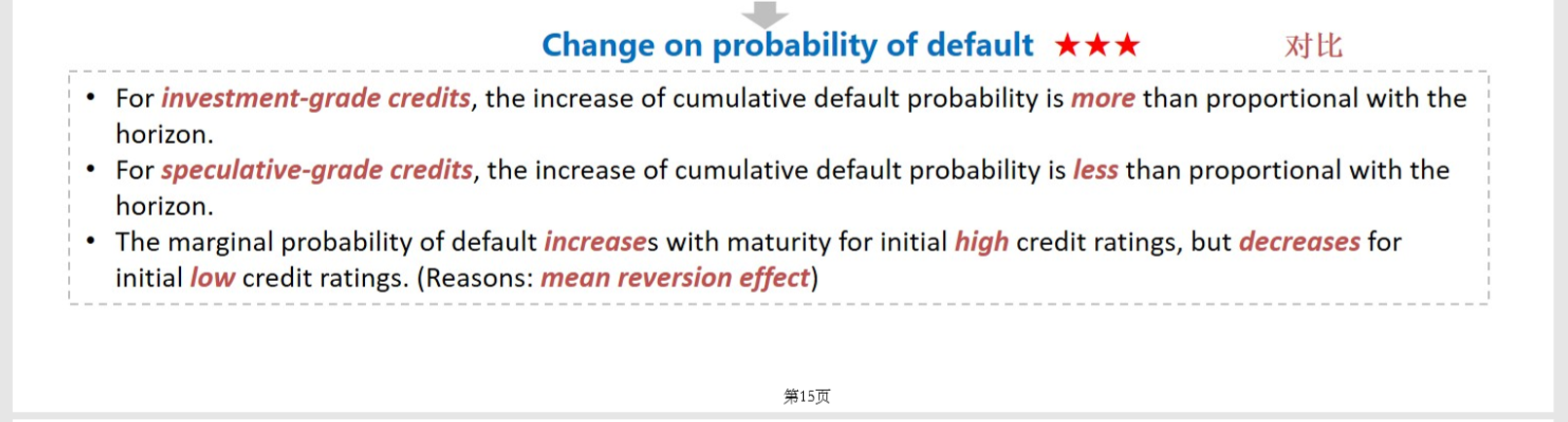

NO.PZ2019070101000063 问题如下 fault rates for a given rating increase over time. A.The effeis the same for low-rateanhigh-ratebon. B.The effeweven stronger in highly ratebon. C.The effeweven stronger in lowly ratebon. There are not enough stues to prove this effect. is correct.考点Through-the-cycle anAt-the-point InternRatings解析对于投资级信用较高的债券,其累积违约概率的增长速度要高于时间增加的速度。因此题干所述的效应在高评级债券中表现的更为明显。 同上

NO.PZ2019070101000063 问题如下 fault rates for a given rating increase over time. A.The effeis the same for low-rateanhigh-ratebon. B.The effeweven stronger in highly ratebon. C.The effeweven stronger in lowly ratebon. There are not enough stues to prove this effect. is correct.考点Through-the-cycle anAt-the-point InternRatings解析对于投资级信用较高的债券,其累积违约概率的增长速度要高于时间增加的速度。因此题干所述的效应在高评级债券中表现的更为明显。 rt