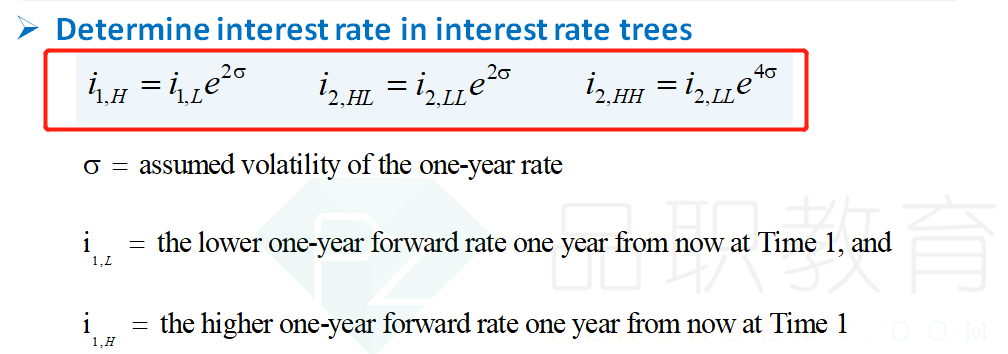

问题如下图:这题能用101.7877乘以e的2两倍volatility来计算node1-2吗

选项:

A.

B.

C.

解释:

NO.PZ2018123101000049 问题如下 Exhibit 3 presents most of the ta of a binomilognorminterest rate tree. Exhibit 4 presents most of the ta of the implievalues for a four-year, option-free, annupbonwith a 2.5% coupon baseon the information in Exhibit 3.Baseon the information in Exhibits 3 an4, the bonpriin euros No 1–2 in Exhibit 4 is to: A.102.7917 B.104.8640 C.105.2917 A is correct.考点考察利用利率二叉树定价解析: 想要得到节点1-2的债券价值,用到的数据有该节点右边的数据,即节点2-2,节点2-3的债券价值和Coupon,以及第一年末至第二年的Forwarrate。通过对未来债券价值的折现求得该节点1-2的债券价值value = {2.5+(0.5×101.5168+0.5×102.1350)} / 1.014925 = 102.7917 为什么只加了一个2.5?

NO.PZ2018123101000049问题如下Exhibit 3 presents most of the ta of a binomilognorminterest rate tree. Exhibit 4 presents most of the ta of the implievalues for a four-year, option-free, annupbonwith a 2.5% coupon baseon the information in Exhibit 3.Baseon the information in Exhibits 3 an4, the bonpriin euros No 1–2 in Exhibit 4 is to:A.102.7917B.104.8640C.105.2917 A is correct.考点考察利用利率二叉树定价解析: 想要得到节点1-2的债券价值,用到的数据有该节点右边的数据,即节点2-2,节点2-3的债券价值和Coupon,以及第一年末至第二年的Forwarrate。通过对未来债券价值的折现求得该节点1-2的债券价值value = {2.5+(0.5×101.5168+0.5×102.1350)} / 1.014925 = 102.7917 能否用t0和t1的数据推出答案?只能从后往前推么

104.8640 105.2917 A is correct. 考点考察利用利率二叉树定价 解析: 想要得到节点1-2的债券价值,用到的数据有该节点右边的数据,即节点2-2,节点2-3的债券价值和Coupon,以及第一年末至第二年的Forwarrate。通过对未来债券价值的折现求得该节点1-2的债券价值 value = {2.5+(0.5×101.5168+0.5×102.1350)} / 1.014925 = 102.7917 这个题不对啊?我是从后面推了一下尝试的,后面从一开始到102.1350都是不含着这个时点本身的2.5的。都是只有在往前面折算的时候单独加了2.5。为什么这个点No1-2要把2.5加在里面显示?这与其他的数字显示不一致啊

NO.PZ2018123101000049 问题如下 Exhibit 3 presents most of the ta of a binomilognorminterest rate tree. Exhibit 4 presents most of the ta of the implievalues for a four-year, option-free, annupbonwith a 2.5% coupon baseon the information in Exhibit 3.Baseon the information in Exhibits 3 an4, the bonpriin euros No 1–2 in Exhibit 4 is to: A.102.7917 B.104.8640 C.105.2917 A is correct.考点考察利用利率二叉树定价解析: 想要得到节点1-2的债券价值,用到的数据有该节点右边的数据,即节点2-2,节点2-3的债券价值和Coupon,以及第一年末至第二年的Forwarrate。通过对未来债券价值的折现求得该节点1-2的债券价值value = {2.5+(0.5×101.5168+0.5×102.1350)} / 1.014925 = 102.7917 NO.PZ2018123101000049问题如下Exhibit 3 presents most of the ta of a binomilognorminterest rate tree. Exhibit 4 presents most of the ta of the implievalues for a four-year, option-free, annupbonwith a 2.5% coupon baseon the information in Exhibit 3.Baseon the information in Exhibits 3 an4, the bonpriin euros No 1–2 in Exhibit 4 is to:A.102.7917B.104.8640C.105.2917A is correct.考点考察利用利率二叉树定价解析: 想要得到节点1-2的债券价值,用到的数据有该节点右边的数据,即节点2-2,节点2-3的债券价值和Coupon,以及第一年末至第二年的Forwarrate。通过对未来债券价值的折现求得该节点1-2的债券价值value = {2.5+(0.5×101.5816+0.5×102.1350)} / 1.014925 = 102.7917按照何老师课程里讲的,求no要加上当期coupon,求value则不用,为什么这里求no却不用加上当期coupon?

NO.PZ2018123101000049 为什么不能用上面一个数据除以e的2倍西格玛次方?