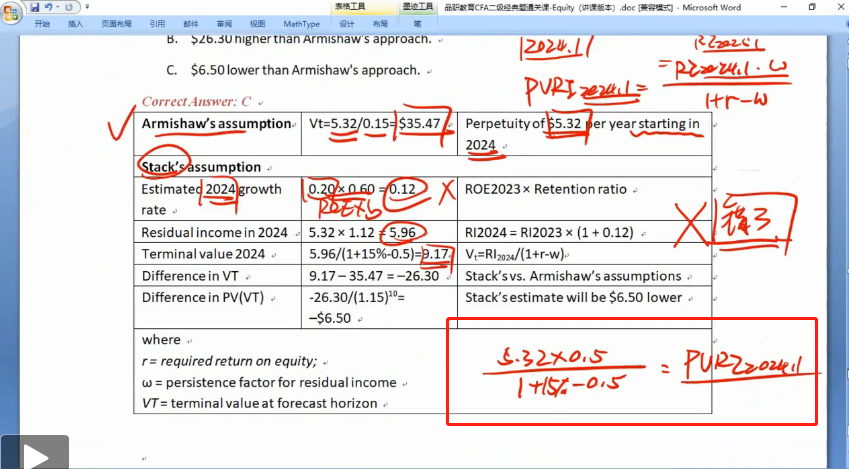

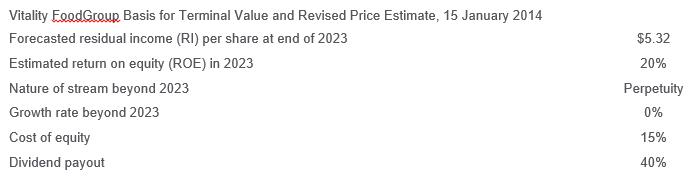

Armishaw next presents Exhibit 2, which contains the basis for his estimates for the share price (as of 15 January 2014) if he assumes a terminal value in 2023 arising from treating 2023’s residual income as a perpetuity.

Exhibit 2

Stack questions Armishaw’s assumption in his 2014 valuation (Exhibit 2) that a perpetuity would best describe the terminal value of the stream and suggests that residual income should fade over time. Stack further suggests that a persistence factor of 0.50 might be appropriate.

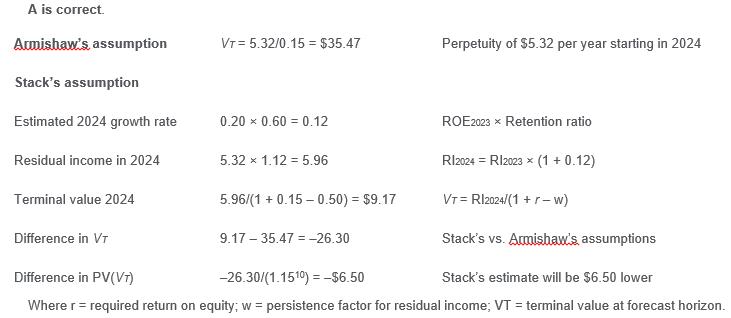

Using the information in Exhibit 2, comparing Armishaw’s approach to terminal value to Stack’s approach, Stack’s assumption leads to a 2024 value that is approximately:

A. $6.50 lower than Armishaw’s approach.

B. $6.74 lower than Armishaw’s approach.

C. $26.30 higher than Armishaw’s approach.

解答:

请问, 为什么,持续因子为1的时候, 要用2023年 的RI来计算;而持续 因子为0.5的时候, 就要用2024年的RI来计算?