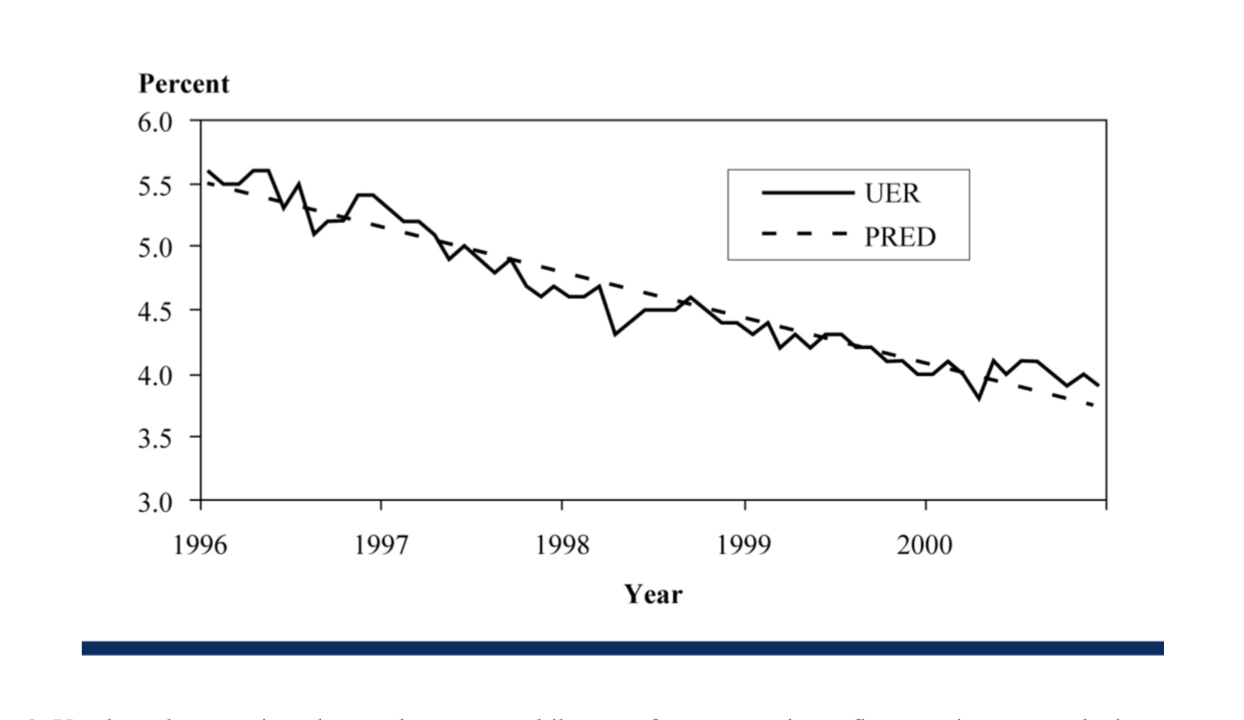

Figure 1 compares the predicted civilian unemployment rate (PRED) with the actual civilian

unemployment rate (UER) from January 1996 to December 2000. The predicted results come from

estimating the linear time trend model UERt = b0 + b1t + εt

What can we conclude about the appropriateness of this model?

课后答案是

The difference between UER and its forecast value, PRED, is the forecast error. In an appropriately

specified regression model, the forecast errors are randomly distributed around the regression line

and have a constant variance. We can see that the errors from this model specification are persistent.

The errors tend first to be above the regression line and then, starting in 1997, they tend to be below

the regression line until 2000 when they again are persistently above the regression line. This

persistence suggests that the errors are positively serially correlated. Therefore, we conclude that the

model is not appropriate for making estimates.