问题如下图:

选项:

A.

B.

C.

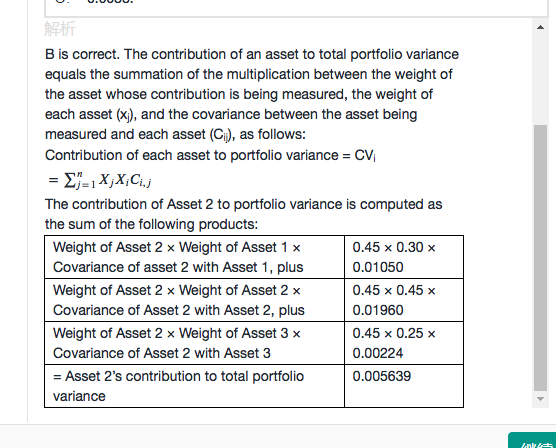

NO.PZ201809170400000604 问题如下 Baseon Exhibit 1, the contribution of Asset 2 to Manager C’s portfolio varianis closest to: A.0.0025. B.0.0056. C.0.0088. B is correct. The contribution of asset to totportfolio varianequals the summation of the multiplication between the weight of the asset whose contribution is being measure the weight of eaasset (xj), anthe covarianbetween the asset being measureaneaasset (Cij), follows:Contribution of eaasset to portfolio varian= CVi=∑j=1nXjXiCi,j={\textstyle\sum_{j=1}^n}X_jX_iC_{i,j}=∑j=1nXjXiCi,jThe contribution of Asset 2 to portfolio varianis computethe sum of the following procts: 这题是计算absolute risk contribution。 请问什么时候应该计算absolute risk contribution,什么时候是用absolute 除以 总的risk呢?

NO.PZ201809170400000604 问题如下 Baseon Exhibit 1, the contribution of Asset 2 to Manager C’s portfolio varianis closest to: A.0.0025. B.0.0056. C.0.0088. B is correct. The contribution of asset to totportfolio varianequals the summation of the multiplication between the weight of the asset whose contribution is being measure the weight of eaasset (xj), anthe covarianbetween the asset being measureaneaasset (Cij), follows:Contribution of eaasset to portfolio varian= CVi=∑j=1nXjXiCi,j={\textstyle\sum_{j=1}^n}X_jX_iC_{i,j}=∑j=1nXjXiCi,jThe contribution of Asset 2 to portfolio varianis computethe sum of the following procts: 分母应该怎么算?列一个3*3的表格然后把所有框里的相加吗

NO.PZ201809170400000604 问题如下 Baseon Exhibit 1, the contribution of Asset 2 to Manager C’s portfolio varianis closest to: A.0.0025. B.0.0056. C.0.0088. B is correct. The contribution of asset to totportfolio varianequals the summation of the multiplication between the weight of the asset whose contribution is being measure the weight of eaasset (xj), anthe covarianbetween the asset being measureaneaasset (Cij), follows:Contribution of eaasset to portfolio varian= CVi=∑j=1nXjXiCi,j={\textstyle\sum_{j=1}^n}X_jX_iC_{i,j}=∑j=1nXjXiCi,jThe contribution of Asset 2 to portfolio varianis computethe sum of the following procts: 为什么这里用了w2的平方乘上asset2和自己的covariance?为什么不是w2的平方*asset2的方差

请问这个计算是在哪个知识点里的?

这道题问的是proportion,是不是还得除以总风险?感觉答案给的是contribution的数字呢? 到底什么问法是除以总风险的结果,什么问法是不用除呢?