factor-based approach在Passive策略和active策略里面都有,我理解的不是很到位,帮我看看下面理解的对吗?

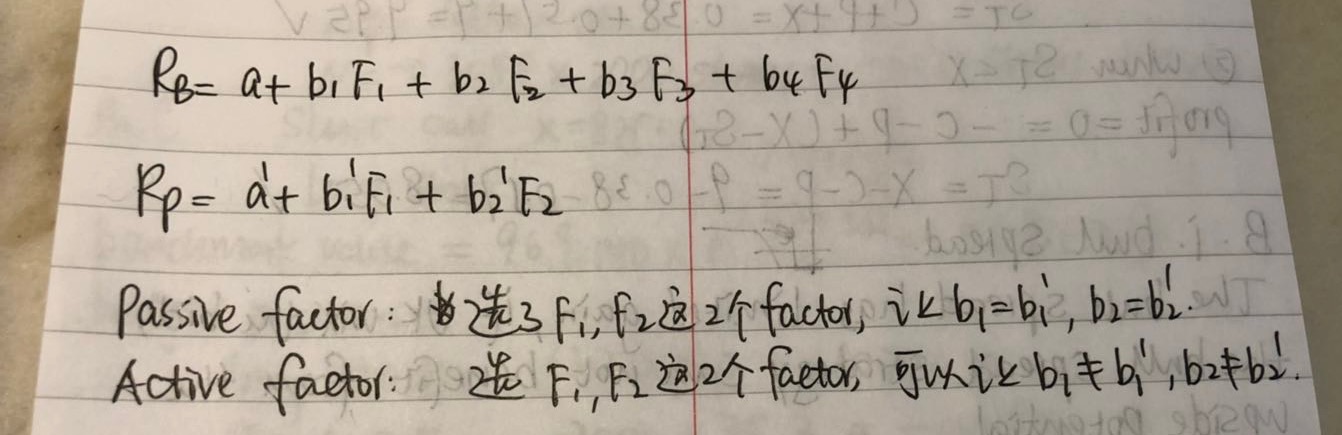

1. passive factor-based approach和active factor-based approach的相同点是:两个策略都是在market index之上选择想要Overweight或underweight的risk factor做concentrated 投资。比如我下面的图,market index里面有4个risk factor, 两个方法选择了其中的2个risk factor(F1和F2)做concentrated投资

2.两者的不同点是:比如我下面的图,active factor based是必须b1不等于b1',b2不等于b2',才算做了主动投资。

3. 在passive factor-based方法的题目(经典题Passive Factor-based strategies第3题)答案有句话是这么说的”passive factor-strategies tend to be transparent in terms of factor selection, weighting, and rebalancing", 我不理解passive factor-based也是基于Market index来有基金经理自主选择risk factor, 怎么能做到transparent? 而且李老师讲这道题的时候解释说,因为是被动投资,所以benchmark需要做到transparent,但是market index确实是公开的,基金经理选factor这个动作怎么能是透明化的?