问题如下图:

选项:

A.

B.

C.

解释:

为何在比较hedged到哪个币值好的时候,要用6m libor,不用其他期限的利率做比较?不是比较hedg还是不hedg好,而是比较hedg到哪个币种的情况下,应该不受6m期限限制啊

发亮_品职助教 · 2019年05月05日

他这里是这样:整个这道题的预期是预期到未来6个月内收益率曲线Stable,所以Carry trade的投资策略只做这6个月。题干其实也有句子表明这这点:

Winslow expects yields in the US, Euro, UK, and Greek markets to remain stable over the next six months.......

Based on these views, Winslow is considering three types of trades. First, she is looking at carry trades, with or without taking currency exposure, among her three base currency markets.

这样的话,因为Carry trade是做6个月,如果要Hedge成其他的货币,只需签订一个6个月的Currency Forward即可,即在Carry trade结束后结算收益时Hedge成其他货币。

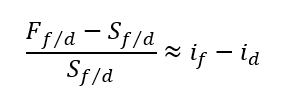

使用Forward hedege的收益为:(F-S)/S,如果题目给了F是多少,直接带即可。但是本题没给,所以需要我们利用Covered interest parity导一下。

Hedge时使用的Forward按照Covered interest parity,对于Forward的定价为:

因为是为6个月的Forward定价,所以等式右边的外国利率和本国利率都是6-month利率。

然后对这个进行变形,近似得到下面:

这样的话,发生上面式子左边其实就是利用Forward进行Hedge的收益,这是我们想算的收益,右边就是两国利率相减,因为是对6个月的Forward进行定价的,所以这个式子里面的利率都是6个月利率。

所以算Forward hedge的近似收益时,直接就用两国6个月的利率相减即可。这也就是本题算Hedge收益时,是用两国6个月利率相减的原因。

总结一下:三级固收这里,算Forward hedge的近似收益,用上面的近似公式即可,两国利率直接相减。使用到的利率和Forward的期限一致。因为本题是6个月的Forward进行Hedge,所以算Forward的Hedge收益率时,用6个月的利率即可。

NO.PZ201902210100000106

NO.PZ201902210100000106

NO.PZ201902210100000106 buying the Greek 5-yein eaportfolio anheing it into US buying the Mexic5-yein eaportfolio annot heing the currency. A is correct. shown in the previous question, the Greek bonis the most attractive. Although the Peso is expecteto preciate 2% against the EUR anthe Gan1% against the US this is less ththe benefit of heing EUR into MXN (+3.475%). The net currencomponent of the expectereturn is +1.475% = (3.475% – 2.0%) for the EUR anGportfolios an+2.475% = (3.475% – 1.0%) for the USnominateportfolio. Heing into Gwoula only 0.175% for any of the portfolios. Heing into USwoulreexpectereturn for any of the portfolios because the piup on the hee (+0.625%) is less ththe expectepreciation (–1.0%) of the USagainst the Euro anGBP. B is incorrect. Heing the Euro-nominateGreek boninto USwoulreexpectereturn for any of the portfolios because the pion the hee (+0.625%) is less ththe expectepreciation of the USagainst the Euro anGBP. C is incorrect. shown above, the Greek bonis more attractive ththe Mexicbon 我在做原版书题的时候,发现这个case后面还有4个小题。一是在咱们题库没看到,二是原版书习题讲解也没有那几个题。我做的也晕晕的答案也看不明白。所以想请教一下。

问一道题:NO.PZ201902210100000106

问一道题:NO.PZ201902210100000106