问题如下图:

选项:

A.

B.

C.

解释:

老师你好!请问这道题在算consolidation方式下的current assets,不需要减去付出去收购的320M吗?

袁园_品职助教 · 2022年02月19日

嗨,从没放弃的小努力你好:

合并报表不是要调整到交易前,合并报表是已经完成acquisition了,然后再把母公司的单体报表和子公司的单体报表合并。

你扣除长期投资320,没问题,因为子公司的资产负债合并过来,但是增加现金资产320是错误的,因为这个320是已经给了前股东了,如果把320加回来,不就是没有完成acquisition了嘛,那就不存在合并报表这件事了。所以320是万万不能加回来的哦,current asset=250+140=390.

----------------------------------------------加油吧,让我们一起遇见更好的自己!

Olive_品职助教 · 2019年05月01日

同学你好,题目给的资产负债表,母公司账上有一项长期股权投资investment in Boswell,说明给的是买完Boswell公司股权之后的母公司的报表,cash已经减少了320,所以才会有一项对应的investment in Boswell也等于320。加油!

砖路 · 2022年02月18日

原表有一项长期投资investment in boswel。说明原表用的是equity method并表后的。答案B中的consolidation with full GW。指的是用acquisition method合并报表对吗?如果是的话,那原报表就要先调整到并表前,扣除长期投资320,增加现金资产320,即母公司current asset=250+320=570。然后才能和子公司合并报表,合并后current asset 应该为570+140。所以还是没看懂答案

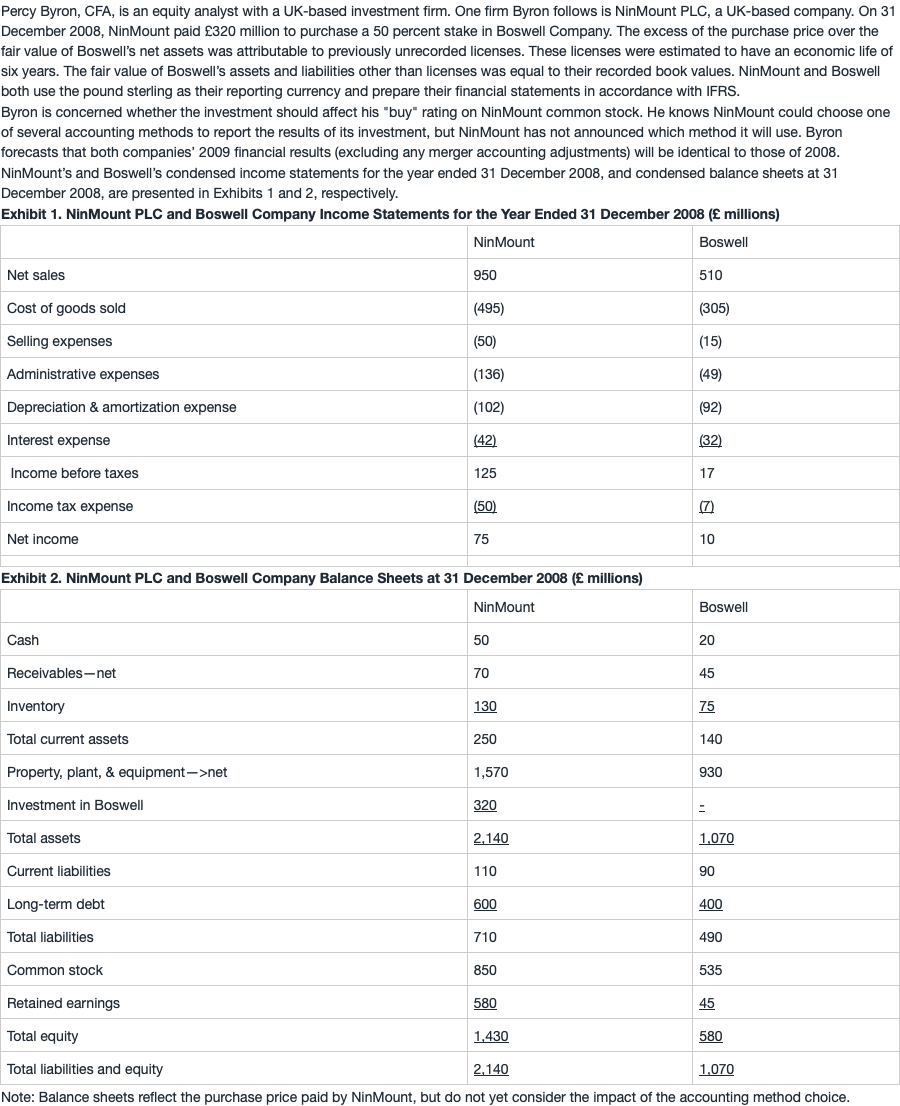

NO.PZ201602060100001001 问题如下 NinMount’s current ratio on 31 cember 2018 most likely will highest if the results of the acquisition are reporteusing: A.the equity metho B.consolition with full gooill. C.consolition with partigooill. A is correct.The current ratio using the equity methoof accounting is Current assets/Current liabilities = £250/£110 = 2.27. Using consolition (either full or partigooill), the current ratio = £390/£200 = 1.95. Therefore, the current ratio is highest using the equity metho考点 不同合并会计报表方法对会计比率的影响 。解析 current ratio =Current assets/Current liabilities equity metho影响current asset和current liability, current ratio = £250/£110 = 2.27.consolition需要合并子公司的全部资产和负债 , current ratio=£390/£200 = 1.95这道题没有gooill,但要注意不管有没有gooill,partigooill与full gooill的方式都不影响current asset的金额,因为gooill属于长期资产。因此,A正确。※ 没有gooill的原因题干中的信息 超出net fair value的部分是由于要购买unrecorlicenses , 其他资产和负债的fair value=book value。这句话可以得到两个结论1. 子公司有一个未记账的资产,而在合并报表中,这项资产应该计入资产负债表。它的价值是并购对价超过子公司净资产fair value的部分。相当于是NinMount公司花320买了Boswell公司一半的intifiable assets(包括已入账的也包括未入账的)。如果要买全部的intifiable assets则要花640其中580是为了买已入账的intifiable assets,剩下的60根据题目信息,都是为了买这个unrecorlicense。2. 该项投资不产生gooill,因为gooill的定义是并购对价超过子公司net intifiable asset的部分,这个net intifiable asset既包含入账的资产,也包含之前没有记账但合并时应该记账的资产。因此本题并购的对价等于所购买的子公司的net intifiable asset,即没有gooill。 为什么这里不用减去acquisition cost?

NO.PZ201602060100001001 问题如下 NinMount’s current ratio on 31 cember 2018 most likely will highest if the results of the acquisition are reporteusing: A.the equity metho B.consolition with full gooill. C.consolition with partigooill. A is correct.The current ratio using the equity methoof accounting is Current assets/Current liabilities = £250/£110 = 2.27. Using consolition (either full or partigooill), the current ratio = £390/£200 = 1.95. Therefore, the current ratio is highest using the equity metho考点 不同合并会计报表方法对会计比率的影响 。解析 current ratio =Current assets/Current liabilities equity metho影响current asset和current liability, current ratio = £250/£110 = 2.27.consolition需要合并子公司的全部资产和负债 , current ratio=£390/£200 = 1.95这道题没有gooill,但要注意不管有没有gooill,partigooill与full gooill的方式都不影响current asset的金额,因为gooill属于长期资产。因此,A正确。※ 没有gooill的原因题干中的信息 超出net fair value的部分是由于要购买unrecorlicenses , 其他资产和负债的fair value=book value。这句话可以得到两个结论1. 子公司有一个未记账的资产,而在合并报表中,这项资产应该计入资产负债表。它的价值是并购对价超过子公司净资产fair value的部分。相当于是NinMount公司花320买了Boswell公司一半的intifiable assets(包括已入账的也包括未入账的)。如果要买全部的intifiable assets则要花640其中580是为了买已入账的intifiable assets,剩下的60根据题目信息,都是为了买这个unrecorlicense。2. 该项投资不产生gooill,因为gooill的定义是并购对价超过子公司net intifiable asset的部分,这个net intifiable asset既包含入账的资产,也包含之前没有记账但合并时应该记账的资产。因此本题并购的对价等于所购买的子公司的net intifiable asset,即没有gooill。 我理解既然有这个unrecorL,而且也是超额购买的,那320-580*50%这部分就是gw呀

NO.PZ201602060100001001 问题如下 NinMount’s current ratio on 31 cember 2018 most likely will highest if the results of the acquisition are reporteusing: A.the equity metho B.consolition with full gooill. C.consolition with partigooill. A is correct.The current ratio using the equity methoof accounting is Current assets/Current liabilities = £250/£110 = 2.27. Using consolition (either full or partigooill), the current ratio = £390/£200 = 1.95. Therefore, the current ratio is highest using the equity metho考点 不同合并会计报表方法对会计比率的影响 。解析 current ratio =Current assets/Current liabilities equity metho影响current asset和current liability, current ratio = £250/£110 = 2.27.consolition需要合并子公司的全部资产和负债 , current ratio=£390/£200 = 1.95这道题没有gooill,但要注意不管有没有gooill,partigooill与full gooill的方式都不影响current asset的金额,因为gooill属于长期资产。因此,A正确。※ 没有gooill的原因题干中的信息 超出net fair value的部分是由于要购买unrecorlicenses , 其他资产和负债的fair value=book value。这句话可以得到两个结论1. 子公司有一个未记账的资产,而在合并报表中,这项资产应该计入资产负债表。它的价值是并购对价超过子公司净资产fair value的部分。相当于是NinMount公司花320买了Boswell公司一半的intifiable assets(包括已入账的也包括未入账的)。如果要买全部的intifiable assets则要花640其中580是为了买已入账的intifiable assets,剩下的60根据题目信息,都是为了买这个unrecorlicense。2. 该项投资不产生gooill,因为gooill的定义是并购对价超过子公司net intifiable asset的部分,这个net intifiable asset既包含入账的资产,也包含之前没有记账但合并时应该记账的资产。因此本题并购的对价等于所购买的子公司的net intifiable asset,即没有gooill。 老师,没看懂答案第2点,为什么没有gooill,不是应该60吗?

NO.PZ201602060100001001 consolition with full gooill. consolition with partigooill. A is correct. The current ratio using the equity methoof accounting is Current assets/Current liabilities = £250/£110 = 2.27. Using consolition (either full or partigooill), the current ratio = £390/£200 = 1.95. Therefore, the current ratio is highest using the equity metho 考点 不同合并会计报表方法对会计比率的影响 。 解析 current ratio =Current assets/Current liabilities equity metho影响current asset和current liability, current ratio = £250/£110 = 2.27. consolition需要合并子公司的全部资产和负债 , current ratio=£390/£200 = 1.95 这道题没有gooill,但要注意不管有没有gooill,partigooill与full gooill的方式都不影响current asset的金额,因为gooill属于长期资产。 因此,A正确。 ※ 没有gooill的原因 题干中的信息 超出net fair value的部分是由于要购买unrecorlicenses , 其他资产和负债的fair value=book value。这句话可以得到两个结论 1. 子公司有一个未记账的资产,而在合并报表中,这项资产应该计入资产负债表。它的价值是并购对价超过子公司净资产fair value的部分。 相当于是NinMount公司花320买了Boswell公司一半的intifiable assets(包括已入账的也包括未入账的)。如果要买全部的intifiable assets则要花640其中580是为了买已入账的intifiable assets,剩下的60根据题目信息,都是为了买这个unrecorlicense。 2. 该项投资不产生gooill,因为gooill的定义是并购对价超过子公司net intifiable asset的部分,这个net intifiable asset既包含入账的资产,也包含之前没有记账但合并时应该记账的资产。因此本题并购的对价等于所购买的子公司的net intifiable asset,即没有gooill。 Current asset 在equity metho不是应该减少吗?因为Cash减少了

NO.PZ201602060100001001 老师好, 虽然通过题干可以得出其实GW是为0的,但我当时又去看了下MI在full GW和partiGW下的计算公式,如下 Full GW下,MI=(consiration/出资投资的比例)*不是你投资的比例 PartiGW下,MI=consiration*不是你投资的比例 然后我一看,哎哟,这个MI的公式也和GW具体是多少没关系哦,那FULL GW算出来的MI应该是最大的,即在题干的三个中full GW的equity最大,所以B的asset/liability比例最大。 老师请问我这么想哪里错了么? 不过我突然发现,我这么想算出来的其实是totasset/ totliability 和题干问的current asset/ current liability还是不一样的,所以不能直接等同。对吧老师? 谢谢老师