问题如下图:

选项:

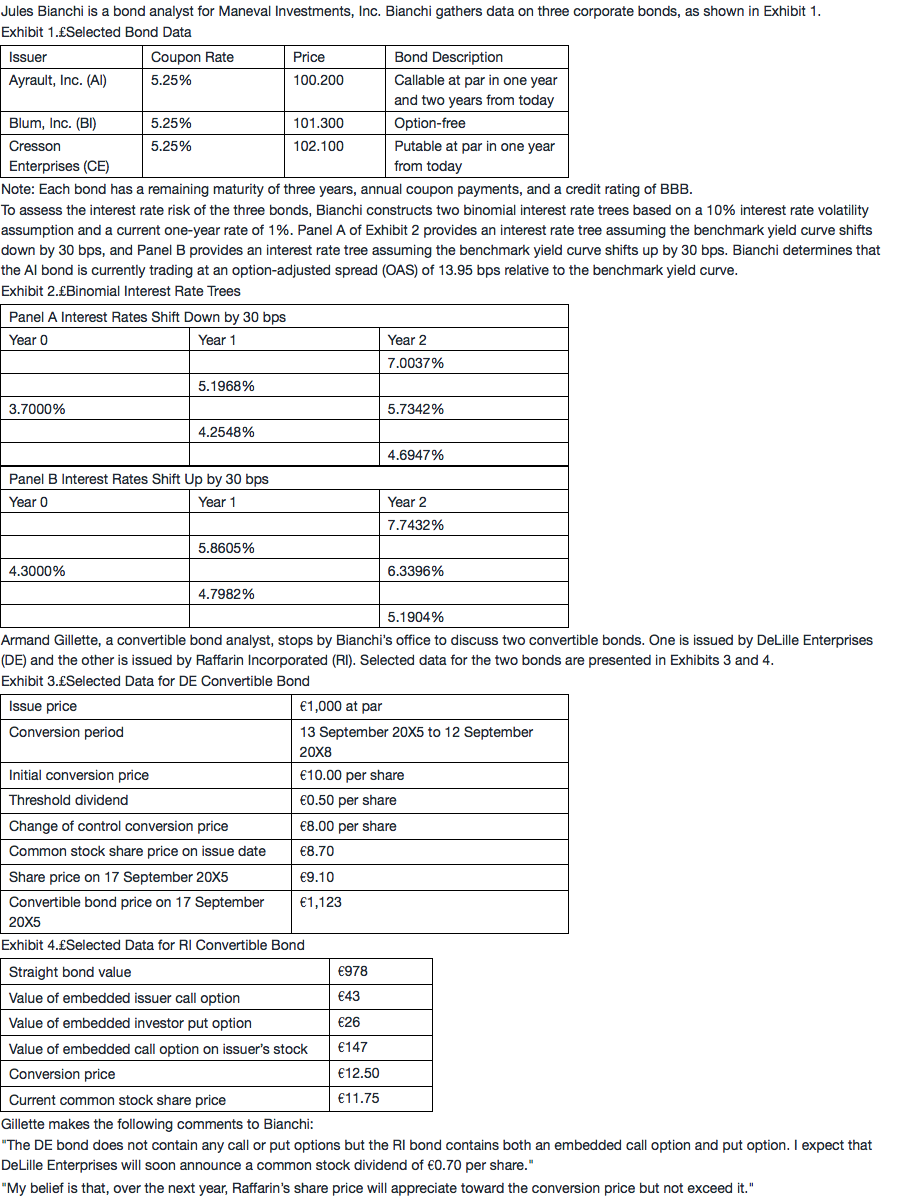

A.  请问老师the bond does not contain any call or put options but the bond contains both 这句英文怎么读不懂,怎么读出来这是一个既含CALL 又含有PUT的 可转换债券 ,谢谢老师

请问老师the bond does not contain any call or put options but the bond contains both 这句英文怎么读不懂,怎么读出来这是一个既含CALL 又含有PUT的 可转换债券 ,谢谢老师

B.

C.

解释:

NO.PZ201712110200000408 还想继续问一下,那么在前面小题里(如下),为什么又要综合考虑 call 和put 的VALUE呢,怎么区分什么时候考虑什么时候不考虑呢。谢谢! No.PZ201712110200000408 来源: 原版书 Baseon Exhibit 4, the arbitrage-free value of the RI bonis closest to: Value of callable putable convertible bon= Value of straight bon+ Value of call option on the issuer’s sto– Value of issuer call option + Value of investor put option.

€1,056. €1,108. C is correct. The value of a convertible bonwith both embeecall option ana put option ctermineusing the following formulValue of callable putable convertible bon= Value of straight bon+ Value of call option on the issuer’s sto– Value of issuer call option + Value of investor put option. Value of callable putable bon= €978 + €147 – €43 + €26 = €1,108 147为什么是债券持有人的呢?谢谢老师

为什么把这种算法算出来的value叫做无套利value?怎么个无套利法?

这道题不是很清楚,可以稍微一下吗?