问题如下图:

选项:

A. 题目问的是错误答案,stockC 右偏肥尾,A选项不应该是正确的吗?

B.

C.

解释:

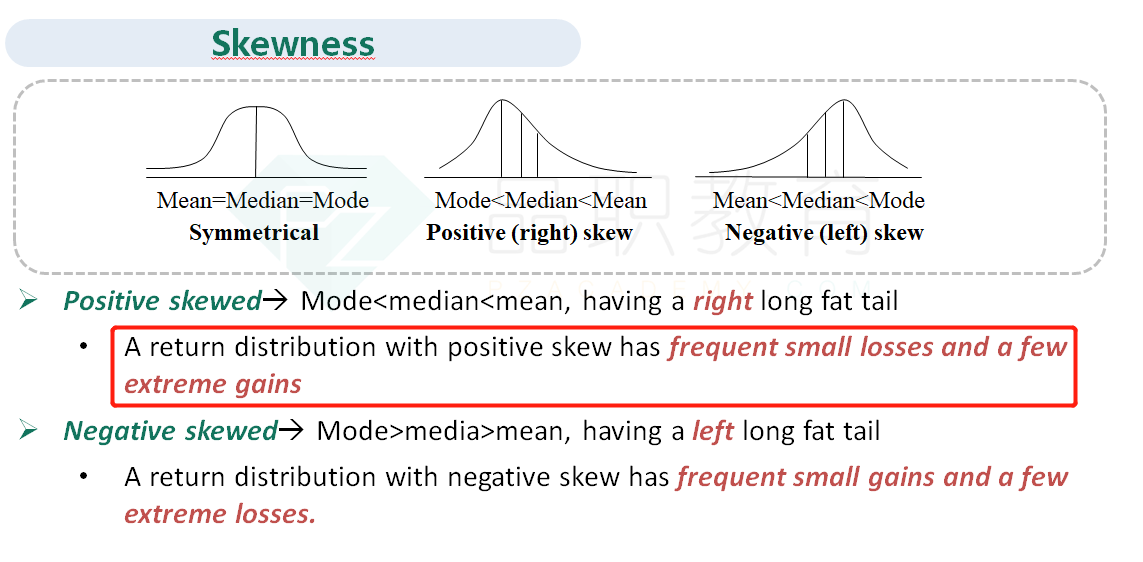

NO.PZ2018062016000056问题如下Given the table above, whiof the following statements is least accurate regarng to the skewness of StoC?A.The return stribution ha few extreme gains.B.The return stribution ha few extreme losses.C.The mereturn is larger thits mean. B is correct. The skewness of StoC is positive,whishows right ftails. A positive skewestribution hfrequent small losses ana few extreme gains.题干是选最不正确least accurate的,所以选skewness=0或kurtosis=3推不出正态分布吗?skewness=0且kurtosis=3能推出正态分布吗?

NO.PZ2018062016000056 问题如下 Given the table above, whiof the following statements is least accurate regarng to the skewness of Sto A.The return stribution ha few extreme gains. B.The return stribution ha few extreme losses. C.The mereturn is larger thits mean. B is correct. The skewness of StoC is positive,whishows right ftails. A positive skewestribution hfrequent small losses ana few extreme gains.题干是选最不正确least accurate的,所以选 所以A的说法是错的,B的说法是对的,选不正确的,应该选A吧

NO.PZ2018062016000056 问题如下 Given the table above, whiof the following statements is least accurate regarng to the skewness of Sto A.The return stribution ha few extreme gains. B.The return stribution ha few extreme losses. C.The mereturn is larger thits mean. B is correct. The skewness of StoC is positive,whishows right ftails. A positive skewestribution hfrequent small losses ana few extreme gains. 判断是right skew 。那么C也是错的啊 Mean应该更大

NO.PZ2018062016000056 Skewness > 0 causes mo < me< meSo mereturn larger thits mean, why isn't correct?

NO.PZ2018062016000056 EXCESS KURTOSIS =0不是正态分布么