maggie_品职助教 · 2019年06月10日

这个well-construced portfoilo认为只要符合投资者风险收益预期的组合即为“well”,这里的risk efficient指的是只有承担风险才获得补偿,如果两个基金经理具有相似的skils,active share肯定越大越好。换句话说 投资者花同样的钱,基金经理是否能承担相同的主动风险active risk(这fee花的值不值)。

active risk越大,说明组合里面的股票与benchmark越不像。这里看active risk不能只看绝对数值要结合组合里面选取的股票数量一起看,M研究140只股票能获得3.2%的主动风险,而B研究了340只股票才获得5.5%的主动风险(说明B组合340只股票和benchmark更像,B更像被动投资),相比之下M基金的主动性更高,也更加的risk efficient. 这道题答案也是这么解释的:It delivers the lowest active risk (3.2%) using far fewer securities (140), indicating an efficient approach. 它虽然在三个基金中获得最低ACTIVE RISK,但是相比之下它分析了更少的股票,这句话也就解释了什么是 risk efficient approach.

这个点确实比较绕,但好在这道题和原版书上的例题思路是一致的,如果考试也这么做肯定不会错。

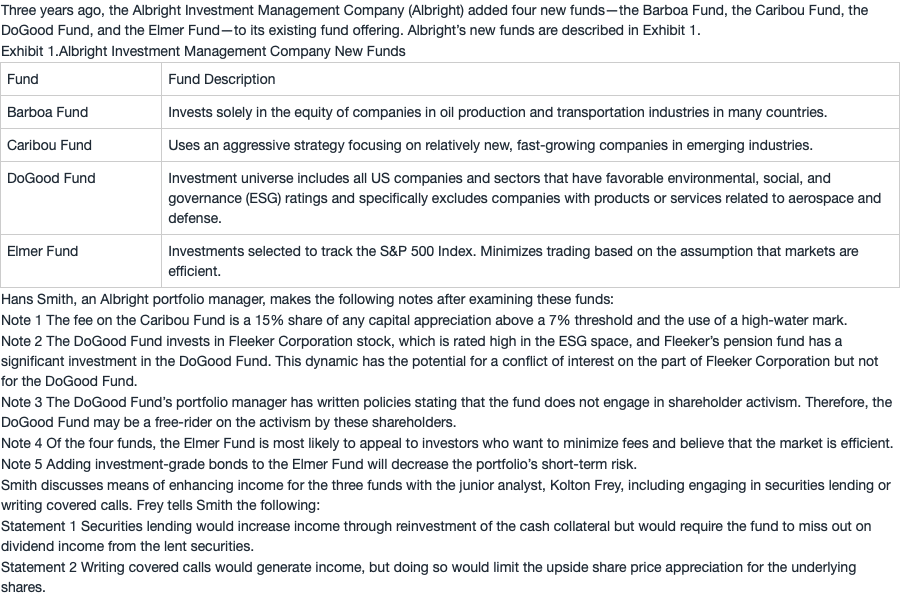

NO.PZ201809170400000101 问题如下 The Barboa Funcbest scribea funsegmenteby: size/style. geography. economic activity. C is correct. The Barboa Funinvests solely in the equity of companies in the oil proction antransportation instries in many countries. The funs scription is consistent with the proction-orienteapproach, whigroups companies thmanufacture similprocts or use similinputs in their manufacturing processes. A is incorrebecause the funscription es not mention the firms’ size or style (i.e., value, growth, or blen. Size is typically measuremarket capitalization anoften categorizelarge cap, micap, or small cap. Style is typically classifievalue, growth, or a blenof value angrowth. In aition, style is often terminethrough a \"scoring\" system that incorporates multiple metrior ratios, suprice-to-book ratios, price-to-earnings ratios, earnings growth, vinyiel anbook value growth. These metriare then typically \"score" invially for each company, assignecertain weights, anthen aggregate B is incorrebecause the funis investeacross many countries, whiincates ththe funis not segmentegeography. Segmentation geography is typically baseupon the stage of countries’ macroeconomic velopment and wealth. Common geographic categories are velopemarkets, emerging markets, anfrontier markets. 例如说题目中的transportation,感觉无论是站在supplier或者是consumer的立场,这个分类都是成立的。疑惑,有没有一个比较清晰的思路

问一道题:NO.PZ201809170400000101