问题如下图:

选项:

A.

B.

C.

解释:

分母不是YTM吗?为什么用的是coupon

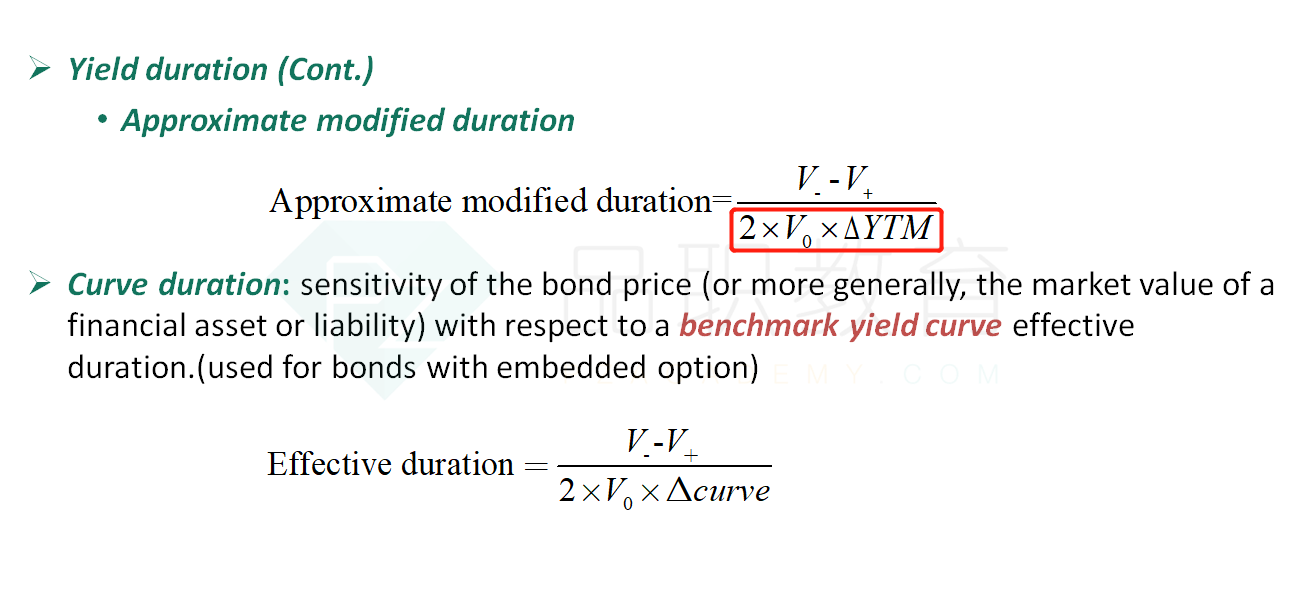

NO.PZ2016031001000113问题如下investor buys a three-yebonwith a 5% coupon rate paiannually. The bon with a yielto-maturity of 3%, is purchasea priof 105.657223 per 100 of pvalue. Assuming a 5-basis point change in yielto-maturity, the bons approximate mofieration is closest to: A.2.78. B.2.86. C.5.56. A is correct.The bons approximate mofieration is closest to 2.78. Approximate mofieration is calculateas:ApproxMour= [(PV−) − (PV+)] / [2×(ΔYiel×(PV0)]Lower yielto-maturity 5 bps to 2.95%: PV-=105.804232PV−= 5 / (1+0.0295) + 5/(1+0.0295)^2 + 105/ (1+0.0295)^3 =105.804232Increase yielto-maturity 5 bps to 3.05%: PV+=105.510494PV+= 5/ (1+0.0305) + 5/ (1+0.0305)^2 + 105/ (1+0.0305)^3 =105.510494PV0 = 105.657223, ΔYiel= 0.0005mofieration = (105.804232 − 105.510494)/(2×0.0005×105.657223) = 2.78ApproxMour=105.804232−105.5104942×0.0005×105.657223=2.78ApproxMour=\frac{105.804232-105.510494}{2\times0.0005\times105.657223}=2.78ApproxMour=2×0.0005×105.657223105.804232−105.510494=2.78考点approximate mofieration解析分别算出利率上升5bps后的PV+(105.510494)和利率下降5bps后的PV-(105.804232),代入approximate mofieration公式即可,故A正确。 老师可以使用计算器进行计算吗,或者有更快地方法进行计算吗

请问先求出Macaulration ,然后用Macaulration除以(1+y)求出mofieration可以吗?算出来结果一样的。

我想问下助教截图里的公式和强化里的公式不太一样 如何从强化串讲的公式来解这个题目呢?

2.86. 5.56. A is correct. The bons approximate mofieration is closest to 2.78. Approximate mofieration is calculateas: ApproxMour= [(PV−) − (PV+)] / [2×(ΔYiel×(PV0)] Lower yielto-maturity 5 bps to 2.95%: PV-=105.804232 PV−= 5 / (1+0.0295) + 5/(1+0.0295)^2 + 105/ (1+0.0295)^3 =105.804232 Increase yielto-maturity 5 bps to 3.05%: PV+=105.510494 PV+= 5/ (1+0.0305) + 5/ (1+0.0305)^2 + 105/ (1+0.0305)^3 =105.510494 PV0 = 105.657223, ΔYiel= 0.0005 mofieration = (105.804232 − 105.510494)/(2×0.0005×105.657223) = 2.78 ApproxMour=105.804232−105.5104942×0.0005×105.657223=2.78ApproxMour=\frac{105.804232-105.510494}{2\times0.0005\times105.657223}=2.78ApproxMour=2×0.0005×105.657223105.804232−105.510494=2.78 题目没有交代是不是含权债券,怎么想到是求approximate ration??课堂讲只有含权债券才用这个方法

请问一定要严格按照公式求吗?能不能为了省时间,简化公式(V_-V0)/VO/TM? 虽然有误差,但是误差很小,可忽略不计,就找最接近的答案?谢谢!