问题如下图:

请老师翻译下几个选项

选项:

A.

B.

C.

D.

解释:

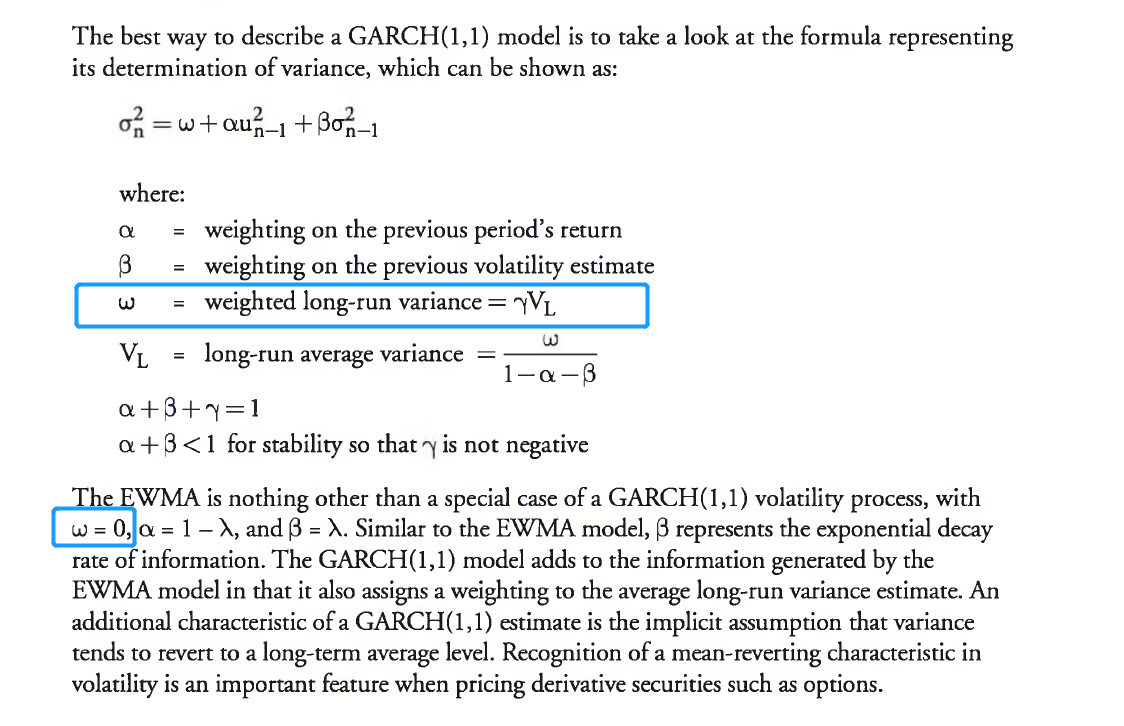

NO.PZ2016062402000052 Whiof the following four statements on mols for estimating volatility is incorre? In the EWMA mol, some positive weight is assigneto the long-run average varianrate. In the EWMA mol, the weights assigneto observations crease exponentially the observations become olr. In the GARCH(1,1) mol, a positive weight is estimatefor the long- run average varianrate. In the GARCH(1,1) mol, the weights estimatefor observations crease exponentially the observations become olr. The GARmol ha finite uncontionvariance, so statement is correct. In contrast, because α1+β\alpha_1+\betaα1+β sum to 1, the EWMA mol hunfinelong-run average variance. In both mols weights cline exponentially with time. 在EWMA模型中,长期平均方差的权重不是r吗?为什么说权重为0?

NO.PZ2016062402000052 Whiof the following four statements on mols for estimating volatility is incorre? In the EWMA mol, some positive weight is assigneto the long-run average varianrate. In the EWMA mol, the weights assigneto observations crease exponentially the observations become olr. In the GARCH(1,1) mol, a positive weight is estimatefor the long- run average varianrate. In the GARCH(1,1) mol, the weights estimatefor observations crease exponentially the observations become olr. The GARmol ha finite uncontionvariance, so statement is correct. In contrast, because α1+β\alpha_1+\betaα1+β sum to 1, the EWMA mol hunfinelong-run average variance. In both mols weights cline exponentially with time. 看到之前的解答中有提到,a是只为正数,而c是可以为正数。我想问的是,难道weighte是只能为正数吗?为什么a还是错误呢,烦请解答一下,谢谢~

看了其他提问,仍然不懂,求详细解析该题目,谢谢!

GARmol V(L)的权重不可以是0吗?