问题如下图:年化VL没看懂是用的什么公式

选项:

A.

B.

C.

D.

解释:

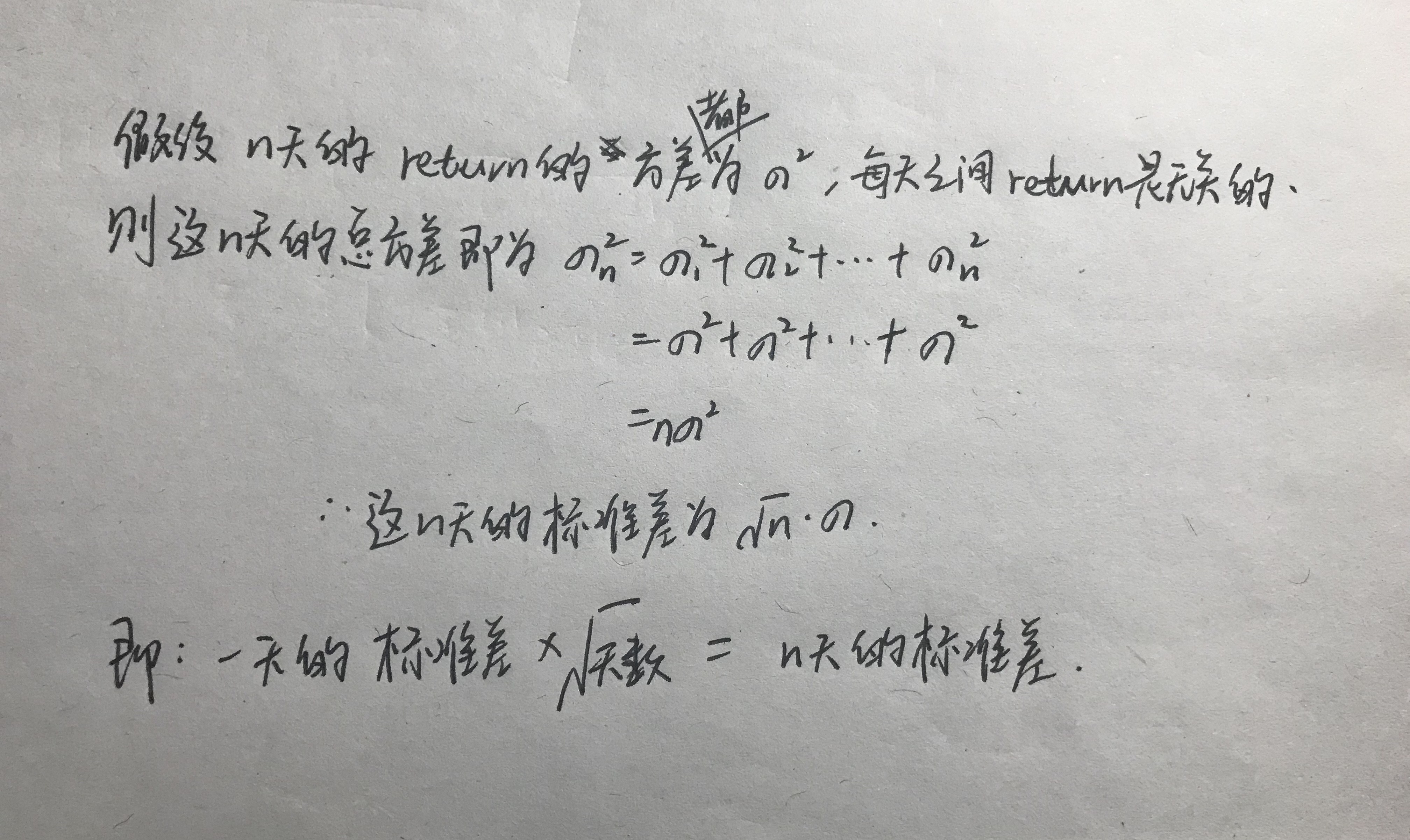

NO.PZ2019040801000079 问题如下 Anlyst Pengyu is using a GARCH(1,1) mol to estimate ily varianon ily returns(rt) :ht:=α0 + α1r2t-1 + βht-1 while α0 = 0.000003α1 = 0.03β = 0.94Whis the long-run annualizevolatility estimate (assuming thvolatility increases the square root of time an252 trang ys in a ye? A.0.015%. B.1.00%. C.9.27%. 15.87%. is correct.考点GARCH(1,1)模型解析首先求出γ,GARCH(1,1)中α1+β+γ=1,所以γ=1-0.03-0.94=0.03.然后long-run ily variance= α0 / γ= 0.000003/0.03= 0.0001那么波动率就是标准差,用方差开方即可0.01.最后年化0.01*(252^0.5)=15.87% 年化具体的计算过程可以详细讲解一下不,谢谢

NO.PZ2019040801000079问题如下Anlyst Pengyu is using a GARCH(1,1) mol to estimate ily varianon ily returns(rt) :ht:=α0 + α1r2t-1 + βht-1 while α0 = 0.000003α1 = 0.03β = 0.94Whis the long-run annualizevolatility estimate (assuming thvolatility increases the square root of time an252 trang ys in a ye?A.0.015%.B.1.00%.C.9.27%.15.87%. is correct.考点GARCH(1,1)模型解析首先求出γ,GARCH(1,1)中α1+β+γ=1,所以γ=1-0.03-0.94=0.03.然后long-run ily variance= α0 / γ= 0.000003/0.03= 0.0001那么波动率就是标准差,用方差开方即可0.01.最后年化0.01*(252^0.5)=15.87% 可以详细一点嘛。关于年化的计算

NO.PZ2019040801000079 问题如下 Anlyst Pengyu is using a GARCH(1,1) mol to estimate ily varianon ily returns(rt) :ht:=α0 + α1r2t-1 + βht-1 while α0 = 0.000003α1 = 0.03β = 0.94Whis the long-run annualizevolatility estimate (assuming thvolatility increases the square root of time an252 trang ys in a ye? A.0.015%. B.1.00%. C.9.27%. 15.87%. is correct.考点GARCH(1,1)模型解析首先求出γ,GARCH(1,1)中α1+β+γ=1,所以γ=1-0.03-0.94=0.03.然后long-run ily variance= α0 / γ= 0.000003/0.03= 0.0001那么波动率就是标准差,用方差开方即可0.01.最后年化0.01*(252^0.5)=15.87%lLong−run ily stanrviation =variance=0.00004=0.6325%Annualizestanrviation=ily stanrviation×time=0.6325%×252=10.04%{l}Long-run\text{ }ily\text{ }stanrtext{ }viation\text{ }=\sqrt{variance}=\sqrt{0.00004}=0.6325\%\\Annualizetext{ }stanrtext{ }viation=ily\text{ }stanrtext{ }viation\times\sqrt{time}\\=0.6325\%\times\sqrt{252}=10.04\%lLong−run ily stanrviation =variance=0.00004=0.6325%Annualizestanrviation=ily stanrviation×time=0.6325%×252=10.04% 1.年化日标准差为什么是除以252的0.5次方,为什么不是直接除以252?2.一年是按250还是按252天算?3.Long−run ily stanrviation = 。。。。。。varian=0.00004此处的0.00004是怎么来的?谢谢老师

NO.PZ2019040801000079问题如下 Anlyst Pengyu is using a GARCH(1,1) mol to estimate ily varianon ily returns(rt) :ht:=α0 + α1r2t-1 + βht-1 while α0 = 0.000003α1 = 0.03β = 0.94Whis the long-run annualizevolatility estimate (assuming thvolatility increases the square root of time an252 trang ys in a ye?A.0.015%.B.1.00%.C.9.27%.15.87%.is correct.考点GARCH(1,1)模型解析首先求出γ,GARCH(1,1)中α1+β+γ=1,所以γ=1-0.03-0.94=0.03.然后long-run ily variance= α0 / γ= 0.000003/0.03= 0.0001那么波动率就是标准差,用方差开方即可0.01.最后年化0.01*(252^0.5)=15.87%lLong−run ily stanrviation =variance=0.00004=0.6325%Annualizestanrviation=ily stanrviation×time=0.6325%×252=10.04%{l}Long-run\text{ }ily\text{ }stanrtext{ }viation\text{ }=\sqrt{variance}=\sqrt{0.00004}=0.6325\%\\Annualizetext{ }stanrtext{ }viation=ily\text{ }stanrtext{ }viation\times\sqrt{time}\\=0.6325\%\times\sqrt{252}=10.04\%lLong−run ily stanrviation =variance=0.00004=0.6325%Annualizestanrviation=ily stanrviation×time=0.6325%×252=10.04%老师这个知识点有点忘了,可以具体一下这个题吗,γ是什么,variance是怎么算出来的

NO.PZ2019040801000079 这里题目里的 long-run annualizevolatility estimate 就是指模型里的VL吗, 不是指的模型里的sigma