发亮_品职助教 · 2019年05月28日

第6题对应的题干在这里:

Hudgens needs Soto’s help to select a benchmark index that is appropriate for Kiest’s young workforce and avoids the “bums” problem.

也就是为Kiest的Pension plan选择一个合适的Benchmark index,Benchmark的属性要适合组合Pension plan。而Kiest pension plan的特点是Young workforce,所以这个Plan有比较长的投资期(Time-horizon),因为Duration和期限成正比,所以这个Plan有比较大的Duration。

如果要作为Kiest pension plan的Benchmark,那这个Benchmark index必须要有较大的Duration。

这个Benchmark还要有第二个要求,就是避免Bums problems。

一些Bond Index,如果以债券市值为权重构建Index,会产生Bums problem,因为发债越多的公司在Index中的权重越高,那这样其实是不太好的,因为发债越多的公司往往杠杆比较高、质量不太好。所以有时就要避免Bums problem,避免给这些高杠杆的企业过多的权重投资。

而Bums probelm是由于使用市值为权重带来的,解决他的方法就是找一个不是以债券市值为权重的Index即可,例如以GDP为权重。

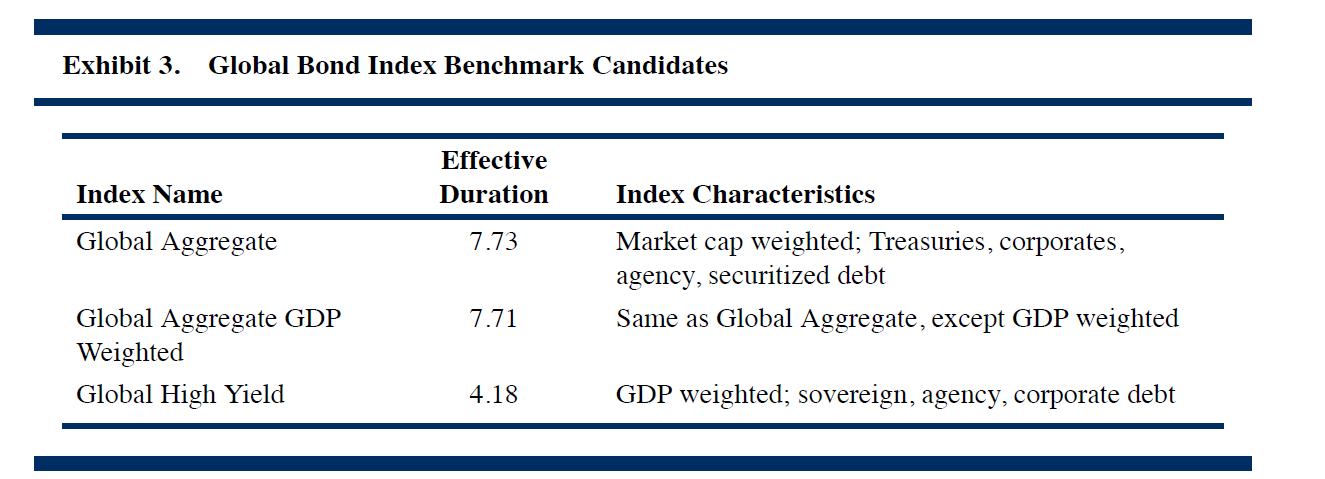

这样,我们就在下面这个表里找一个不是以市值为权重的Index,同时Index的Duration要比较大。

第一个Global Aggregate是以市值为权重(Market cap weighted),所以排除。

第三个Global high yield,虽然不是以市值为权重的,但是他的Effective duration太小,排除。

这样就是第二个Global aggregate GDP weighted符合要求,不是以市值为权重(以GDP为权重),且Duration较大。

第八题问投资Mutual fund的三个Reason哪个是正确的。

Reason 1: Total return swaps have much higher transaction costs and initial cash outlay than bond mutual funds.

这点错误,因为Swap只是交换期间现金流,期初不需要支出,所以他说的Higher initial cash outlay不对。

Reason 3: Bond mutual funds can be traded throughout the day at the net asset value of the underlying bonds

他说Mutual fund可以以Net asset value完成日内交易(traded throughout the day),这点错误,因为Mutual fund不能完成日内交易,一般至少会有一个1天的Time-lag,也就是说今天下单卖出,明天才能完成指令。

Reason 2:Unlike bond mutual funds, bond ETFs can trade at discounts to their underlying indexes, and those discounts can persist.

这点是正确的。他是说ETF二级市场的交易价格低于他标的指数的价格(Net asset value)。

ETF可以在二级市场交易,所以市场交易会影响到交易价格,交易价格会偏离ETF标的指数的内在价格Net asset value;虽然说ETF存在1级与2级市场套利,使得ETF价格和NAV趋同,但是债券市场流动性较差,一些套利比较难完成,所以这种差价可能会持续(discounts can persist)。所以Reason 2说的交易价格持续低于标的指数的价格正确。