开发者:上海品职教育科技有限公司 隐私政策详情

应用版本:4.2.11(IOS)|3.2.5(安卓)APP下载

随时随地学习课程,支持音视频下载!

ciaoyy · 2019年07月16日

问题如下图:

选项:

A.

B.

C.

D.

解释:

品职答疑小助手雍 · 2019年07月16日

同学你好,是求导的结果,这个t=T/3其实可以当成结论来记一下了~

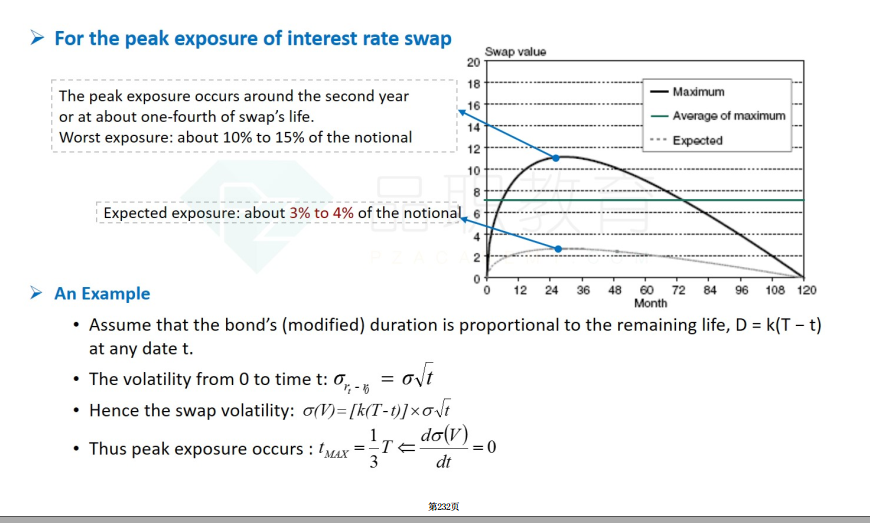

Assume thyou have entereinto a fixefor-floating interest rate swthstarts toy anen in six years. Assume ththe ration of your position is proportionto the time to maturity. Also assume thall changes in the yielcurve are parallel shifts, anththe volatility of interest rates is proportionto the square root of time. When woulthe maximum potentiexposure reache In two months In two years In six years In four years anfive months ANSWER: B Exposure is a function of ration, whicreases with time, aninterest rate volatility, whiincreases with the square root of time. fine T the originmaturity ank a constant. This gives σ(Vt)=k(T−t)t\sigma{(V_t)}=k{(T-t)}\sqrt tσ(Vt)=k(T−t)t . Taking the rivative with respeto t gives a maximum t=T3t=\frT3t=3T. This gives t=63=2t=\frac63=2t=36=2years. 这里不是说ration会随着时间增长而增加吗 那个1/3的结论不是说到期ration的效果减少吗,那是不是没有摊销效应