问题如下图:

选项:

A.

B.

C.

D.

解释:

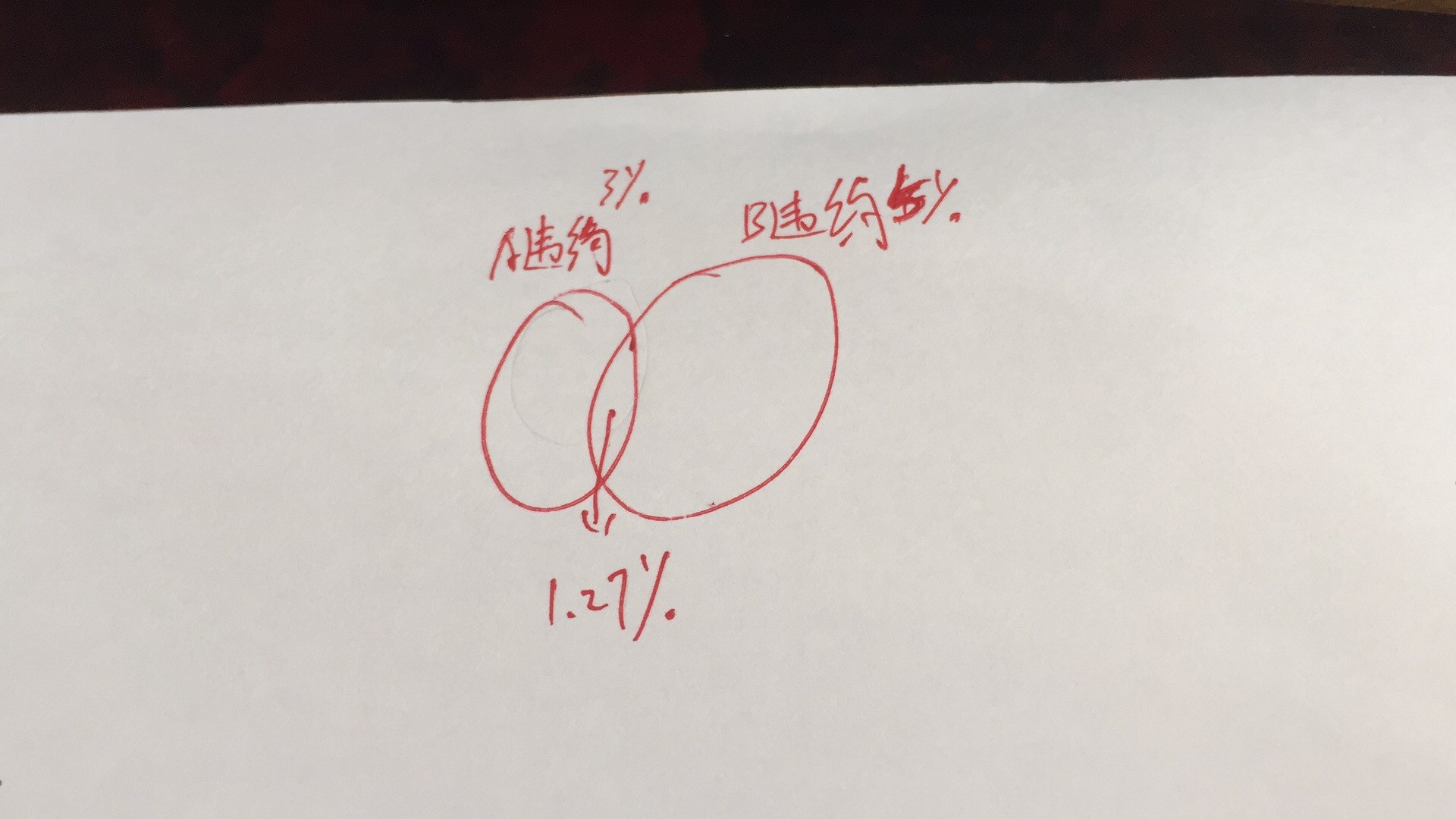

两个bond的default有相关性,为什么40k的损失对应的概率可以是3%-1.27%呢?

US400,000 US360,000 US370,000 ANSWER: Here, the joint fault probability matters. If the two bon fault, the loss is $1,000,000×(1−60%)+$600,000×(1−40%)=$400,000+$360,000=$760,000\$1,000,000\times\left(1-60\%\right)+\$600,000\times\left(1-40\%\right)=\$400,000+\$360,000=\$760,000$1,000,000×(1−60%)+$600,000×(1−40%)=$400,000+$360,000=$760,000. This will happen with probability 1.27%. The next biggest loss is $400,000, whihprobability of 3.00%-1.27%=1.73% Its cumulative probability must 100.00−1.27=98.73%100.00-1.27=98.73\%100.00−1.27=98.73%. This is slightly above 98%, so $400,000 is the quantile the 98% level of confinor higher. Subtracting the megives $370,000. 请问第二大损失400000发生的概率是如何推导的?

还有最后这个expecteloss (the me) = 40000 是怎么算出来的?

为什么算expecteloss的时候 只考虑回收率而不考虑 fault probability呢?

The next biggest loss is $400,000, whihprobability of 3.00%-1.27%=1.73% 请问为什么概率不是3%*(1-5%)=2.85%

选%的时候,不是应该选择大一点的么?为什么不能选择760的98.7%呢?为什么还需要再算一个400的loss呢?谢谢